SCOR forecasts “persistent underwriting discipline” at June and July renewals

This content is copyright to www.artemis.bm and should not appear anywhere else, or an infringement has occurred. France-headquartered global reinsurance firm SCOR is forecasting that the market will maintain its discipline at the upcoming June and July renewals, as the company continued to take advantage […]

Industry Loss WarrantySwiss Re continues growth at April renewals, as nat cat drives rate increases

This content is copyright to www.artemis.bm and should not appear anywhere else, or an infringement has occurred. Global reinsurance company Swiss Re continued to expand its business at the recent April renewals, underwriting 6% more in treaty premium volumes, at US $2.5 billion, which price […]

Industry Loss WarrantyFlorida Citizens expects slightly higher risk transfer rate-on-line for 2024

This content is copyright to www.artemis.bm and should not appear anywhere else, or an infringement has occurred. Florida’s Citizens Property Insurance Corporation, the state’s insurer of last resort that is currently in the catastrophe bond market with a new issuance that could approach $1.25 billion […]

Industry Loss Warranty

SCOR forecasts “persistent underwriting discipline” at June and July renewals

This content is copyright to www.artemis.bm and should not appear anywhere else, or an infringement has occurred. France-headquartered global reinsurance firm SCOR is forecasting that the market will maintain its discipline at the upcoming June and July renewals, as the company continued to take advantage […]

Industry Loss WarrantyThis content is copyright to www.artemis.bm and should not appear anywhere else, or an infringement has occurred.

France-headquartered global reinsurance firm SCOR is forecasting that the market will maintain its discipline at the upcoming June and July renewals, as the company continued to take advantage of market conditions to grow so far this year.

At the April reinsurance renewals, SCOR said that it grew its book of renewed premiums by 17%, while rates continued to improve for the company, especially in its non-proportional reinsurance book.

At the April reinsurance renewals, SCOR said that it grew its book of renewed premiums by 17%, while rates continued to improve for the company, especially in its non-proportional reinsurance book.

In announcing its first-quarter 2024 results this morning, SCOR said that its group net income rose to EUR 196 million for the period, while insurance revenue rose 6% to EUR 4.113 billion and the P&C reinsurance combined ratio was attractive at 87.1%.

Thierry Léger, Chief Executive Officer of SCOR, said, “For the first quarter of the Forward 2026 strategic plan, SCOR publishes a strong net income of EUR 196 million. In P&C, we are reaping the benefits of the very attractive market conditions with a combined ratio of 87.1% and we remain determined on building reserve buffers. In L&H, we are impacted by an adverse experience variance, mainly driven by US mortality and claims reporting effects. In Investments, SCOR benefits from elevated regular income yield and reinvestment rates. Overall, we are starting the year with a high ROE of 17.3% and an improved solvency ratio of 215% supported by strong operating capital generation driven by P&C January renewals.”

Like all the other major reinsurance firms, the profitability achieved at renewals flows through into strong cash generation across the year and with prices still rising each year at renewals, these effects are not yet ready to tail off.

P&C re/insurance was assisted by a low natural catastrophe loss ratio of 7.2%, despite SCOR (like others) raising its estimate for last year’s Italian severe weather and hailstorm, which the industry has raised estimates for.

At the recent April 1 reinsurance renewals, SCOR said it continued to grow in preferred lines.

Notably, SCOR maintained the terms and conditions on renewal business, as well as the improved profitability being seen.

Estimated gross premiums written increased by 17% at April 1, with SCOR’s Alternative Solutions book almost doubling and specialty lines business increasing by almost 23%.

SCOR said that the pricing trend observed in January was maintained in April, with a +3.2% price change overall.

On a technical basis, SCOR says rate will drive an improvement of -1.5% to the underwriting ratio.

“In this very positive environment, SCOR anticipates continued underwriting discipline for the upcoming June and July renewals,” the company said.

This has been the view of the big four reinsurance firms in their Q1 2024 reporting, that market conditions have eased, but there has been no change in the levels of attachment, the strength of terms, or in the rates being paid.

We just aren’t seeing the rapid acceleration in rates that were seen before, but at these high levels reinsurance remains an extremely profitable business, while major losses remain absent from the market.

SCOR said it has not changed its approach to natural catastrophe business at the recent April renewals, resulting in a reduced relative size of that segment in its renewed portfolio after 4/1.

With more opportunities to grow at the June and July reinsurance renewals, it’s expected SCOR will continue to deploy more capacity to build its book of premiums further, while market conditions remain so conducive to do so.

SCOR forecasts “persistent underwriting discipline” at June and July renewals was published by: www.Artemis.bm

Our catastrophe bond deal directory

Sign up for our free weekly email newsletter here.

Swiss Re continues growth at April renewals, as nat cat drives rate increases

This content is copyright to www.artemis.bm and should not appear anywhere else, or an infringement has occurred. Global reinsurance company Swiss Re continued to expand its business at the recent April renewals, underwriting 6% more in treaty premium volumes, at US $2.5 billion, which price […]

Industry Loss WarrantyThis content is copyright to www.artemis.bm and should not appear anywhere else, or an infringement has occurred.

Global reinsurance company Swiss Re continued to expand its business at the recent April renewals, underwriting 6% more in treaty premium volumes, at US $2.5 billion, which price increases so far this year have been most significant in the natural catastrophe business.

![]() Swiss Re reported group net income of $1.1 billion this morning, with its property and casualty reinsurance business contributing $552 million of it at a combined ratio of 84.7%.

Swiss Re reported group net income of $1.1 billion this morning, with its property and casualty reinsurance business contributing $552 million of it at a combined ratio of 84.7%.

So far this year, Swiss Re’s P&C reinsurance business has not experienced many large losses above $20 million, so the combined ratio is well within the full-year target of 87%.

However, the company’s CFO revealed a $100 million net and around $77 million gross impact from the Baltimore Bridge collapse, which affected P&C Re.

P&C reinsurance revenues continue to be driven by the strong price increases achieved at renewal rounds, although denting the IFRS 17 insurance service result after the first-quarter were some reserve additions made for large prior-year natural catastrophe and man-made loss events, as well as specific reserve additions for the pre-2020 US liability book.

Swiss Re’s Group Chief Executive Officer Christian Mumenthaler commented, “Swiss Re had a good start to the year, with all our main businesses posting strong results. This reflects continued underwriting discipline, a strong return on investments and effective management of operating expenses.”

With around 65% of Swiss Re’s reinsurance treaty business now renewed after April, the company said this equated to an 8% increase in treaty premium volumes and a +10% price increase so far this year.

At the April 1st renewals, Swiss Re renewed $2.5 billion in reinsurance premiums, which was up 6% on the prior year and saw a 12% price increase across the renewal book.

However, loss assumptions also increased 12%, as Swiss Re continued to take a “prudent view on inflation and updated loss models” the reinsurer explained.

Price increases this year so far have been most pronounced in property catastrophe reinsurance business renewed, Swiss Re explained this morning.

However, while price increases were 10% across the 2024 renewal portfolio, loss assumptions have been raised 12%, driving a -2% net price change and showing that inflationary effects and views on risk suggest little ambition to return to softening of prices.

At April 1st, Swiss Re grew its property and specialty books by 21%, while casualty shrank -27%.

Year-to-date, nat cat business grew +12% and Swiss Re said that it saw rate improvements here, but “discipline was maintained on attachment point.”

CFO John Dacey said that the Swiss Re book is around 5% bigger year-on-year, across the business.

CEO Christian Mumenthaler said, “The strong earnings in the first quarter have given Swiss Re a positive start to the year as we continue to focus on our 2024 targets, including a net income of more than USD 3.6 billion. Underwriting discipline, coupled with a favourable market environment, underpin our confidence.”

The company also announced this morning that Ivan Gonzalez, CEO Reinsurance China, has now been appointed CEO Corporate Solutions, succeeding Andreas Berger who will become group CEO as Mumenthaler departs this year.

In addition, the company said that Moses Ojeisekhoba, CEO Global Clients and Solutions and former reinsurance leader at the firm, is now set to depart the company to pursue other opportunities outside Swiss Re.

Swiss Re continues growth at April renewals, as nat cat drives rate increases was published by: www.Artemis.bm

Our catastrophe bond deal directory

Sign up for our free weekly email newsletter here.

Florida Citizens expects slightly higher risk transfer rate-on-line for 2024

This content is copyright to www.artemis.bm and should not appear anywhere else, or an infringement has occurred. Florida’s Citizens Property Insurance Corporation, the state’s insurer of last resort that is currently in the catastrophe bond market with a new issuance that could approach $1.25 billion […]

Industry Loss WarrantyThis content is copyright to www.artemis.bm and should not appear anywhere else, or an infringement has occurred.

Florida’s Citizens Property Insurance Corporation, the state’s insurer of last resort that is currently in the catastrophe bond market with a new issuance that could approach $1.25 billion in size, expects that the rate-on-line across its reinsurance and risk transfer purchases for the 2024 hurricane season could be slightly higher than the prior year.

![]() This despite the Florida reinsurance renewals expected to range from down -5% to up +5% this year, Florida Citizens CFO Jennifer Montero explained today during a Board meeting.

This despite the Florida reinsurance renewals expected to range from down -5% to up +5% this year, Florida Citizens CFO Jennifer Montero explained today during a Board meeting.

Montero explained how reinsurance market conditions are looking as the mid-year renewals fast-approach, noting that appetites for risk have adjusted in recent months.

She said that, “The reinsurance markets are better than last year but have significantly changed since the beginning of the year. There were significant amounts of capital invested in reinsurance markets in the last quarter of 2023, as interest rates were starting to come down with the expectation of Fed rate cuts.

“However, as inflation continued the Fed changed its stance to higher-for-longer and now investors are trying to capitalise on higher rates.

“Therefore, they’ve been moving some of the capital from reinsurance markets to alternative investments, including private credit where their returns are higher.”

Which is an interesting and notable observation from Montero, especially given the recent trend towards spread widening and higher issuance pricing in the catastrophe bond market, where investors have certainly upped their return requirements in the last few weeks.

Montero also noted that coastal and catastrophe exposed reinsurance buyers are purchasing more cover in 2024, particularly the residual markets, such as in Texas, Louisiana, California and Florida, given their escalating exposure levels, but also in Florida specifically because government-backed reinsurance layers the RAP and FORA have not been continued this year, so demand is up and capacity as a result remains constrained.

Highlighting the role of exposure and inflation in this, Montero said, “Citizens’ exposure grew by 31% in 2023, and is expected to grow by 7% this year, even though we expect only a slight change in the policy count in 2024.”

That has driven Citizens significant need for reinsurance this year, with $5.5 billion from its catastrophe bonds and reinsurance program needed this year.

As we reported earlier today, Citizens needs to increase its budget for risk transfer to $750 million in 2024, up from around $650 million a year earlier.

The exposure growth is the main driver, as well as the fact much more protection is required to cover that.

At the Board meeting, the increased budget was approved, Artemis can report, which is a maximum that Citizens staff can spend up to, to secure the necessary $5.5 billion cat bond and reinsurance tower.

Montero pointed out that Citizens can and will walk away, if it feels it cannot buy the protection at prices it deems to be reasonable, so if the market were to suddenly harden further specific purchases could shrink, or spend by shifted, or the entire buy be downsized, as we saw in 2022.

As well as needing to buy much more, to cover its higher insured values, Florida Citizens staff also expect a slightly higher rate-on-line will need to be paid across the reinsurance program.

Montero said that the rate-on-line (ROL) is expected to be 13% for the reinsurance and cat bond purchases this year, at the $750 million budget level to buy up to $5.5 billion of protection needed.

That’s up from a reported 12.69% for 2023, when much less protection was required.

But, it’s important to also remember that Florida Citizens merged its coastal, personal and commercial accounts into a single reinsurance tower, the Citizens Account, for 2024.

So the way the reinsurance is bought has changed quite significantly this year, which could also drive some adjustments to how the rates flow across the cat bond and reinsurance purchases.

Also read:

– Florida Citizens budget for 2024 cat bonds & reinsurance lifts to $750m max.

– Florida Citizens sets up to $1.25bn target for new Everglades catastrophe bond.

Florida Citizens expects slightly higher risk transfer rate-on-line for 2024 was published by: www.Artemis.bm

Our catastrophe bond deal directory

Sign up for our free weekly email newsletter here.

Cat bonds are only new capital. Retro recovery likely for Baltimore Bridge: Hannover Re

This content is copyright to www.artemis.bm and should not appear anywhere else, or an infringement has occurred. Executives from global reinsurance firm Hannover Re said today that there is no sign of new capital in the reinsurance market aside from through the catastrophe bond sector […]

Industry Loss WarrantyThis content is copyright to www.artemis.bm and should not appear anywhere else, or an infringement has occurred.

Executives from global reinsurance firm Hannover Re said today that there is no sign of new capital in the reinsurance market aside from through the catastrophe bond sector and some unlocked trapped collateral, and also discussed the Baltimore Bridge collapse saying that retrocession recoveries are anticipated.

Speaking during the firm’s first-quarter earnings call, Hannover Re CEO Jean-Jacques Henchoz said that reinsurance remains in a stable market environment.

Speaking during the firm’s first-quarter earnings call, Hannover Re CEO Jean-Jacques Henchoz said that reinsurance remains in a stable market environment.

“Generally, there is a stable environment as you’ve seen. We’re very happy with rate adequacies. We will see that programmes are being filled, but there is more of an equilibrium in supply and demand at this stage,” Henchoz said.

He went on to say that there are, “No significant new entrants in the P&C reinsurance space, so, the outlook is for more of the same with a stable perspective in the P&C market and my sense is that the same is true at this stage for the outlook for 2025.”

Also speaking during the earnings call, Sven Althoff, Member of the Executive Board for P&C at Hannover Re discussed the state of the reinsurance market.

“I mean, we are still not seeing new capital entering the market with maybe the exception of the cat bond space.

“So, the increase in capacity we are observing in the market is coming from net retained earnings, or collateral that becomes un-trapped,” Althoff said.

Adding that, “From the existing market players all the macro drivers are still there, with climate change, geopolitical uncertainty, and still above the long-term average inflationary environment.

“So, that would imply that the existing market players will continue to look for similar levels of profitability compared to where we are today from a pricing point of view. And then, of course, a lot will depend on what 2024 will produce as far as losses. And I would expect that the markets will continue to react to significant loss development, wherever it may arise.”

Asked about Hannover Re’s major losses from the first-quarter, Althoff went on to discuss the Baltimore Bridge ship collision that resulted in the collapse of the main span.

As we reported earlier, the reinsurer reported net large losses for Q1 of EUR 52 million.

However, the company has booked its full loss budget for the quarter anyway, of EUR 378 million, but has not yet supplied a loss estimate for the Baltimore Bridge collapse.

But Hannover Re said it expects the net impact will be contained within that budget amount, which suggests the net maximum could be as much as EUR 326 million, after any retrocessional effects.

Althoff commented this morning that, “There are still uncertainties given the complexity of the claim, the root cause of the claim. So, therefore, we have not allocated any reserves to specific segments or contracts at this stage.

“But your assumption is correct, that we do expect retro recoveries on the marine side where we have significant retrocessional protection, further down the line. We’ll be able to share more details in Q2.”

It’s possible therefore that Hannover Re could share some percentage of the Baltimore Bridge collapse loss with third-party capital backing its K-Cession quota share sidecar like structure, as that has historically contained some specialty lines risks, such as marine.

Cat bonds are only new capital. Retro recovery likely for Baltimore Bridge: Hannover Re was published by: www.Artemis.bm

Our catastrophe bond deal directory

Sign up for our free weekly email newsletter here.

Hannover Re says reinsurance stabilised at high level, shares no losses with ILS

This content is copyright to www.artemis.bm and should not appear anywhere else, or an infringement has occurred. Global reinsurance company Hannover Re expects that the current “high levels” seen in the reinsurance industry can be sustained and it does not expect much change at upcoming […]

Industry Loss WarrantyThis content is copyright to www.artemis.bm and should not appear anywhere else, or an infringement has occurred.

Global reinsurance company Hannover Re expects that the current “high levels” seen in the reinsurance industry can be sustained and it does not expect much change at upcoming renewals.

In announcing its first-quarter results today, Hannover Re also revealed that, thanks to a more benign quarter of natural catastrophe losses the company did not share any of its major losses with insurance-linked securities (ILS) investors during the period.

In announcing its first-quarter results today, Hannover Re also revealed that, thanks to a more benign quarter of natural catastrophe losses the company did not share any of its major losses with insurance-linked securities (ILS) investors during the period.

Hannover Re reported that its group net income rose by 15% to EUR 558 million in Q1 2024, while its reinsurance revenue rose to EUR 6.7 billion.

As a result, return on equity reached 21.3%, which was well-above the target of 14% set under the reinsurance firm’s strategy.

In property and casualty reinsurance, Hannover Re’s combined ratio came down from 92.3% a year ago, to just 88% for Q1 2024, which is below the full-year target of 89%.

As a result, major losses fell well within budget for the quarter and the natural catastrophe experience was not significant to Hannover Re’s business.

“We can look back on a rather benign quarter as regards large losses. We had a good start into the year, putting us on track to achieve our full-year profit target,” Jean-Jacques Henchoz, Chief Executive Officer of Hannover Re commented. “At the same time, with the recent treaty renewals we have put in place a solid foundation for further profitable growth given the continued demand for high-quality and reliable risk protection in what is a challenging landscape.”

In P&C reinsurance, Hannover Re noted some growth in the area of structured transactions and insurance-linked securities (ILS), particularly in EMEA and the Americas.

This is where the reinsurers business that sees it retroceding risk to ILS investors is undertaken, as the company continues to front and transform risk for capital market investors.

Large losses came in at EUR 52 million for the period, although Hannover Re has not put a figure on its loss from the Baltimore Bridge collision, but it has booked the full budget for the quarter anyway, of EUR 378 million, and said that event will be easily covered.

In the quarter, Hannover Re noted a “low retrocession recovery” with no positive impact from the large losses booked, that came in below budget.

Gross large losses were booked at EUR 59 million, net at the aforementioned EUR 52 million, but Hannover Re also noted that the share of loss for ILS investors was zero in the period, as none of the events were severe enough to attach the ILS contracts Hannover Re has facilitated and partnered on.

The Japanese earthquake at the beginning of the year only resulted in a net loss of EUR 25 million, while wildfires in Chile cost EUR 15.8 million. In addition there was an aviation loss at EUR 11.7 million.

Looking to the full-year, Hannover Re expects positive conditions to persist in reinsurance, forecasting that its reinsurance revenue in total business will grow by more than 5% this year, at constant exchange rates, while group net income is forecast to reach at least EUR 2.1 billion.

CEO Henchoz commented on market conditions, saying, “The 1 April renewals provided further confirmation that the market environment has stabilised on a high level after the substantial improvements in prices and conditions recorded in prior years.

“We are optimistic that this level can be sustained in the coming renewals as well. It remains the case that our clients value our quality as a strong partner and our focus on our core expertise, namely reinsurance.”

Hannover Re says reinsurance stabilised at high level, shares no losses with ILS was published by: www.Artemis.bm

Our catastrophe bond deal directory

Sign up for our free weekly email newsletter here.

AmCoastal extends reinsurance tower to $1.2bn thanks to new cat bond: CEO

This content is copyright to www.artemis.bm and should not appear anywhere else, or an infringement has occurred. Thanks to the recent successful issuance of its latest catastrophe bond, American Coastal Insurance (AmCoastal) has extended the top exhaustion point of its main catastrophe reinsurance tower to […]

Industry Loss WarrantyThis content is copyright to www.artemis.bm and should not appear anywhere else, or an infringement has occurred.

Thanks to the recent successful issuance of its latest catastrophe bond, American Coastal Insurance (AmCoastal) has extended the top exhaustion point of its main catastrophe reinsurance tower to roughly $1.2 billion for 2024, according to CEO Dan Peed.

As Artemis had reported, AmCoastal successfully secured an upsized $200 million Armor Re II Ltd. (Series 2024-1) Florida named storm cat bond in April, finalising the deal with a risk spread within the lower-half of the initial range of price guidance.

As Artemis had reported, AmCoastal successfully secured an upsized $200 million Armor Re II Ltd. (Series 2024-1) Florida named storm cat bond in April, finalising the deal with a risk spread within the lower-half of the initial range of price guidance.

The insurer has now disclosed that the catastrophe bond occupies roughly two-thirds of the top-layer of the main AmCoastal catastrophe reinsurance tower for 2024.

During the insurer’s earnings call yesterday, CEO Dan Peed commented on the reinsurance renewal saying, “We have increased our multi-year reinsurance commitments, enhancing stability. Our 2024 catastrophe reinsurance program was marketed with a structure that further protects the balance sheet.”

Adding that, “We have been able to increase the expected exhaustion point with the successful placement of AmCoastal’s multi-year cat bond which was oversubscribed at the lower end of the expected coupon range.”

AmCoastal President Brad Martz went into more detail on the reinsurance tower renewal, explaining, “As of today, we have secured over 90% of the total limit being sought, and the placement is progressing in line with our expectations.”

He said that AmCoastal had three goals when it began planning its reinsurance renewal for the 2024 hurricane season, to increase the overall protection, improve cost efficiency, and maintain similar levels of retention.

“I believe we will achieve all three this year,” Martz said.

“For American Coastal, we are seeking to purchase roughly $265 million more limit from the private market this year, which will stretch our exhaustion point up closer to $1.2 billion, for the 208-year return time compared to the expiring program of 167-year return time as estimated by the AIR hurricane model.

“$200 of the additional open market limit was secured in a new three-year catastrophe bond that closed in April,” he commented.

Martz also noted that AmCoastal’s quota share reinsurance is being reduced from 40% to 20%, which should drive “a material increase in net premiums earned, partially offset by higher net losses, as we retain more of those.”

The goal with the new reinsurance strategy is to “retain more of our gross underwriting margin,” Martz said.

He added that, “We expect to have both towers fully-placed well before June 1st and we will provide more information on the final limits, retentions, and costs, once both programs have been completed.”

You can see the new AmCoastal 2024 reinsurance tower below.

You can read all about AmCoastal’s new Armor Re II Ltd. (Series 2024-1) catastrophe bond transaction and every other cat bond ever issued in our Artemis Deal Directory.

AmCoastal extends reinsurance tower to $1.2bn thanks to new cat bond: CEO was published by: www.Artemis.bm

Our catastrophe bond deal directory

Sign up for our free weekly email newsletter here.

Parametric structures minimise or eliminate limitations of ILWs: Skyline Partners

This content is copyright to www.artemis.bm and should not appear anywhere else, or an infringement has occurred. Industry loss warranties (ILWs) remain a useful and well-established instrument within the capital management toolbox of risk carriers, but do have their drawbacks, some of which can be […]

Industry Loss WarrantyThis content is copyright to www.artemis.bm and should not appear anywhere else, or an infringement has occurred.

Industry loss warranties (ILWs) remain a useful and well-established instrument within the capital management toolbox of risk carriers, but do have their drawbacks, some of which can be mitigated or removed entirely by a parametric structure, according to Skyline Partners.

![]() As parametric insurance, reinsurance, and retrocession structures continue to grow in popularity, Artemis spoke with Laurent Sabatié, Co-founder and Executive Director, and Ken MacDonald, Strategic Advisor of Skyline Partners, a full-service provider in the parametric insurance supply chain.

As parametric insurance, reinsurance, and retrocession structures continue to grow in popularity, Artemis spoke with Laurent Sabatié, Co-founder and Executive Director, and Ken MacDonald, Strategic Advisor of Skyline Partners, a full-service provider in the parametric insurance supply chain.

ILWs are an indexed-based reinsurance instrument which pays out when the estimated total industry-wide insured loss arising from a specific, covered event or group of events exceeds an agreed threshold, as calculated by a third party.

They can be used to cover a dead or live cat event, and Sabatié explained are often purchased by cedants as a back-up cover to protect their balance sheets when multiple sequential events during the same storm season occur or are feared.

But while ILWs are both useful and well-established, Sabatié stressed that they’re certainly not without their limitations, including the issue of basis risk.

“They typically use market-loss data compiled by commercial entities or major reinsurers to determine when an ILW is triggered for payment. This is inherently inconsistent with any specific cedant’s actual value at risk. The inconsistency is exacerbated by reporting gaps which leave total losses underestimated or based on guesswork,” said Sabatié.

“Perhaps worse is the long wait for settlement,” he continued. “ILWs – by design – do not pay until the industry loss has settled, or at least comfortably exceeds the trigger point. The naturally long period required to calculate a reliable industry loss can, in the extreme, be many years. In the interim, the cedant may not be able even to recognise the reinsurance recovery in their P&L.”

Expanding on the limitations and issues surrounding ILWs, MacDonald highlighted both a lack of flexibility and a potential lack of transparency.

“Their structure is very rigid, with trigger conditions that take no account, for example, of variations in risk profiles across portfolios, or the evolving nature of tropical cyclone risk.

“The ILW market operates predominantly as an over-the-counter market, with limited regulatory oversight, and therefore transparency, relative to traditional reinsurance markets,” said MacDonald.

Another negative, according to Sabatié and MacDonald, include the fact the scope of the ILS coverage is limited geographically, as areas not covered by third-party industry loss collation services cannot be covered by ILW instruments.

Further, calculation of total loss is often underestimated because certain types of losses may be excluded from industry loss calculations, explained the pair.

According to Sabatié and MacDonald, the answer to these limitations with ILWs, is the parametric structure, which does share some characteristics with ILWs.

“They too can be index based, but they are triggered for payment when a specified event occurs, with no regard for the total (and irrelevant) industry loss arising from the event. They minimise or eliminate many of the issues associated with ILWs,” said Sabatié.

Starting with the basis risk issue, Sabatié told Artemis that parametric triggers can reduce basis risk as they can be designed to align very closely with the actual damages caused by an event to a specific re/insured portfolio.

“Through pre-event analysis of its exposed values and location coordinates, coverage can be designed to react with precision to relevant events, reducing basis risk substantially compared to ILWs.

“The trigger events – or “parameters” – of the index, and the loss scales created and adopted for a specific coverage contract, can each be calibrated to minimise remaining basis risk. This may apply, for example, to the intensity triggers of the index such as windspeed, days of excess temperature, or the order of the event during a coverage period. Adjustment can be used to ensure triggers align with cedant objectives regarding the attachment and/or exhaustion probability of specific economic loss tranches, as well as budget,” said Sabatié.

Adding, “This alignment ensures triggers match the modelled cat losses used in reinsurance purchasing and capital modelling. The parameters can even be optimised to align with the distribution probability of the cat losses that inform not just the overall reinsurance placement, but also the capital modelling behind it. They are, therefore, fully integrated within the purchaser’s enterprise risk management framework.

“Alignment makes the value of parametric coverage is much greater, because it focusses more accurately on the reinsured’s specific exposures, not those of the entire industry.”

Another benefit of a parametric structure is that claims settlement is extraordinary efficient, with settlement often within a calendar month of the triggering loss event.

“Reduced administrative burdens provide faster, certain access to funds underpinning liquid capital. The beneficial financial impact of parametric reinsurance can be recognised much faster,” said MacDonald.

“Settlement is much simpler than with traditional indemnity-based reinsurance, which may also be said of ILWs, but with parametric reinsurance payments are not delayed while industry-level losses are calculated and left to develop. Nor does inflation decrease the relative value of the recovery while you wait.

“This lightning speed of settlement also benefits reinsurance capital providers by eliminating trapped capital and removing concerns over loss creep,” he continued.

The flexibility of parametric structures, explained Sabatié, means that coverage can be tailored to match the risk, which ensure better pricing as cedants pay solely for protection that matches their exposure precisely.

Additionally, Sabatié noted that coverage is broader than with an ILW, as any type of economic loss with a covered event may be reimbursed by a parametric reinsurance structure, including intangible exposures such as loss of access.

“Parametric triggers are highly flexible and can be tailored to respond to parameters which precisely meet each cedant’s specific needs. Triggers may take into account factors such as geographic location, risk profile, historical incidence, and/or almost anything which can be shown to contribute to loss and quantified. Payment structures can be varied to account for changing values at risk, or future changes of conditions. Risk nuances can therefore be measured more effectively and covered more advantageously. Nor is parametric reinsurance limited to nat cat exposures. It has been used to reinsure perils ranging from cyber to marine cargo,” said Sabatié.

Commenting on some additional, major benefits of a parametric structure, MacDonald explained that, “Parametric reinsurance structures typically operate in well-established regulated markets which ensures greater transparency and oversight relative to ILWs. Insurers can therefore gain access to a broader range of potential counterparties, and benefit from the expertise and financial strength of established reinsurance players. Most of them are already active in parametric.”

He also underlined that regulated parametric products do not rely on uncertain Letters of Credit or unrated capital, which gives cedants reassurance over the reliability and stability of their reinsurance arrangements.

“With lower basis risk, better counterparties, closer alignment with modelled outcomes, and a regulated nature, parametric reinsurance qualifies as Tier 2 Capital under European solvency rules. This is in stark contrast to ILWs which are considered derivative products,” said MacDonald.

“In Parametric vs. ILW, parametric reinsurance wins on transparency, certainty, responsiveness, simplicity, speed of payment, and balance-sheet benefits. Skyline Partners, the parametric catalyser, has everything it takes to get parametric reinsurance structures designed, built, and operational. We work daily with brokers, cedants, captives, and reinsurers alike to deliver the winning parametric advantage,” concluded Sabatié and MacDonald.

It’s important to note that ILW’s and parametrics both play an important role and are well-suited to specific situations, with some protection buyers even using the structures to complement each other within their coverage arrangements.

We suspect both will continue to play these important roles, but as technology advances and use of data becomes increasingly sophisticated, the basis risk associated with them will increasingly be minimised and the structures themselves refined, with their protection honed and improved.

Parametric structures minimise or eliminate limitations of ILWs: Skyline Partners was published by: www.Artemis.bm

Our catastrophe bond deal directory

Sign up for our free weekly email newsletter here.

Zero appetite to weaken terms & conditions, reduce attachments: Munich Re CFO

This content is copyright to www.artemis.bm and should not appear anywhere else, or an infringement has occurred. There is zero appetite at reinsurance giant Munich Re to budge on attachment points or weaken any terms and conditions, the firm’s CFO Christoph Jurecka explained today. As […]

Industry Loss WarrantyThis content is copyright to www.artemis.bm and should not appear anywhere else, or an infringement has occurred.

There is zero appetite at reinsurance giant Munich Re to budge on attachment points or weaken any terms and conditions, the firm’s CFO Christoph Jurecka explained today.

As we reported this morning, Munich Re had a very strong first-quarter to 2024 and said that April reinsurance renewals were positive in terms of volumes, but flatter in terms of rates.

As we reported this morning, Munich Re had a very strong first-quarter to 2024 and said that April reinsurance renewals were positive in terms of volumes, but flatter in terms of rates.

The company also said it anticipates positive renewals at the mid-year, despite a recognition that market pressure is rising in the reinsurance space.

Asked during an investor call this morning whether Munich Re expects any pressure on its terms, in particular whether it foresees any decline in reinsurance contract attachment points, the firm’s CFO Christoph Jurecka said there is zero chance.

Instead, the company is hoping for a stable outlook in reinsurance through 2024, on both price and terms.

That means no loosening of underwriting terms and conditions, on which Jurecka was very clear.

In response to an investment analysts question about whether Munich Re would consider reducing attachment points for its clients, Jurecka said, “Lower attachment points, or these kinds of things, is clearly nothing we would want to go into.”

He went on to explain that Munich Re would, “Rather really focus on maintaining the improved terms and conditions and then continuing to write business at the attractive price level, of where we currently are.”

Commenting on the stabilisation of the reinsurance price environment , Jurecka said, “It seems as if we are on a plateau level for 1-1 and 1-4 now, from a pricing perspective, where supply and demand met each other at very reasonable terms.”

Adding that, looking forwards on price expectations for renewals, “I would just assume that continues.”

Jurecka then reiterated the importance of discipline, especially on terms and conditions.

Telling the analyst, “Then again, our appetite to weaken some of our T&C’s. or to be looser on the underwriting side, the appetite is absolutely zero and the discipline needs to be maintained going forward.”

Zero appetite to weaken terms & conditions, reduce attachments: Munich Re CFO was published by: www.Artemis.bm

Our catastrophe bond deal directory

Sign up for our free weekly email newsletter here.

Munich Re: Reinsurance market pressure rising, but positive July renewals expected

This content is copyright to www.artemis.bm and should not appear anywhere else, or an infringement has occurred. Global reinsurance giant Munich Re has noted a slight increase in market pressure after the April round of renewals, but believes that the overall market environment will remain […]

Industry Loss WarrantyThis content is copyright to www.artemis.bm and should not appear anywhere else, or an infringement has occurred.

Global reinsurance giant Munich Re has noted a slight increase in market pressure after the April round of renewals, but believes that the overall market environment will remain positive at the next major reinsurance renewals in July.

![]() In announcing a stellar result for the first-quarter of 2024 this morning, when its business generated an impressive €2.1 billion net result, Munich Re said that it anticipates continued good momentum, helped by positive opportunities to deploy its capacity.

In announcing a stellar result for the first-quarter of 2024 this morning, when its business generated an impressive €2.1 billion net result, Munich Re said that it anticipates continued good momentum, helped by positive opportunities to deploy its capacity.

Also assisting in the strong result was a very low combined ratio in property and casualty reinsurance, of just 75.3%, as overall major losses fell year-on-year, helped by a lower level of natural catastrophe loss events in the quarter.

“Munich Re kicked off the new financial year with great momentum. Our Q1 net result this year is nearly 70% higher than in 2023. Every line of business played a role in this impressive performance. In addition, we got a boost from the treaty renewals at 1 April, where we tapped into attractive growth opportunities against a backdrop of continuing high rates. We still expect to generate a profit of €5bn in 2024. In fact, it has become more likely that we will surpass that target,” Christoph Jurecka, CFO of Munich Re explained.

Property-casualty reinsurance generated a net result of €1.336 billion, up strongly from the prior year’s €760 million.

Major losses fell to €650 million, from over one billion euros in the prior year, with man-made major losses rising to €418 million due to the inclusion of the collapse of the Francis Scott Key Bridge in Baltimore, while catastrophe losses fell significantly to €232 million, down from €870 million in the previous year period.

At the latest reinsurance renewals on April 1st 2024, Munich Re grew the volume of business written to €2.6 billion, a 6.1% increase.

The reinsurer said it “exploited the ongoing favourable market conditions to expand attractive business, with growth opportunities being realised particularly in India, Latin America and Europe.”

Price development was stable overall, largely compensating for higher loss estimate trends, Munich Re said.

Interestingly though, Munich Re notes, “market pressure increasing slightly” at the renewals.

This reflects the increased appetite of reinsurers and capital markets players, as well as higher available capacity in the reinsurance market, we expect.

We also suspect this is in part due to higher competition, as reinsurers are keen to maximise their opportunity in the hard market environment, in case softening ensues.

Looking ahead though, it seems Munich Re is not anticipating any significant reversal in market conditions.

The company said, “Munich Re expects the environment to remain positive in the upcoming July renewal round.”

In fact, Munich Re said that it anticipates “sustained advantageous business opportunities in coming quarters,” and as a result says the chance it surpasses its full-year profit guidance of €5 billion has now risen, after the strong start to the year.

Munich Re: Reinsurance market pressure rising, but positive July renewals expected was published by: www.Artemis.bm

Our catastrophe bond deal directory

Sign up for our free weekly email newsletter here.

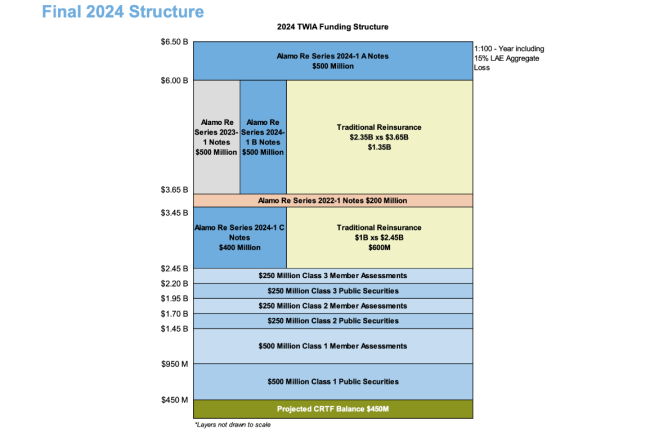

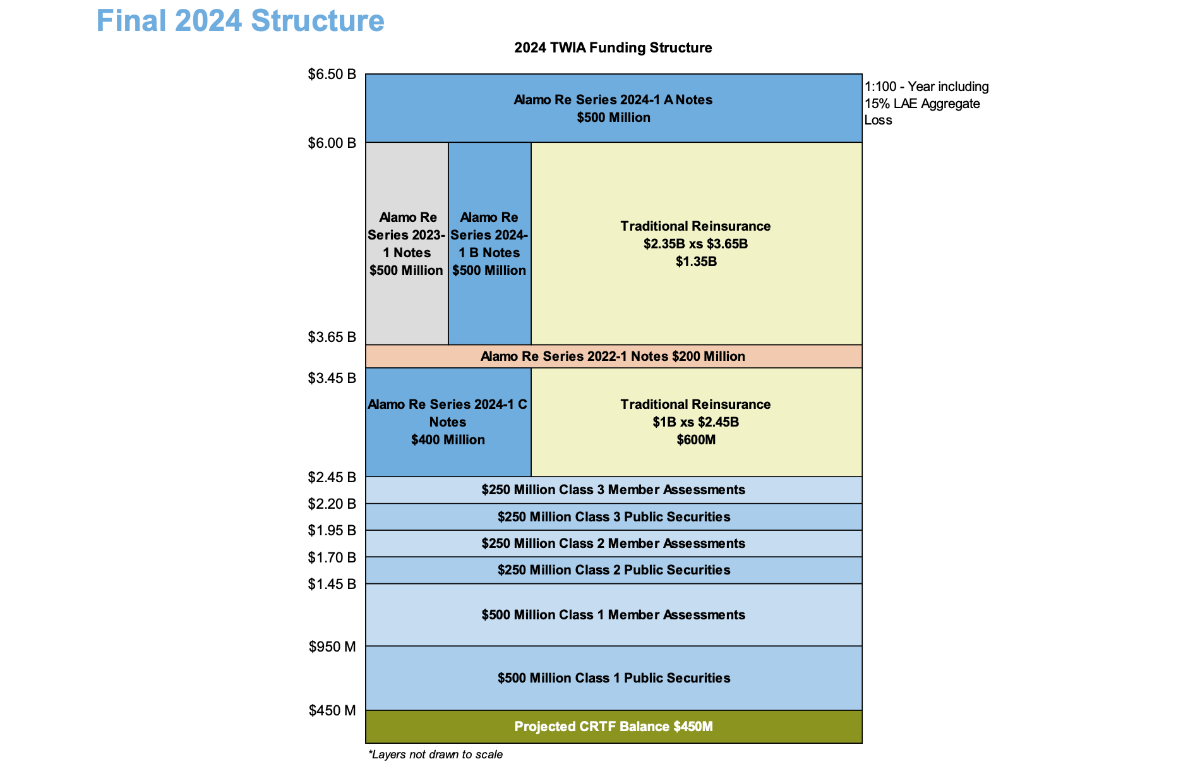

Texas Windstorm (TWIA) ready to sign reinsurance renewal lines this week

This content is copyright to www.artemis.bm and should not appear anywhere else, or an infringement has occurred. Having already secured its largest ever catastrophe bond issue this year, the Texas Windstorm Insurance Association (TWIA) is now ready to sign lines for its reinsurance renewal, with […]

Industry Loss WarrantyThis content is copyright to www.artemis.bm and should not appear anywhere else, or an infringement has occurred.

Having already secured its largest ever catastrophe bond issue this year, the Texas Windstorm Insurance Association (TWIA) is now ready to sign lines for its reinsurance renewal, with support secured for the rest of its capacity needs, according to staff and broker Gallagher Re’s executives.

At a Board meeting of the Texas Windstorm Insurance Association (TWIA) today, an update on the reinsurance and funding for 2024 was provided.

At a Board meeting of the Texas Windstorm Insurance Association (TWIA) today, an update on the reinsurance and funding for 2024 was provided.

Recall that we reported last week that for 2024, TWIA’s funding tower will see catastrophe bonds as the largest component, providing 32% of the funding limit needed to meet the statutory 1-in-100 year probable maximum loss for the coming hurricane season.

TWIA had already sponsored its largest cat bond yet, with the $1.4 billion Alamo Re Ltd. (Series 2024-1) catastrophe bond issued in recent weeks.

In addition, as we reported in our article last week, TWIA had already placed $750 million of the traditional reinsurance limit it requires for 2024 before the end of April.

In total, TWIA needs just over $4 billion of reinsurance and cat bonds in-force for 2024, to meet its statutory funding limit.

The residual market insurer will have $2.1 billion in cat bonds, having $700 million from previous years that are still in-force.

Then, with that $750 million of traditional reinsurance secured, it left around $1.2 billion left to secure.

Progress seems to have been quickly made, as Gallagher Re executives said that support is already secured for that and it’s expected to be finalised imminently.

Alan Cashin, of Gallagher Re told the TWIA Board, “At this point, it’s a June 1st renewal. A large majority of it has been placed, I think we were left with about $1.2 billion in limit that needed to be placed and as of now we have enough support to execute and sign the programme over the next couple of days.”

Cashin added that, “I will work with staff Wednesday and Thursday of this week to finalise the entire programme… We are just over $1.2bn and then we’ll work with staff to sign lines over the next couple of days.”

Bill Dubinsky, of Gallagher Securities, provided some colour on the largest cat bond issuance TWIA has ever sponsored.

Dubinsky explained that, “To get to the $4 billion figure we increased the total amount of cat bonds by $900 million, so there were $1.4 billion placed this year.”

Dubsinsky went on to discuss the overall reinsurance tower that TWIA will have in-force for the 2024 Atlantic hurricane season.

He explained that, “The whole structure that you see here is designed to both access reinsurance capacity and cat bond capacity on a differentiated basis, to get to reinsurers as well as investors who have different risk-return appetites.

“That really was something that hadn’t been done as much in the past on the cat bond side, but was really key in getting to that $1.4 billion structure.”

TWIA has been directly sponsoring catastrophe bonds since 2014 and now sits as one of the largest sponsors in our cat bond market sponsors leaderboard.

Texas Windstorm (TWIA) ready to sign reinsurance renewal lines this week was published by: www.Artemis.bm

Our catastrophe bond deal directory

Sign up for our free weekly email newsletter here.