At $2.1bn, cat bonds will be TWIA’s biggest source of funding for 2024

This content is copyright to www.artemis.bm and should not appear anywhere else, or an infringement has occurred. For 2024, the funding tower of residual market insurer the Texas Windstorm Insurance Association (TWIA) will see catastrophe bonds as its largest component, providing 32% of the funding […]

Industry Loss Warranty

Allstate lifts Nationwide cat reinsurance tower by $1bn to $7.9bn, helped by cat bonds

This content is copyright to www.artemis.bm and should not appear anywhere else, or an infringement has occurred. Allstate has significantly lifted the top of its Nationwide excess catastrophe reinsurance tower to just over $7.9 billion, which is almost a $1 billion increase from the prior […]

Industry Loss Warranty

Heritage lifts southeast reinsurance tower to $1.3bn, cat bonds assist

This content is copyright to www.artemis.bm and should not appear anywhere else, or an infringement has occurred. Heritage Insurance Holdings, Inc. has now finalised its catastrophe excess-of-loss reinsurance renewal for the coming year and the top of its reinsurance tower stretches to $1.3 billion, with […]

Industry Loss Warranty

At $2.1bn, cat bonds will be TWIA’s biggest source of funding for 2024

This content is copyright to www.artemis.bm and should not appear anywhere else, or an infringement has occurred. For 2024, the funding tower of residual market insurer the Texas Windstorm Insurance Association (TWIA) will see catastrophe bonds as its largest component, providing 32% of the funding […]

Industry Loss WarrantyThis content is copyright to www.artemis.bm and should not appear anywhere else, or an infringement has occurred.

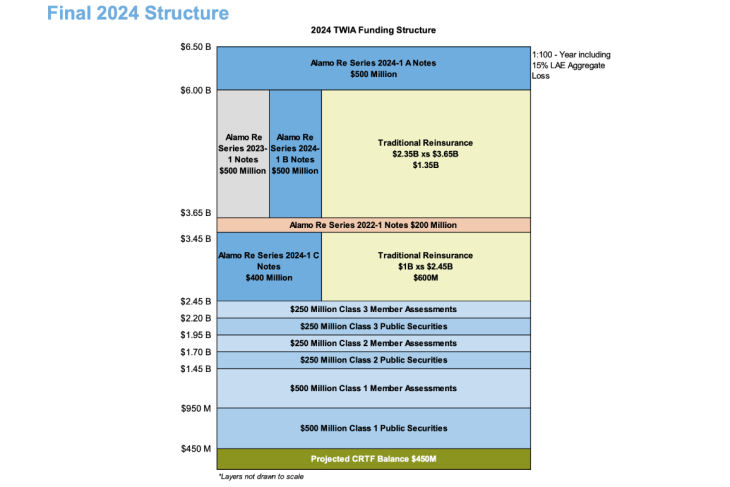

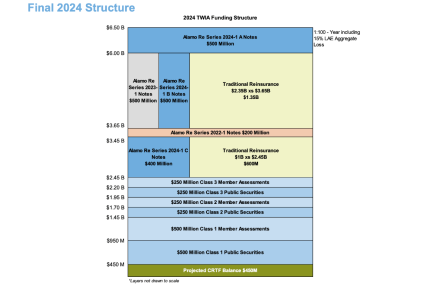

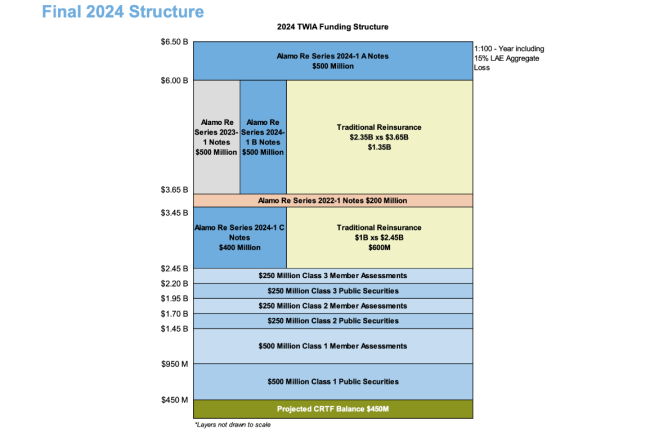

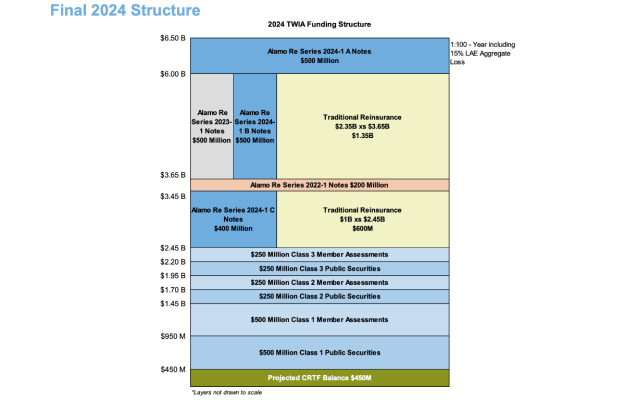

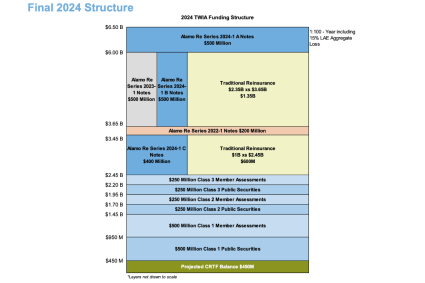

For 2024, the funding tower of residual market insurer the Texas Windstorm Insurance Association (TWIA) will see catastrophe bonds as its largest component, providing 32% of the funding limit needed to meet the statutory 1-in-100 year probable maximum loss for the coming hurricane season.

Recall that, back in February the Board of the Texas Windstorm Insurance Association (TWIA) approved a 1-in-100 year PML for 2024 funding purposes at a new high of $6.5 billion, meaning the insurer of last resort needs just over $4 billion in reinsurance limit for the 2024 wind season.

Recall that, back in February the Board of the Texas Windstorm Insurance Association (TWIA) approved a 1-in-100 year PML for 2024 funding purposes at a new high of $6.5 billion, meaning the insurer of last resort needs just over $4 billion in reinsurance limit for the 2024 wind season.

Already TWIA has been making rapid progress in securing that, helped enormously by the catastrophe bond market.

TWIA will have $700 million in catastrophe bond limit from prior year issues that rolls forwards to provide cover through the 2024 hurricane season.

These outstanding cat bonds have also been repositioned within TWIA’s funding tower for 2024, to make most efficient use of their coverage alongside newly placed cat bonds and reinsurance that will be bought.

The insurer added its largest cat bond yet to the funding tower, in the recently completed $1.4 billion Alamo Re Ltd. (Series 2024-1) catastrophe bond that we have been covering in recent weeks.

In addition to that $2.1 billion of cat bond protection, TWIA will be out in the traditional reinsurance market to secure $1.95 billion in cover as well, before June 1st.

It’s now come to light that TWIA had already placed $750 million of that traditional reinsurance limit before the end of April.

The expectation is that the rest of the needed limit will be secured well in advance of the end of May.

Once all the new reinsurance is secured, the $2.1 billion of catastrophe bonds will make up the largest component of TWIA’s funding for 2024, at 32% of the $6.5 billion.

After that, $2 billion of member assessments and public securities will contribute 31% of funding between them, then the $1.95 billion of traditional reinsurance (some of which could come from collateralized or fronted ILS market sources, we expect) will make up another 30% of funding, and lastly a 7% contribution from the CRTF (catastrophe reserve trust fund).

You can see TWIA’s funding and reinsurance tower for 2024 below, including the positioning of its catastrophe bonds and traditional reinsurance layers:

It’s testament to the appetite of the capital markets to support TWIA’s reinsurance needs that it is catastrophe bonds that now make up the largest share of its funding needs.

TWIA has been directly sponsoring catastrophe bonds since 2014 and now sits as one of the largest sponsors in our cat bond market sponsors leaderboard.

At $2.1bn, cat bonds will be TWIA’s biggest source of funding for 2024 was published by: www.Artemis.bm

Our catastrophe bond deal directory

Sign up for our free weekly email newsletter here.

Allstate lifts Nationwide cat reinsurance tower by $1bn to $7.9bn, helped by cat bonds

This content is copyright to www.artemis.bm and should not appear anywhere else, or an infringement has occurred. Allstate has significantly lifted the top of its Nationwide excess catastrophe reinsurance tower to just over $7.9 billion, which is almost a $1 billion increase from the prior […]

Industry Loss WarrantyThis content is copyright to www.artemis.bm and should not appear anywhere else, or an infringement has occurred.

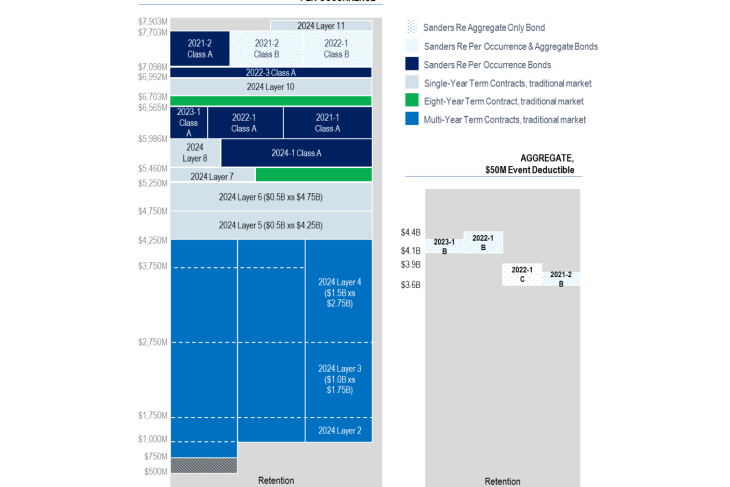

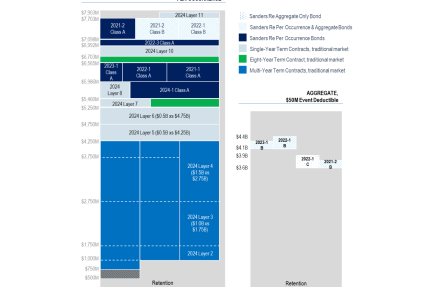

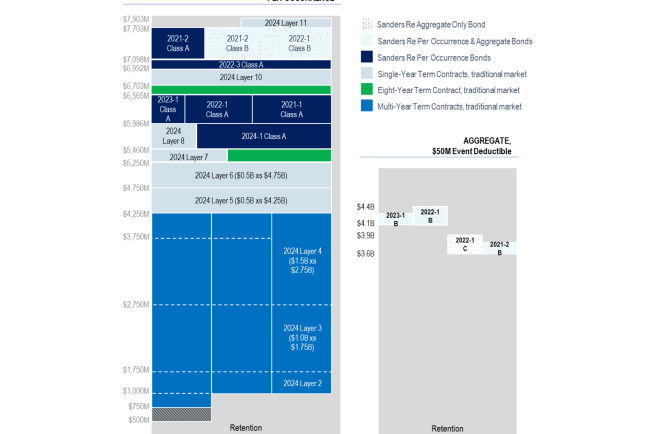

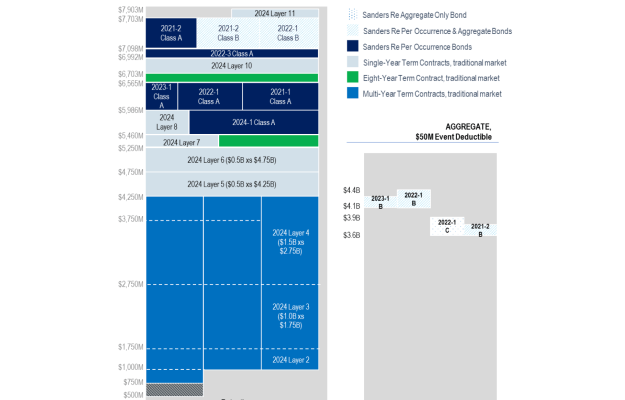

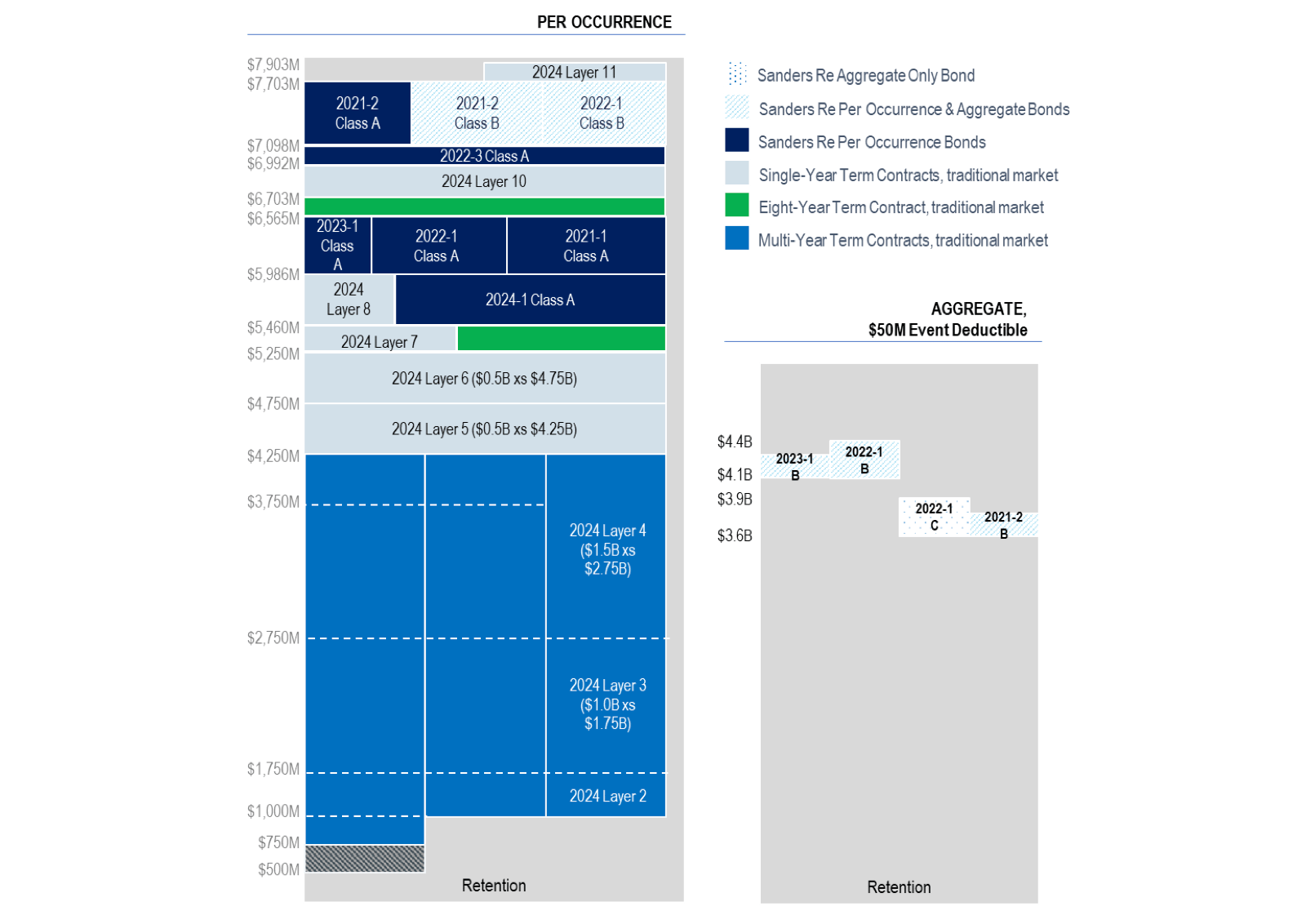

Allstate has significantly lifted the top of its Nationwide excess catastrophe reinsurance tower to just over $7.9 billion, which is almost a $1 billion increase from the prior year and catastrophe bonds are filling out much of the upper-layers.

Catastrophe bonds now occupy portions of Allstate’s reinsurance tower from $5.46 billion right the way up to $7.7 billion, with the Sanders Re cat bond program filling out a significant proportion of the upper-layers of the insurers program.

Catastrophe bonds now occupy portions of Allstate’s reinsurance tower from $5.46 billion right the way up to $7.7 billion, with the Sanders Re cat bond program filling out a significant proportion of the upper-layers of the insurers program.

Secured for 2024, the $400 million Sanders Re III Ltd. (Series 2024-1) catastrophe bond issued in January is the most recent ILS market addition and occupies an important slot in the tower, covering 76% of a layer attaching at $5.46 billion and running to almost $6 billion of losses.

Significant new traditional reinsurance purchases have also bulked out the tower and helped Allstate to grow it to the new approaching $8 billion level.

But, at the same time as the top of Allstate’s main nationwide catastrophe reinsurance tower extending by approximately $1 billion, at the other end there is more risk now being retained.

Where as, in 2023, Allstate’s Nationwide Excess Catastrophe Reinsurance Program covered it for losses of up to $6.92 billion after retentions of between $500 million and $750 million, the retentions have now increased.

For 2024, Allstate’s Nationwide catastrophe reinsurance tower provides coverage for loss events up to $7.90 billion, after retentions of $500 million to $1 billion.

Another notable change is that Allstate no longer has aggregate reinsurance coverage that features a franchise deductible.

With the aggregate reinsurance tower solely provided by catastrophe bonds, the old Sanders cat bonds that had a $1 million franchise deductible are no more.

Now, Allstate only has four tranches of cat bonds that provide aggregate reinsurance, but feature a $50 million event deductible instead.

Recall that, we reported recently on the last tranche of aggregate cat bond notes that featured a franchise deductible to reveal that qualifying losses from the risk period that ended March 31st 2024 are now very close to attaching the coverage and so Allstate may benefit from recoveries under that tranche, should loss development continue.

But, that tranche was due to mature anyway, so no longer features in the insurers reinsurance programs from April 1st this year. But it will stay available for any recoveries that can be made, should the aggregate loss tally creep higher and attach the coverage.

Placed in the traditional reinsurance market in 2024 for Allstate were multi-year contracts attaching at the $500 million to $1 billion retentions and providing coverage of up to $4.25 billion, so exhausting at $4.75 billion.

In addition, Allstate placed two eight-year term reinsurance contracts, that provide it $105 million of cover in excess of a minimum $5.25 billion retention and $131 million of cover in excess of a minimum $6.57 billion retention.

Allstate also placed five single-year term reinsurance agreements in 2024 as well, which have a range of attachment and exhaustion points throughout the Nationwide catastrophe reinsurance tower.

You can see how Allstate’s Nationwide reinsurance towers looked at April 1st 2024 below:

Allstate also purchased a Canadian catastrophe reinsurance arrangement at January 2024, providing total coverage of CA$355 million in excess of a CA$75 million retention.

One other notable fact, related to Allstate’s reinsurance arrangements for 2024, is the increased cost associated with its procurement.

While more limit has been secured, the cost of Allstate’s reinsurance has risen faster, it seems.

Allstate said that the total cost of its property catastrophe reinsurance programs, excluding reinstatement premiums, was $286 million in Q1 2024, compared to $219 million in Q1 2023.

In addition, Allstate has disclosed that its reinsurance arrangements cost it $1.02 billion in 2023, which was up significantly from $788 million in 2022.

But, Allstate has been steadily filling out the upper-layers of its reinsurance tower over the last two years, largely with catastrophe bonds, and has now extended it by almost $1 billion, so the increased costs are understandable, along with the effects of the hard reinsurance market.

View details of every catastrophe bond ever sponsored by Allstate here.

Read all of our reinsurance renewals news.

Allstate lifts Nationwide cat reinsurance tower by $1bn to $7.9bn, helped by cat bonds was published by: www.Artemis.bm

Our catastrophe bond deal directory

Sign up for our free weekly email newsletter here.

Heritage lifts southeast reinsurance tower to $1.3bn, cat bonds assist

This content is copyright to www.artemis.bm and should not appear anywhere else, or an infringement has occurred. Heritage Insurance Holdings, Inc. has now finalised its catastrophe excess-of-loss reinsurance renewal for the coming year and the top of its reinsurance tower stretches to $1.3 billion, with […]

Industry Loss WarrantyThis content is copyright to www.artemis.bm and should not appear anywhere else, or an infringement has occurred.

Heritage Insurance Holdings, Inc. has now finalised its catastrophe excess-of-loss reinsurance renewal for the coming year and the top of its reinsurance tower stretches to $1.3 billion, with increased protection for the southeast US, while shrinking coverage for the northeast US and Hawaii.

Year-on-year, Heritage has shifted its focus on reinsurance protection to the southeast over the northeast it seems, perhaps reflecting stronger growth in states such as Florida this year, and perhaps also a nod to the impending and expected to be active hurricane season.

Year-on-year, Heritage has shifted its focus on reinsurance protection to the southeast over the northeast it seems, perhaps reflecting stronger growth in states such as Florida this year, and perhaps also a nod to the impending and expected to be active hurricane season.

For 2024, the Heritage reinsurance program provides coverage up to $1.3 billion of losses for the southeast United States, $1.1 billion for the northeast and $750 million for Hawaii.

That compares to a 2023 reinsurance renewal that provided $1.3 billion for the Northeast, $1.1 billion for the Southeast and $870 million in Hawaii.

The all indemnity based, catastrophe excess-of-loss reinsurance program for 2024, covers subsidiaries Heritage Property Casualty Insurance Company, Narragansett Bay Insurance Company and Zephyr Insurance Company for the year to end of May 2025.

This year, Heritage has more in-force catastrophe bond cover that assists it through the multi-year protection and terms they offer.

That said, the total consolidated cost of the Heritage reinsurance program for 2024 is reported to be slightly higher year-on-year at $422.3 million, compared to the $420.5 million paid a year earlier.

But, it’s notable that one change to the tower was that Heritage replaced a $70 million chunk of reinsurance that came from the Florida Reinsurance to Assist Policyholders (RAP) program in 2023, with private market coverage in 2024. So the slight increase in cost is perhaps lower than might have been anticipated with that in mind.

“We are delighted to announce the successful completion of our 2024-2025 catastrophe excess of loss reinsurance program,” explained Heritage CEO Ernie Garateix. “We value the unwavering support of our valued long-term reinsurance partners as well as new reinsurance partners and reaffirm our commitment to provide appropriate coverage for the markets we serve.

“I’m pleased to continue to place a portion of our program through capital markets using catastrophe bonds issued by Citrus Re, which provides multi-year reinsurance coverage.”

Heritage has $435 million of outstanding catastrophe bond backed reinsurance, which provides multi-year, layered protection and so assists the company when it comes to renewals, given the certainty on price and coverage terms that provides.

Heritage most recently added $100 million of named storm reinsurance for southeast states through a Citrus Re Ltd. (Series 2024-1) transaction issued in March 2024.

The carrier also has $120 million of northeast only named storm reinsurance limit and a shared $115 million of northeast and Hawaii named storm limit through its May 2023 issuance Citrus Re Ltd. (Series 2023-1).

In addition, $100 million of northeast only reinsurance from the Citrus Re Ltd. (Series 2022-1) cat bond is also available for the coming hurricane season.

The retention on the Heritage reinsurance program is approximately $40 million for the southeast and Hawaii and $32 million for the northeast for 2024, with the northeast up slightly from the $30 million retention it had a year ago.

Once again, Heritage can use its captive reinsurance vehicle Osprey Re to buy-down the retention and expand the program coverage as well.

In terms of the state backed reinsurance, Heritage opted for a 90% Florida Hurricane Catastrophe Fund participation, which was consistent with the prior year.

As Heritage continues on its expansion plan, to become an increasingly super-regional property and casualty insurance carrier, it’s encouraging to see the company continuing to place the catastrophe bond market at the heart of its reinsurance arrangements and we should expect more cat bonds to be sponsored next year, particularly with its 2022 issuance set to mature prior to the 2025 hurricane season.

Heritage lifts southeast reinsurance tower to $1.3bn, cat bonds assist was published by: www.Artemis.bm

Our catastrophe bond deal directory

Sign up for our free weekly email newsletter here.

Positive reinsurance trend to remain strong through renewals: Munich Re CEO

This content is copyright to www.artemis.bm and should not appear anywhere else, or an infringement has occurred. According to Joachim Wenning, CEO and Chair of the Board of Management at Munich Re, the positive trends experienced in reinsurance over the last year are not expected […]

Industry Loss WarrantyThis content is copyright to www.artemis.bm and should not appear anywhere else, or an infringement has occurred.

According to Joachim Wenning, CEO and Chair of the Board of Management at Munich Re, the positive trends experienced in reinsurance over the last year are not expected to weaken during the remaining renewals of 2024.

In his letter to shareholders at yesterdays Munich Re AGM, Wenning explained that reinsurance has been particularly good for Munich Re over the last year or so.

Commenting on 2023, Wenning said, “Insurance revenue in this field rose to about €38bn, driven by organic growth particularly in natural disaster business and specialty insurance.

“Reinsurance as a whole contributed nearly €3.9bn to the Group’s 2023 net result. Let me put this straight: these figures are spectacular.”

This despite the P&C reinsurance result being “weighed down by high natural disaster losses,” although hurricane season was relatively benign there were “numerous severe convective storms in North America and Europe in particular caused unprecedented losses,” Wenning went on to explain.

Munich Re, like other major reinsurers, has taken the opportunity to grow its P&C reinsurance business through the hard market conditions and Wenning does not expect any immediate reversion to reinsurance fortunes, for his firm at least.

Looking ahead, the Munich Re CEO explained, “We’re confident that the favourable market environment for property-casualty reinsurers will continue throughout 2024.”

He continued to explain that, in 2024, “The renewals at 1 January were positive for us. We managed to continue the previous year’s very high level of profitability and further enhance the quality of our portfolio.”

Adding, “What’s more, we don’t anticipate this trend to weaken during this year’s remaining renewal rounds.”

So, Munich Re is expecting stability at least, overall at the upcoming reinsurance renewals of June and July 2024, it seems.

With such a broadly diversified and global book, that’s perhaps no surprise, as while some areas of the market may be softening, such as top-layer catastrophe risks, it’s clear that other areas of reinsurance are set to remain stable, in pricing terms, while others continue to catch-up with primary rate trends as well.

All in, a positive outlook from the CEO of one of the largest companies in the industry, which should perhaps help to settle any nerves that a wholesale, capital influx triggered softening could be on the horizon.

Positive reinsurance trend to remain strong through renewals: Munich Re CEO was published by: www.Artemis.bm

Our catastrophe bond deal directory

Sign up for our free weekly email newsletter here.

Universal finalises renewal with more multi-year reinsurance, expanded panel: CEO

This content is copyright to www.artemis.bm and should not appear anywhere else, or an infringement has occurred. Universal Insurance Holdings, the Florida headquartered insurer, has already completed its June reinsurance renewal and its CEO said that the company added more multi-year protection this time, while […]

Industry Loss WarrantyThis content is copyright to www.artemis.bm and should not appear anywhere else, or an infringement has occurred.

Universal Insurance Holdings, the Florida headquartered insurer, has already completed its June reinsurance renewal and its CEO said that the company added more multi-year protection this time, while also adding more reinsurers to its panel.

As a Florida focused carrier, Universal is considered one of the bellwether’s for signals of appetite for risk and use of reinsurance for those operating in the state.

As a Florida focused carrier, Universal is considered one of the bellwether’s for signals of appetite for risk and use of reinsurance for those operating in the state.

Back in March, the company had already revealed that it had secured 90% of its first-event reinsurance tower for 2024 with more multi-year coverage, as the company got out early to avoid the market congestion around the mid-year renewals.

Now, Stephen J. Donaghy, Chief Executive Officer of Universal, has explained that the mid-year reinsurance renewal is completed some weeks ahead of the coverage inception date.

“I’m pleased to announce the completion of our 2024-2025 reinsurance renewal for our insurance entities, as our program is now fully supported and secured,” CEO Donaghy explained in announcing the insurers first-quarter results (read more on the results over at our sister publication Reinsurance News).

Donaghy went on to explain that, “We’ve also secured additional multi-year coverage, taking us through the 2025-2026 hurricane season and have added new, financially strong reinsurers to our existing panel of long-term partners.”

“This achievement reflects the diligence and planning of our reinsurance team throughout the year,” he added. Also saying that, “Program cost and coverage were consistent with our expectations and we’ll provide specific details at the end of May, as we typically do.”

Universal has been growing back into Florida and reported 5.2% growth in Florida for the first-quarter, but also 25.6% in other states, showing that its still on a path to diversify its business further.

Still, almost 80% of Universal’s premiums written in Q1 2024 came from Florida, reflecting the fact its reinsurance tower is largely a Florida wind risk opportunity.

Universal finalises renewal with more multi-year reinsurance, expanded panel: CEO was published by: www.Artemis.bm

Our catastrophe bond deal directory

Sign up for our free weekly email newsletter here.

Rate increases slower for catastrophe exposed US property in Q1: Marsh

This content is copyright to www.artemis.bm and should not appear anywhere else, or an infringement has occurred. In what is perhaps a reflection of an insurance and reinsurance marketplace with more catastrophe risk capital available, broker Marsh has for the first time in a while […]

Industry Loss WarrantyThis content is copyright to www.artemis.bm and should not appear anywhere else, or an infringement has occurred.

In what is perhaps a reflection of an insurance and reinsurance marketplace with more catastrophe risk capital available, broker Marsh has for the first time in a while cited a slowing level of rate increases for catastrophe exposed commercial property accounts in the United States, with even some rate decreases reported.

For around five years now, there hasn’t been any real talk of catastrophe exposed property insurance rates in the US decreasing.

For around five years now, there hasn’t been any real talk of catastrophe exposed property insurance rates in the US decreasing.

The seemingly inexorable rise in property insurance rates for both commercial and residential properties in regions of higher catastrophe risks, as well as those with tropical storm exposure on the coast, has been a feature of the market for some years now and while it does continue, there are signs of moderation, perhaps even stabilisation.

Marsh reports that, overall, it sees US commercial property insurance rates as still increasing, but stabilising, with an average rate increase of 8% in the first-quarter of 2024, down from an 11% average increase in the final quarter of 2023.

However, the commentary is perhaps the most positive, from a protection buyers point of view, in quite a long time.

“Many companies were able to secure additional limits in higher layers and improve coverage as competition increased and rate increases have leveled off,” Marsh explained.

With one driver being that, “Strong insurer financial results and additional reinsurance market supply led to increased insurer appetite.”

Importantly, the broker added that, “Companies with concentrations of assets in catastrophe (CAT) zones — such as the Gulf of Mexico, Atlantic coast, and California — that had experienced higher rate increases in recent years have begun to see lower increases or even decreases.”

But also explained that things still aren’t easy and adjustments are still being made, as “Underwriters continued to scrutinize CAT deductibles and limitations of cover for non-physical damage, cyber, and communicable disease.”

As a result of still very high insurance rates, protection buyers are exploring alternatives still and Marsh explained that, “Insureds continued to increase retentions and adopt alternative risk transfer such as captives, parametric, or structured solutions.”

In Europe where property rates slowed to 5% in Q1, down from a 7% increase in the previous quarter, the picture has also perhaps become more stable, with buyers in catastrophe exposed areas scrutinised, but capacity seen as generally available, even for cat exposed risks, although Marsh noted that, “Companies with natural catastrophe exposure generally saw above average price increases, capacity reductions, increased deductibles, and scrutiny of limits.”

It’s not the same everywhere though and Marsh highlighted that Mexico is one area where capacity was seen as low, “Contributing to increased rates in the wake of Hurricane Otis, particularly for complex risks and those with catastrophe exposure,” although in LatAm overall property rate increases slowed slightly as well in Q1.

In Asia, while overall property rates declined 1%, Marsh said that, “Highly CAT-exposed geographies, including Japan, Taiwan, and the Philippines, and industries with significant business interruption exposure remained exceptions to the downward rate trend.”

Elsewhere, such as the Middle East, Africa and India, reinsurance pricing is still filtering through and resulting in some rate increases, Marsh noted.

Overall around the globe, it’s clear catastrophe exposed property rates continue to move higher at the fastest rates, which is as you might expect, but there is also now clear evidence that improved reinsurance market conditions and better supply of catastrophe risk capital is filtering down to the primary insurance space.

In the United States, where much of the influx of catastrophe risk capital is naturally focused, conditions appear much-improved, compared to just a few quarters ago, with the effects of more abundant reinsurance capital definitely evident here.

It will be interesting to see whether any moderation begins to become evident in the US homeowners marketplace, in regions with elevated catastrophe risks, or whether that takes longer to manifest and could be dependent on how the hurricane season plays out.

However, it is worth remembering, that some are forecasting that catastrophe exposed commercial property insurance renewals are still expected to see perhaps the biggest rate gains in 2024.

Rate increases slower for catastrophe exposed US property in Q1: Marsh was published by: www.Artemis.bm

Our catastrophe bond deal directory

Sign up for our free weekly email newsletter here.

ILS market yield potential remains attractive, cat bonds still top-pick: K2 Advisors

This content is copyright to www.artemis.bm and should not appear anywhere else, or an infringement has occurred. K2 Advisors, the hedge fund focused investment management unit of Franklin Templeton, believes that the forward-looking total yield potential of insurance-linked securities (ILS) remains attractive despite recent spread […]

Industry Loss WarrantyThis content is copyright to www.artemis.bm and should not appear anywhere else, or an infringement has occurred.

K2 Advisors, the hedge fund focused investment management unit of Franklin Templeton, believes that the forward-looking total yield potential of insurance-linked securities (ILS) remains attractive despite recent spread tightening, leading the manager to keep catastrophe bonds as its top sub-sector pick.

![]() Looking to the rest of the second-quarter of 2024, overall, “the ILS market remains attractive,” after a more orderly period of reinsurance renewals and recent tightening of spreads, K2 Advisors said.

Looking to the rest of the second-quarter of 2024, overall, “the ILS market remains attractive,” after a more orderly period of reinsurance renewals and recent tightening of spreads, K2 Advisors said.

“The rate-on-line for private ILS strategies and the catastrophe bond market spread remain elevated and provide appealing total yield potential,” the alternative asset manager explained.

K2 Advisors continues to believe that investors should look to alternatives, such as insurance-linked securities (ILS), as diversifying strategies are an advised complement to their long-only portfolios, which the asset manager cautions are “only becoming more and more correlated to one another.”

Which makes accessing relatively uncorrelated returns from an asset class such as ILS and reinsurance all the more important right now.

They explain, “We think it is prudent to think of future returns and risk distributions as being wider and having fatter tails to both the upside and downside. Active asset managers, of which hedge funds are the most agile and dynamic, may need to be a larger component of asset owners’ portfolios for the foreseeable future.”

On ILS, the K2 Advisors team note that, “The forward- looking total yield potential in ILS markets remains attractive.”

You can analyse the yield of the catastrophe bond market using Artemis’ chart.

While catastrophe bond spreads tightened in response to supply-demand dynamics, the team still believe stabilisation is ahead.

“Given the projections for an extremely active year of primary market issuance, coupled with the fact that we’ve already seen over US$5 billion of such offerings during the first quarter, we expect spreads will likely stabilize as we approach hurricane season,” the K2 Advisors team explained.

Adding that, “The combination of increasing investor demand for more senior ILS risk and higher total insured values (likely due to economic inflation) has led the catastrophe bond market to reach its largest size on record.

“The current spread environment, coupled with meaningful collateral return, continues to provide, in our view, an attractive entry point for investors into the catastrophe bond market.”

K2 Advisors maintains an “overweight” view on the insurance-linked securities (ILS) sector as a whole, given the still attractive returns it can generate for investors.

On catastrophe bonds, private ILS transactions (so collateralized reinsurance) and retrocession, K2 Advisors remains with a “strongly overweight” view.

While the manager is “neutral” on industry-loss warranties (ILW’s) and “strongly underweight” life ILS investments.

When it comes to ranking those sub-sectors, which K2 Advisors does versus other alternative and hedge fund asset classes using a conviction and type of investment weighting as to how it might recommend a strategy, the manager places catastrophe bonds right at the top.

Cat bonds have a z-score of 2, retrocession 1.6, private ILS transactions 1.4 and these all come in the top four recommended sub-sector strategies, in K2 Advisor’s opinion.

Such scoring and recommendation are seen by end-investors, which can only be good for the long-term visibility and popularity of the ILS asset class.

Reflecting on the year so far, the K2 Advisors team say that, “The lack of pricing giveback following the rate reset last year was a strong positive sign of the future health of the markets,” at the key January reinsurance renewals.

Looking ahead, for catastrophe bonds in particular, the investment manager explained, “We expect to see some level of spread stabilization over the next several months, as increased primary market activity will help soak up excess cash in the market.

“There was a record setting US$15 billion of new catastrophe bond issuance in 2023, and early indications suggest primary market issuance in 2024 could set another record.”

ILS market yield potential remains attractive, cat bonds still top-pick: K2 Advisors was published by: www.Artemis.bm

Our catastrophe bond deal directory

Sign up for our free weekly email newsletter here.

US cat sees “material softening” in minimum rates-on-line: Gallagher Re

This content is copyright to www.artemis.bm and should not appear anywhere else, or an infringement has occurred. Catastrophe reinsurance pricing for programs in the United States is seeing “material softening” in minimum rates-on-line, broker Gallagher Re has said, as reinsurers “abandon” the need for top-layer […]

Industry Loss WarrantyThis content is copyright to www.artemis.bm and should not appear anywhere else, or an infringement has occurred.

Catastrophe reinsurance pricing for programs in the United States is seeing “material softening” in minimum rates-on-line, broker Gallagher Re has said, as reinsurers “abandon” the need for top-layer pricing to exceed the risk-free rate.

![]() While there are only limited US property catastrophe reinsurance renewals at April 1st, the broker notes that placements seen suggest a continuation of the moderation trend witnessed at January renewals.

While there are only limited US property catastrophe reinsurance renewals at April 1st, the broker notes that placements seen suggest a continuation of the moderation trend witnessed at January renewals.

All of which is playing out in the catastrophe bond market, where pricing for protection has softened over recent months.

“Capacity has continued to flow into the property catastrophe market, where capacity is sufficient to meet expiring and new capacity needs,” Gallagher Re explained.

Gallagher Securities, the insurance-linked securities (ILS) and investment banking broker-dealer arm of the broker noted the trend in the cat bond market through the first-quarter of 2024.

Saying that, “Cat bond risk spreads for most perils have declined 30% plus year-on-year but remain stable vs. Q4 2023 with growing capacity in dynamic balance with growing demand.”

You can analyse trends in cat bond risk spreads by year and by quarter in our chart.

While cat bonds generally place in the upper-layers of reinsurance towers, Gallagher Re noted that lower-layers are still more challenging for cedents.

“Cat pricing discipline continued at the bottom end of programs, where risk adjusted decreases were difficult to achieve,” the broker said.

While at higher layers, where the cat bond market is most prevalent, “We saw risk adjusted rate reductions at the top end of programs, particularly on capacity that was purchased new in the height of the hard market.

“We are seeing the end of “inverted pricing” where new top layers placed in the past couple years required pricing in excess of underlying layers.”

Gallagher Re sees the risk market as still firmer than property catastrophe placement for the United States, as capital has not flowed to that segment of the market as much as to pure cat risks.

“That said, across both risk and cat markets we are seeing material softening in minimum rates on line, as reinsurers abandon the requirement for top layer pricing to exceed the risk-free rate of return in US Treasuries,” stated Gallagher Re.

US cat sees “material softening” in minimum rates-on-line: Gallagher Re was published by: www.Artemis.bm

Our catastrophe bond deal directory

Sign up for our free weekly email newsletter here.

Improved Florida cat reinsurance renewal conditions expected for June 1: MMC CEO

This content is copyright to www.artemis.bm and should not appear anywhere else, or an infringement has occurred. Early signs suggest that the Florida catastrophe reinsurance renewals at June 1st 2024 will see improved conditions for cedents, as capital has flowed in and reinsurer appetites have […]

Industry Loss WarrantyThis content is copyright to www.artemis.bm and should not appear anywhere else, or an infringement has occurred.

Early signs suggest that the Florida catastrophe reinsurance renewals at June 1st 2024 will see improved conditions for cedents, as capital has flowed in and reinsurer appetites have recovered, according to Marsh McLennan CEO John Doyle.

Speaking yesterday during the Marsh McLennan earnings call, Doyle highlighted an improving marketplace for the clients of his firm’s reinsurance broker Guy Carpenter.

Speaking yesterday during the Marsh McLennan earnings call, Doyle highlighted an improving marketplace for the clients of his firm’s reinsurance broker Guy Carpenter.

The recent April 1st reinsurance renewals saw increased capacity and reinsurer appetite, which the broker expects will positively influence the June reinsurance renewals as well in 2024.

“Reinsurance market conditions remain stable with increased client demand and adequate capacity,” Doyle explained.

He noted that, “In the April renewal period, US property cat reinsurance rates were flat, with some decreases for accounts without losses,” while “Loss impacted accounts averaged increases in the 10 to 20% range.”

Adding that, “I think both markets continued to stabilise, on average, in the quarter. And again, I would remind everyone, it’s a collection of markets, not a single market. That stabilisation is good for our clients and in some cases a better market has led to increased demand in both insurance and reinsurance.”

Dean Klisura, CEO of Guy Carpenter went into some more detail, saying, “Market conditions are stable, but we’re definitely seeing increased client demand to buy additional property cat limit, particularly at the top end of programmes. That was very pronounced throughout the first quarter, at 1/1, through the quarter, and certainly that trend continued on April 1st.”

Adding that his teams are seeing, “Strong capital inflows into the reinsurance market, driven by strong reinsurer returns, double digit returns in 2023.

“Reinsurer appetite is increased for property cat, there’s an inflow of capital and capacity, competition at the top end of programmes, it’s been good for both buyers and sellers in the marketplace.”

Looking ahead to the mid-year, Doyle explained, “Early signs for June 1 Florida cat risk renewals point to improve market conditions for cedents, increased reinsurance appetite for growth should be adequate to meet higher demand.”

Which is already being seen in early placements for the mid-year and the catastrophe bond market.

Reinsurance capacity levels are expected to be more than adequate, while differentiation will continue and loss impacted accounts are still likely to see the greatest chance of increases, it appears.

However, Marsh McLennan CEO Doyle also commented that, “I would also say that insurers and reinsurers are cautious about that rising cost of risk environment that I mentioned as well. And so, while again a stabilising market is better for our clients overall, I don’t expect that relative stability to change anytime soon, given some of the rising cost of risk issues that the insurance community is confronting today.”

This “relative stability” suggests that the appetites for risk may not increase so significantly at the lower-levels of reinsurance towers, which are again likely to prove the most stable of all the layers placed at 6/1 and 7/1 renewals.

Improved Florida cat reinsurance renewal conditions expected for June 1: MMC CEO was published by: www.Artemis.bm

Our catastrophe bond deal directory

Sign up for our free weekly email newsletter here.

Banque Bonhôte launches ESG fund strategy incorporating catastrophe bonds

This content is copyright to www.artemis.bm and should not appear anywhere else, or an infringement has occurred. Banque Bonhôte & Cie, a Swiss private bank, investment firm and wealth manager, has announced the launch of a new environmental, social and governance (ESG) focused fund strategy […]

Industry Loss WarrantyThis content is copyright to www.artemis.bm and should not appear anywhere else, or an infringement has occurred.

Banque Bonhôte & Cie, a Swiss private bank, investment firm and wealth manager, has announced the launch of a new environmental, social and governance (ESG) focused fund strategy that will incorporate catastrophe bonds as one of its allocations.

![]() Pierre-François Donzé, Head of Asset Management at Banque Bonhôte, said that, “Our approach and the integration of ESG criteria, is based on a quantitative allocation methodology to identify appropriate investment opportunities in the entire spectrum of the fixed income bond universe.”

Pierre-François Donzé, Head of Asset Management at Banque Bonhôte, said that, “Our approach and the integration of ESG criteria, is based on a quantitative allocation methodology to identify appropriate investment opportunities in the entire spectrum of the fixed income bond universe.”

The newly launched Bonhôte Selection Global Bonds ESG fund strategy does not follow a benchmark, instead leveraging quantitative methods to identify assets to invest in from the fixed income universe, based on indicators that define the attractiveness of one type of bond, over another.

These can range from the majority of the global fixed income universe, including sovereign bonds, investment-grade and high-yield corporate bonds.

But in addition catastrophe bonds are a specific asset class that will be targeted for this ESG focused investment fund strategy, the private bank explained.

The private bank notes that, catastrophe bonds, “Offer an advantageous risk/reward and provide useful diversification through a performance that is largely uncorrelated with conventional financial markets.”

Explaining that, “CAT bonds, which are part of the insurance-linked securities (ILS) category, are used by insurers and reinsurers to transfer the risks of predefined events to investors.”

The strategy has been optimised for investors whose reference currency is the Swiss franc and takes into account the cost of currency hedging as well.

The use of ESG criteria to identify opportunities is “a fundamental part of our investment strategy,” Banque Bonhôte & Cie said.

“The fund promotes environmental or social features, or a mix of the two, by investing in the vehicles and securities of issuers with an ESG profile above the median of their peers. Many controversial business activities and sectors are automatically excluded,” the company further explained.

Catastrophe bonds can be up to a maximum of 20% of the ESG investment fund strategy

Julien Stähli, Director of Investments, stated “This new fund gives pride of place to ESG criteria and marks a further step in our long-standing commitment to responsible investment and quantitative approaches.”

Donzé also said the approach taken, “Makes it possible to add value compared to strategies limited to a single market segment. The indicators used estimate the relative attractiveness of the various segments of the bond market on a historical basis.”

He also said that the Global Bonds ESG fund portfolio will be “dynamically rebalanced” when the indicators used suggest this is necessary.

It’s clear that Banque Bonhôte & Cie recognises the investment qualities of catastrophe bonds and the diversifying benefits they can deliver to portfolios, as well as the inherent ESG qualities given their role in the provision of critical disaster risk financing to support the global insurance and reinsurance industry.

As we previously reported, Banque Bonhôte & Cie had said before that catastrophe bonds, as an asset class, exhibits the rare property of price moves that are independent of broader financial markets and so can be considered “the only true source of diversification.”

Banque Bonhôte launches ESG fund strategy incorporating catastrophe bonds was published by: www.Artemis.bm

Our catastrophe bond deal directory

Sign up for our free weekly email newsletter here.