Rate increases slower for catastrophe exposed US property in Q1: Marsh

This content is copyright to www.artemis.bm and should not appear anywhere else, or an infringement has occurred. In what is perhaps a reflection of an insurance and reinsurance marketplace with more catastrophe risk capital available, broker Marsh has for the first time in a while […]

Industry Loss WarrantyILS market yield potential remains attractive, cat bonds still top-pick: K2 Advisors

This content is copyright to www.artemis.bm and should not appear anywhere else, or an infringement has occurred. K2 Advisors, the hedge fund focused investment management unit of Franklin Templeton, believes that the forward-looking total yield potential of insurance-linked securities (ILS) remains attractive despite recent spread […]

Industry Loss WarrantyUS cat sees “material softening” in minimum rates-on-line: Gallagher Re

This content is copyright to www.artemis.bm and should not appear anywhere else, or an infringement has occurred. Catastrophe reinsurance pricing for programs in the United States is seeing “material softening” in minimum rates-on-line, broker Gallagher Re has said, as reinsurers “abandon” the need for top-layer […]

Industry Loss Warranty

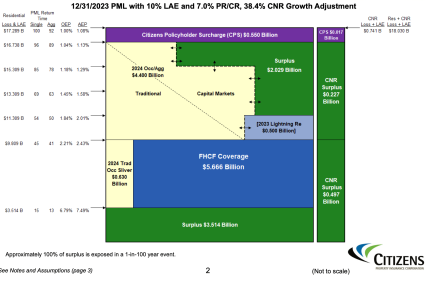

Florida Citizens: Capital markets “especially” positive for $5.5bn reinsurance renewal

This content is copyright to www.artemis.bm and should not appear anywhere else, or an infringement has occurred. Florida’s property insurer of last resort, Citizens Property Insurance Corporation, has said that its sees market conditions as especially positive in the capital markets, as it looks to […]

Industry Loss WarrantyThis content is copyright to www.artemis.bm and should not appear anywhere else, or an infringement has occurred.

Florida’s property insurer of last resort, Citizens Property Insurance Corporation, has said that its sees market conditions as especially positive in the capital markets, as it looks to progress its $5.5 billion reinsurance renewal for 2024.

Citizens is expected to buy its largest tower ever, with a total of $5.5 billion of reinsurance limit needed this year.

The insurer has merged its three previous accounts, the Personal Lines Account (PLA), the Commercial Lines Account (CLA), and the Coastal Account, into a single Citizens Account and this is the first time Citizens is coming to the reinsurance market with this consolidated approach to its risk tower and risk transfer needs.

The total $5.5 billion reinsurance purchase will come in two main layers.

First, a sliver layer that sits alongside the FHCF coverage, which will provide approximately $630 million of per-occurrence one-year cover, in excess of at attachment point of $3.5 billion, to cover personal residential and commercial residential losses.

This sliver layer will be placed in the traditional reinsurance market and is designed to work alongside the mandatory coverage provided by the FHCF.

Above that will sit the bulk of Florida Citizens private market risk transfer and reinsurance (roughly $4.9 billion worth), with layer 1 attaching at $9.8 billion and extending to $16.7 billion, with reinsurance, catastrophe bonds and surplus all set to work together in this layer.

The residual market insurer is planning to keep its industry-loss triggered Lightning Re Ltd. (Series 2023-1) catastrophe bond for the coming year, clearly finding it a cost-effective form of reinsurance to continue paying the risk premiums for.

It’s important to note that this is not a new Lightning Re issuance, it’s just the multi-year cat bond rolling forwards and being maintained for another year for Citizens.

In addition to that, Citizens will need roughly $4.4 billion of new reinsurance and risk transfer for this layer.

Florida Citizens intends to procure this from both the traditional and capital markets, so more catastrophe bonds are anticipated.

Both aggregate and occurrence coverage will fill this layer as well, although it’s not clear whether any occurrence cat bonds would be issued, as Citizens has not sponsored a purely occurrence cat bond since 2013, with aggregate named storm cover the most likely structure, we believe.

This layer 1 of around $4.9 billion will provide reinsurance for Florida Citizens personal residential and commercial residential losses.

Now that the structure of the tower is better understood, it’s anticipated Citizens will get indications from markets to help it decide how best to structure the reinsurance within this layer and how much of it could be sourced in catastrophe bond and also collateralized reinsurance form.

Historically, Florida Citizens has always sponsored cat bonds and had a significant component of its traditional reinsurance provided by ILS funds, often in collateralized formats.

We see no reason to expect different in 2024. In fact, it’s anticipated that Florida Citizens could bring a particularly large catastrophe bond to market this year, while we’re also hearing that large lines are anticipated by some of the major ILS market players again.

Citizens staff noted that, “Thus far in 2024, global reinsurance markets, especially capital markets, have a positive outlook with an increase in capacity and demand with rates that projected to remain flat to – 5% depending on the cedent.”

No doubt Florida Citizens will have been watching the cat bond market closely and will be pleased with recent price developments for catastrophe bonds with Florida hurricane exposure.

A year ago, Florida Citizens secured just over $5.38 billion of reinsurance protection, from traditional and ILS markets, for 2023.

This consisted of $2.4 billion of outstanding catastrophe bonds, at the time of the renewal, and a fresh placement of $2.98 billion of traditional and collateralized reinsurance at the June 1st renewal in 2023.

Buying $5 billion of completely new reinsurance for 2024 is a significant increase, remember the Lightning Re bond is still in-force and will roll forwards to provide the other $500 million.

Florida Citizens: Capital markets “especially” positive for $5.5bn reinsurance renewal was published by: www.Artemis.bm

Our catastrophe bond deal directory

Sign up for our free weekly email newsletter here.

PGGM / PFZW lift ILS allocation ranges for Swiss Re sidecar, Nightingale Re

This content is copyright to www.artemis.bm and should not appear anywhere else, or an infringement has occurred. Target allocation ranges have been adjusted for some of the investments that make up the giant insurance-linked securities (ILS) portfolio managed by PGGM, the Dutch pension fund investment […]

Industry Loss WarrantyThis content is copyright to www.artemis.bm and should not appear anywhere else, or an infringement has occurred.

Target allocation ranges have been adjusted for some of the investments that make up the giant insurance-linked securities (ILS) portfolio managed by PGGM, the Dutch pension fund investment manager, on behalf of its end-client the Dutch pension PFZW.

In particular, the target allocation ranges for the Swiss Re private sidecar structure Viaduct Re and private mandate vehicle Nightingale Re have both seen increases in recent months.

In particular, the target allocation ranges for the Swiss Re private sidecar structure Viaduct Re and private mandate vehicle Nightingale Re have both seen increases in recent months.

As we reported back in March, the PGGM managed insurance-linked securities (ILS) portfolio had grown to more than US $9 billion in ILS assets under management by the end of 2023.

At that time, we also knew was that the investor had been making increased use of the Nightingale Re Ltd. private mandate vehicle, through which PGGM aims to partner directly with cedents needing reinsurance capital, entering into private transactions that can be significant in size.

By the end of 2023 PGGM’s insurance-linked investments team had made 11 investments using the Nightingale Re structure.

But, now Artemis has learned from the latest disclosure made by PGGM’s client the Dutch pension fund for the care and healthcare sector PFZW, that the target allocation range has been increased for the Nightingale Re strategy from the EUR 50-250 million, that was set as recently as the middle of 2023, to now between EUR 250-500 million as of January 31st 2024.

Which implies the Nightingale Re strategy could double, or more, for PGGM and PFZW if they chose to, with scope to increase the amount of private collateralised reinsurance activity entered into using the Bermuda vehicle.

Another notable change, in the targeted allocation ranges, is for the Viaduct Re Ltd. private reinsurance sidecar arrangement between PGGM and Swiss Re.

We reported back in 2020 that PGGM had made a second investment into Viaduct Re, which meant private reinsurance sidecar arrangements between the investor and Swiss Re had reached over US $500 million in terms of size.

But now, the latest disclosure from pension PFZW, shows that the target allocation range for PGGM’s Viaduct Re arrangement has risen from the EUR 250-500m it had been set at back at the mid-point of 2023, to now between EUR 500 million to 1 billion as of January 31st.

Which again suggests scope to double the allocation, should it prove appealing and the market opportunity conducive to do so.

With these allocation target ranges, which PGGM / PFZW have set for each of the ILS managers and reinsurance partners they invest with, of course we don’t have specific visibility of just how large each allocation is.

But, when the target allocation range doubles, it suggests there has at least been growth in how much capital is being invested through that arrangement or ILS partnership, at least tipping it into the new bracket, as it becomes too large for the old.

For most of the rest of the PFZW ILS investments managed by PGGM, the target ranges remain static since 2023, to such industry names as Aeolus Capital Management, Fermat Capital Management, Nephila Capital, LGT ILS Partners, Elementum Advisors, Munich Re, AXA XL, rated reinsurer Vermeer Re, Partner Re and SCOR.

But, for the first time we have visibility of the allocation to a fund managed by Integral ILS, which is named the Riemann Fund and has an allocation target range of EUR 50-250 million set.

There is also one that has declined, which is a strategy that had been managed by AlphaCat, the Soteria Fund, which at June 2023 had been cited as having a target range of EUR 250-500 million, but now presumably being in run-off since the acquisition of Validus by RenRe, that target has dropped to EUR 50-250 million.

However, the overall ILS allocation scope remains within a range of EUR 5 billion to EUR 10 billion for PFZW, capping the potential across all of the different ILS strategies and reinsurer partnerships.

PGGM remains the largest single investor listed in our directory of pension funds and sovereign wealth funds investing in ILS and reinsurance and is the biggest allocator in the ILS sector.

PGGM / PFZW lift ILS allocation ranges for Swiss Re sidecar, Nightingale Re was published by: www.Artemis.bm

Our catastrophe bond deal directory

Sign up for our free weekly email newsletter here.

Signs of growth in collateralised reinsurance market: Vickers, Gallagher Re

This content is copyright to www.artemis.bm and should not appear anywhere else, or an infringement has occurred. The level of insurance-linked securities (ILS) capital reached new heights in 2023 on the back of record issuance in the catastrophe bond market, and while collateralised reinsurance has […]

Industry Loss WarrantyThis content is copyright to www.artemis.bm and should not appear anywhere else, or an infringement has occurred.

The level of insurance-linked securities (ILS) capital reached new heights in 2023 on the back of record issuance in the catastrophe bond market, and while collateralised reinsurance has so far failed to rebound, there are signs of growth, according to James Vickers, Chairman of International, Gallagher Re.

Artemis spoke with Vickers around the launch of the reinsurance broker’s April 1 renewals report, which reveals that further price softening is anticipated as demand continues to rise alongside greater availability of capital.

Artemis spoke with Vickers around the launch of the reinsurance broker’s April 1 renewals report, which reveals that further price softening is anticipated as demand continues to rise alongside greater availability of capital.

After reaching record heights in 2023 and with cat bond market momentum persisting so far in 2024, Vickers feels that ILS capital’s influence could be quite significant at the mid-year reinsurance renewals.

“ILS capital is always playing a supporting role to the traditional market. But it is buoyant, and the spreads are coming down,” said Vickers.

“The best ILS fund managers are growing their funds under management; they produced some wonderful returns for 2023. And some of them we know have got offers of more capital that they feel comfortable to deploy. So, yes, ILS capital can be very helpful,” he added.

On the traditional cat bond side of the ILS marketplace, Vickers reiterated that ILS managers who’ve performed well almost have an embarrassment of riches at the moment.

“It’s more a question of can they continue to deploy their capacity at attractive terms,” he said.

But while cat bond market growth has been impressive in recent times, the collateralised reinsurance market, which is the largest part of the ILS universe, has stagnated.

“Collateralisation is an interesting topic,” said Vickers. “There are signs that there is a bit of growth there. Capacity is coming into that market, and for a lot of investors that’s a better way to enter the market. Partner up, do a collateralised sidecar with an existing, well-known reinsurer rather than investing in a bricks and mortar reinsurer from scratch.”

Vickers went on to note that it’s quite noticeable that a number of the new reinsurance startups that have been discussed have failed to materialise, stating that at this time, they don’t seem to be able to attract investors.

“And one of the reasons, I think, is that those who wish to invest in reinsurance, is you’ve got so many other options, such as collateralised sidecars, so if you can find the right partner, is quite an attractive option.

“So, collateralised, it may grow a bit, particularly as investors grow in confidence,” said Vickers.

Commenting on capital more broadly and whether it can rebuild this year and how influential that could be at the mid-year renewals and into 2025, Vickers said that if 2024 is another good underwriting year and the investment performance is decent, capital will continue to build.

“If you think what one good underwriting year can do, allied with reducing interest rates that are boosting up the asset side of the balance sheets as well, it can be quite significant.

“Having said that, as a reinsurer sitting sit there at the mid-year, you’ve still got the US hurricane season ahead of you, you’re probably not counting your chickens until you get to the end of the year and know what state your capital is going to be in. Touch wood, so far, it’s been a pretty good Q1. But just because nothing untoward happens between now and 1/6 doesn’t necessarily mean that reinsurers will be overly aggressive in terms of using their capital because they know that they’ve still got to get through the more traditionally difficult second-half year,” said Vickers.

Interestingly, Vickers told Artemis that while there appears to be a feeling around the investor community that the reinsurance market was hardening from around 2019 onwards, the reality is that 2020, 2021, and 2022 were all pretty poor years.

“And there are more hard bitten investors who think okay, fine, 2023 is a good year but one swallow doesn’t make a summer. Reinsurers need to produce another year and show that they can do it consistently,” said Vickers.

“Let’s wait and see whether reinsurers can manage a second decent year. Then I think the dynamics might change a bit. But again, smart investors will also be looking at demand as they will be worried if the capital grows too fast that’ll only push pricing down and the returns will fall away.

“Now, if they can be convinced that demand is going to grow and that capital can be put to good use at a reasonable margin, that’s another subject,” he concluded.

Read all of our interviews with ILS market and reinsurance sector professionals here.

Signs of growth in collateralised reinsurance market: Vickers, Gallagher Re was published by: www.Artemis.bm

Our catastrophe bond deal directory

Sign up for our free weekly email newsletter here.

Tokio Marine is first Japanese cat bond sponsor to use sustainable development bond

This content is copyright to www.artemis.bm and should not appear anywhere else, or an infringement has occurred. Tokio Marine Holdings, Inc., through its subsidiary Tokio Marine & Nichido Fire Insurance Co. Ltd., has become the first Japanese insurer to make use of a SOFR-based World […]

Industry Loss WarrantyThis content is copyright to www.artemis.bm and should not appear anywhere else, or an infringement has occurred.

Tokio Marine Holdings, Inc., through its subsidiary Tokio Marine & Nichido Fire Insurance Co. Ltd., has become the first Japanese insurer to make use of a SOFR-based World Bank Sustainable Development Bond as a permitted investment within its latest catastrophe bond issuance, the company highlighted today.

As Artemis has been reporting, Tokio Marine has been in the market since February and has now secured its targeted $100 million Kizuna Re III Pte. Ltd. (Series 2024-1) catastrophe bond recently, with the reinsurance coverage from the transaction priced at the low-end of initial guidance.

Now, the Japanese insurer has highlighted its use of the proceeds of the catastrophe bond issuance to purchase a sustainable development bond, saying that using this “as collateral for the Kizuna Re III cat bond is supporting the achievement of sustainable development goals and contributing to the realization of a sustainable society.”

Use of proceeds of cat bond issues to invest into financing for sustainable development helps sponsors align their catastrophe bond issues with their own environmental, social and governance (ESG) agendas, while also making the investment more appealing to investors with an ESG focus or mandate.

Tokio Marine used the proceeds of the Kizuna Re III 2024-1 catastrophe bond, that provides it with earthquake reinsurance and was issued out of Singapore, to purchase a SOFR-based Sustainable Development Bond issued by the World Bank Group’s International Bank for Reconstruction and Development (IBRD).

The company said that, through its sustainability strategy, it aims to “solve social issues through business activities and contribute to the realizations of a sustainable society” as a medium- to long-term growth engine and is accelerating its efforts to take climate action, improve disaster resilience, and protect the natural environment.”

The company said that, as part of its goal to improve disaster resilience in what is one of the most disaster-prone countries in the world, Tokio Marine has been a regular user of catastrophe bonds, alongside purchasing traditional reinsurance capacity.

“As a part of these strategies, besides sponsoring the issuance of the Kizuna Re III cat bond, TMNF has elected to invest the proceeds from the sale of the Kizuna Re III cat bond in a SDB issued by IBRD (rather than money-market funds), which is the first example of a Japanese insurer doing so since IBRD notes transitioned from LIBOR to SOFR,” the company explained.

Adding that, “The principal amount of this catastrophe bond raised from qualified institutional investors will be invested in a SDB issued by IBRD under its Global Debt Issuance Facility. The net proceeds of the SDB will be used by IBRD to fund projects, programs, and activities in IBRD’s member countries designed to achieve positive social and environmental impacts and outcomes.”

It’s encouraging to see the use of sustainable development bonds as collateral investments in the catastrophe bond market expanding further beyond just the World Bank, to private insurance sector cat bond sponsors.

The World Bank itself was the first to do so this, since when insurance giant Assicurazioni Generali S.p.A. developed its framework for Green insurance-linked securities (ILS) which saw the proceeds of one of its catastrophe bonds used to refinance a green asset in an effort to help avoid greenhouse gas emissions.

But, Tokio Marine is the first private insurance or reinsurance market sponsor of a catastrophe bond to use a puttable SOFR linked Sustainable Development Bond from the IBRD, which marks an efficient way to structure a cat bond with collateral that can be put to work in supporting sustainable or ESG driven goals.

As a reminder, Gallagher Securities, the insurance-linked securities (ILS) specialist arm of reinsurance broker Gallagher Re was the sole structuring agent for this new cat bond for Tokio Marine, so will have been instrumental in incorporating the sustainable development bond as permitted investments for the collateral, within the overall cat bond structure for this issuance.

You can read all about this new Kizuna Re III Pte. Ltd. (Series 2024-1) catastrophe bond transaction and every other Tokio Marine sponsored cat bond in our Artemis Deal Directory.

Tokio Marine is first Japanese cat bond sponsor to use sustainable development bond was published by: www.Artemis.bm

Our catastrophe bond deal directory

Sign up for our free weekly email newsletter here.

ILW market activity rising, as preparations for hurricane season begin

This content is copyright to www.artemis.bm and should not appear anywhere else, or an infringement has occurred. According to Artemis’ sources, activity in the industry-loss warranty (ILW) market has increased in the last few weeks, as reinsurance and insurance-linked securities (ILS) markets prepare for what […]

Industry Loss WarrantyThis content is copyright to www.artemis.bm and should not appear anywhere else, or an infringement has occurred.

According to Artemis’ sources, activity in the industry-loss warranty (ILW) market has increased in the last few weeks, as reinsurance and insurance-linked securities (ILS) markets prepare for what is anticipated to be an active 2024 Atlantic hurricane season.

![]() As we’ve reported, long-range seasonal forecasts for Atlantic hurricanes have suggested a challenging storm season could be ahead.

As we’ve reported, long-range seasonal forecasts for Atlantic hurricanes have suggested a challenging storm season could be ahead.

As we said, one forecaster called for a “hurricane season from hell” in 2024, while another is seen as particularly aggressive in calling for a large number of storms.

As we also reported from the SIFMA ILS event last week, forecaster Phil Klotzbach, Ph.D., from the Department of Atmospheric Science of the Colorado State University, said that the odds of La Niña are “pretty elevated” while conditions suggest we might not necessarily see as much re-curvature of storms as we did last year.

Forecasts are now concentrating minds on what could be ahead this hurricane season, with the Atlantic also at record warmth in the main development region, where storms form and fuel themselves.

With all that going on, it makes sense those holding portfolios of US coastal hurricane exposure would be preparing themselves and their portfolios for what could be a busy year of watching the tropics.

At the SIFMA ILS event in Miami last week, the subject of industry-loss warranties (ILW) and hedging preparations for hurricane season came up with a number of our contacts at ILS managers and investors in the sector.

All said that activity in ILW’s had picked up in just the last few weeks, while we also met some active buyers for the instruments.

It seems with a busy hurricane season forecast, the main route to hedging the portfolios of ILS investments continues to be the ILW, with some discussing the county-weighted industry-loss triggered instruments as well.

There was also discussion of industry-index products being constructed to more accurately reflect peak exposures in catastrophe bond portfolios, as tools for hedging against US wind exposure.

One source told us that ILW pricing has remained under-pressure through recent weeks, recall that Artemis’ data on industry loss warranty (ILW) price trends was already signalling this would occur during the last quarter of 2023.

Managers of portfolios of ILS instruments, reinsurance and retrocession with significant coastal wind exposure in the United States are keenly focused on ensuring their peaks are managed and concentration risk is controlled, we are told.

All of which makes perfect sense, in a year where such high hurricane numbers are being forecast currently.

We are also told that interest in ILW’s for hedging is being shown in some quarters of the London market as well, where retrocession needs have remained less sufficient than in previous years.

While the retro market was far more balanced at the January renewals, not everyone managed to secure the hedging capacity they needed and some were waiting to see how Atlantic conditions developed.

For those with capacity to deploy in support of industry-loss based reinsurance and retro, now might also be a good time to deploy it, as the forecasts may also assist in holding rates up a little more and some are suggesting that the softening in ILW triggered instruments that we’ve seen in catastrophe bonds of late may be slowing or even halting at this time.

We are told that capacity remains in ample supply for ILW’s and industry-loss index triggered instruments, albeit becoming more selective than it was around the January renewals.

Of course, there’s still a long way to go until the hurricane season peak and with more season hurricane forecasts due out over the next few weeks, it will be interesting to see if the activity levels in trading instruments such as ILW’s can further increase.

ILW market activity rising, as preparations for hurricane season begin was published by: www.Artemis.bm

Our catastrophe bond deal directory

Sign up for our free weekly email newsletter here.

Munich Re behind Hawaii coral reef parametric insurance renewal, coverage expands

This content is copyright to www.artemis.bm and should not appear anywhere else, or an infringement has occurred. An innovative parametric insurance product that provides protection to fund repairs following storm damage to coral reefs in Hawaii has been renewed and its coverage expanded, while global […]

Industry Loss WarrantyThis content is copyright to www.artemis.bm and should not appear anywhere else, or an infringement has occurred.

An innovative parametric insurance product that provides protection to fund repairs following storm damage to coral reefs in Hawaii has been renewed and its coverage expanded, while global reinsurance firm Munich Re is again backing the cover, which is arranged by WTW.

Back in November 2022, WTW alongside The Nature Conservancy launched the parametric coral reef insurance concept in the United States for the first time with a policy focused on Hawaii. Munich Re underwrote the risk for that first Hawaiian coral reef parametric insurance arrangement.

The same parametric risk transfer product concept had already been utilised in Mexico and was then expanded to also cover the Mesoamerican Reef system.

As we reported earlier this month, broker WTW has now taken the coral reef insurance concept across the globe to cover a South pacific coral reef in the Fiji archipelago as well.

Now, the Hawaii instance of the product has been renewed, with expanded coverage and higher payouts available, so that it can make more impact on the reef and the communities that rely on it.

The new parametric coral reef insurance policy expands coverage around the main Hawaiian islands and increases payouts after qualifying storms, WTW explained.

The new Hawaiian policy adds 314,976 square miles to the coverage area so that it can capture more storm events, with a maximum payout of $2 million total over the year-long policy period and $1 million possible per storm.

At the same time, the minimum payout after the parametric trigger is activated has doubled to $200,000, enabling a more meaningful post-storm response.

Payouts can be triggered when tropical storm winds of 50 knots or greater occur in the core of the coverage area.

Once again, a Munich Re insurance entity was selected as the coverage provider from seven competitive bids.

WTW said that more companies bid on this year’s policy, which it noted shows “increasing interest among insurers in nature-based solutions to protect against climate impacts.”

“Parametric insurance is increasingly demonstrating value in addressing disaster risk for natural assets, in this case providing Hawai’i with a tangible solution to quickly finance post- storm restoration activities that help reefs better recover and maintain resilience in the face of increasing climate impacts,” explained Simon Young, Senior Director in WTW’s Disaster Risk Finance and Parametrics team. “Increasing recognition of this value by conservation organisations, government bodies and other stakeholders on the demand side and by insurers on the supply side is mainstreaming parametric protections, driving accessibility and sustainability.”

“We are building something really transformative for communities and ecosystems as we respond to increasing storm activity associated with the climate crisis,” added Ulalia Woodside Lee, Executive Director, The Nature Conservancy, Hawai‘i and Palmyra. “The first policy provided momentum to develop response plans and partnerships. With these now in place and an increased minimum payout, we will be able to start damage assessments and reef repairs after a storm as soon as it’s safe to get in the water. This is important because corals must be reattached within several weeks after breaking or they will likely die.”

René Mück, Munich Re’s Global Head of Natural Catastrophe Parametrics, also said ”Using parametric risk transfer as a means to contribute to TNC’s conservation objectives in Hawaii aligns exactly with the objectives of Munich Re’s parametric business unit. We are proud to support TNC in Hawaii and appreciate the work with WTW on such initiatives.”

The parametric coral reef insurance product has already demonstrated its utility, when Hurricane Lisa’s landfall in Belize on November 2nd 2022 triggered the Mesoamerican Reef system parametric insurance product.

Munich Re behind Hawaii coral reef parametric insurance renewal, coverage expands was published by: www.Artemis.bm

Our catastrophe bond deal directory

Sign up for our free weekly email newsletter here.

Parametric insurance to cover South Pacific coral reef in Fiji archipelago

This content is copyright to www.artemis.bm and should not appear anywhere else, or an infringement has occurred. An innovative parametric insurance program has been taken across the globe to cover a South pacific coral reef in the Fiji archipelago, with broker WTW saying it will […]

Industry Loss WarrantyThis content is copyright to www.artemis.bm and should not appear anywhere else, or an infringement has occurred.

An innovative parametric insurance program has been taken across the globe to cover a South pacific coral reef in the Fiji archipelago, with broker WTW saying it will provide up to US $450,000 of cover for reef restoration and community assistance if cyclones hit.

The payout would go to Fiji’s island communities, if a cyclone hits the coral reef system of the South Pacific Ocean’s volcano-formed Lau Group of islands.

The payout would go to Fiji’s island communities, if a cyclone hits the coral reef system of the South Pacific Ocean’s volcano-formed Lau Group of islands.

The Indigenous people of Lau depend on the reef ecosystem as a source of food and income, so protecting it using a parametric risk transfer insurance product that will pay out after a cyclone strikes which could damage the reef, can enable the community to recover faster and put funds into reef conservation, restoration and resilience.

Development insurer and risk pool the Pacific Catastrophe Risk Insurance Company (PCRIC) is the insurer for this South Pacific parametric reef insurance, winning the bid after what WTW called “a competitive placement process.”

WTW worked with local correspondent broker Insurance Holdings (Pacific) Pte Ltd. and Fiji’s Vatuvara Foundation (VVF), which is the policyholder of the parametric insurance programme.

As well as helping to protect and repair the reef in the event of a cyclone, the parametric insurance payouts can be used to support the community with assistance activities to help address food and water security concerns caused by storm damage.

The initial coverage is for Vatuvara Island, a protected natural reserve; Yacata, where the local community resides; and Kaibu, the Vatuvara Private Islands Resort, while further sites in the Lau Seascape may be covered in future years.

Sarah Conway, Director and Ecosystem Resilience Lead, WTW, commented “We are grateful to BHP for supporting the design and implementation of the first coral reef insurance programme in Fiji. Building on lessons learned from our involvement with similar initiatives in other countries, this programme provides an exciting opportunity to innovate beyond rapid reef response to also include community assistance, enhancing the resilience of the ecosystem and those who depend on it.”

PCRIC CEO, Aholotu Palu, stated, “PCRIC is very pleased to demonstrate its commitment to serve non-sovereign entities with innovative parametric insurance products, in line with PCRIC’s mission to help the island communities of the Pacific to better prepare, structure and manage finances to foster disaster resilience and ensure rapid access to funds; the work of the Vatuvara Foundation, both in reef conservation and in local community empowerment, is recognised by the Government of Fiji as being in the national interest and consistent with development priorities, particularly the Blue Pacific Strategy, as well as commitments to climate change adaptation and disaster risk management.”

Katy Miller, Director, Vatuvara Foundation, added, “We are thankful that the innovative parametric policy will allow for the prompt access to funds following a destructive cyclone event to identify reef damage and assist reef recovery with a community-led team in Northern Lau. Increased frequency and severity of extreme weather events is expected in the area, and protecting natural ecosystems in the Lau Group is crucial to build long-term community resilience to anthropogenic threats including climate change.”

Ashley Preston, Head of Climate Resilience, BHP, also said, “BHP is funding an innovative parametric insurance product, which aims to support the conservation of coral reefs and surrounding local communities in Fiji’s northern Lau Group, and build the knowledge base for how similar financial products could be used to improve climate resilience. We are pleased to work with WTW and Vatuvara Foundation on this project, which supports BHP’s commitments to action on climate, conservation and empowering communities.”

Parametric insurance to cover South Pacific coral reef in Fiji archipelago was published by: www.Artemis.bm

Our catastrophe bond deal directory

Sign up for our free weekly email newsletter here.

Jireh Connect facilitates first industry loss warranty (ILW) placement

This content is copyright to www.artemis.bm and should not appear anywhere else, or an infringement has occurred. Jireh Connect, a technology platform that targets helping brokers place risk more efficiently with reinsurance and risk capital providers and manage the process more effectively, has announced the […]

Industry Loss WarrantyThis content is copyright to www.artemis.bm and should not appear anywhere else, or an infringement has occurred.

Jireh Connect, a technology platform that targets helping brokers place risk more efficiently with reinsurance and risk capital providers and manage the process more effectively, has announced the completion of its first placement, an industry loss warranty (ILW).

Jireh Connect has been launched by well-known Bermuda-based insurance-linked securities (ILS) market executive Sal Tucci.

Last year, Tucci launched Jireh Holdings Ltd., a company offering ILS risk transformation, fronting and advisory services to clients, with a broader insurance management offering in the works.

Jireh Connect was also launched, as Tucci sought to bring a technology platform to market that is built by brokers, for brokers, but makes their workflow easier and more efficient.

The Jireh Connect platform was soft-launched with one broker in Bermuda at the start of this year, successfully managing nearly $100 million in capacity across various ILW structures in its first month of operation, the company claimed today.

“We couldn’t be more pleased with the early success of Jireh Connect both in terms of facilitating its first bound transaction but also in having six markets actively engage on the platform,” explained Tucci. “We have had very positive feedback without our having made any prior public announcement of its availability to them. We credit this positive engagement to our very different approach to technology within our unique market.”

As we reported, ReFlex Solutions Ltd, an independent reinsurance brokerage headquartered in Bermuda launched by Neville Ching was said to be partnering with Jireh.

Jireh Connect enables brokers to coordinate reinsurance placements across their teams, acting as a front-office broker workbench, which can distribute deals, share documents with markets and capture external market feedback for users.

The platform can deliver analytics on market appetite and pricing in real-time, to help inform strategies when structuring transactions.

Jireh Connect was initially launched as a Minimum Viable Product (MVP) in 2024, with a focus on becoming a reinsurance broker workbench for ILW arrangements. New product offerings and system features are expected to be rolled out based on market demand, the company said.

Tucci said, “In the past, we’ve seen the roll out of numerous platforms in the reinsurance market developed by people from outside the industry who, looking in from the outside, endeavor to compress the value chain by disintermediating what they deem to be an inefficient market. We believe this is absolutely the wrong approach. Jireh Connect has been specifically designed ‘by brokers for brokers’ to complement the current reinsurance broker market process rather compete or replace it.”

Tucci further explained, “By way of example, despite the unquestionable convenience of ordering and paying for goods via your smartphone, there will always be customers who opt to wait in longer lines to order and pay cash. Many previous technology attempts within the reinsurance market make sense in theory and look great in a venture capital pitchbook, but the well-entrenched realities of how reinsurance is bought and sold cannot simply be ignored. Given our deep market experience, we designed Jireh Connect to provide the same efficacy to brokers through the platform even when customers or markets opt to communicate via email or in person. That is a significant differentiator between Jireh Connect and others that have come before us.”

Jireh Connect facilitates first industry loss warranty (ILW) placement was published by: www.Artemis.bm

Our catastrophe bond deal directory

Sign up for our free weekly email newsletter here.

Bermuda’s BMA aims to better facilitate parametric climate-related re/insurance

This content is copyright to www.artemis.bm and should not appear anywhere else, or an infringement has occurred. The Bermuda Monetary Authority (BMA) has laid out its plans for 2024, with Chief Executive Officer (CEO) Craig Swan highlighting specific opportunities in parametric risk transfer for climate […]

Industry Loss WarrantyThis content is copyright to www.artemis.bm and should not appear anywhere else, or an infringement has occurred.

The Bermuda Monetary Authority (BMA) has laid out its plans for 2024, with Chief Executive Officer (CEO) Craig Swan highlighting specific opportunities in parametric risk transfer for climate insurance.

The 2024 business plan of Bermuda’s financial regulator contains a focus on “initiatives and projects to achieve positive outcomes and strengthen Bermuda’s regulatory framework for the upcoming year.”

The 2024 business plan of Bermuda’s financial regulator contains a focus on “initiatives and projects to achieve positive outcomes and strengthen Bermuda’s regulatory framework for the upcoming year.”

Of relevance to the insurance, reinsurance and insurance-linked securities (ILS) community, the Bermuda Monetary Authority (BMA) expects to continue to work on enhancing its regulatory and supervisory regimes to meet the evolving needs of financial service companies today.

There will be further work on the Insurance Code of Conduct, “to uphold the importance of financial transparency, consumer protection and education initiatives,” the BMA explains.

While an Environmental, Social and Governance (ESG) model and a Sustainability Strategy are also key initiatives and here there are relevant items to look out for, for this industry.

BMA CEO Craig Swan said, “The Authority’s strategy is underpinned by deep expertise and cross-functional viewpoints designed to champion innovation. This plan’s many thoughtfully curated objectives will optimise excellence while simultaneously preparing the organisation to meet and address emerging challenges that impact the regulatory environment. In a continually fluctuating business climate, this approach enables the BMA to open new pathways for enhancing our abilities and innovative practices today and for many years to come.”

Swan also commented, “The pace of innovation is challenging organisations to remain agile and adapt how they work to meet the ebb and flow of their markets. From artificial intelligence and automation to decentralised finance and insurance-linked securities, the financial services industry has evolved markedly over the last few decades with increasingly transformative leaps forward each successive year.

“As firms confront issues such as inflationary pressures, relentless consumer demands, volatility in the commodity markets and extreme climate patterns, they are building systems to redefine and reimagine their future aspirations.”

The BMA intends to explore working with investment funds to “set up a new framework that facilitates the ability to designate certain Bermuda funds as ESG compliant,” Swan said.

This could be an interesting initiative for ILS managers, given there are plenty of ILS fund structures domiciled in Bermuda that could find an ESG framework appealing to look into.

The BMA also intends to prepare a consultation paper on a new climate risk disclosure framework for Bermuda commercial (re)insurers, Swan also explained.

But, perhaps most compelling in the current environment and in terms of opportunity, the BMA also intends to work in 2024 on “reviewing and, where applicable, updating other (re)insurance frameworks to better facilitate parametric climate-related insurance products.”

Bermuda has always considered itself as the world’s climate risk capital market and given the proliferation of catastrophe, weather and climate focused underwriting expertise in the islands insurers, reinsurers and of course ILS fund managers, there is clearly a wealth of experience and relevant knowledge, as well as ongoing business there.

If Bermuda can make its regulatory and supervisory regime even more relevant to underwriters of parametric climate risk insurance and reinsurance opportunities, while also finding ways to tap into the ILS market expertise on the island, the opportunity to attract and deploy climate risk capital out of the market there seems a worthwhile achievable goal.

The BMA has always followed a forward-thinking agenda and this year’s business plan again highlights the regulators’ ability to focus on emerging trends that can be drivers of future profit for Bermuda’s financial market and its participants.

Bermuda’s BMA aims to better facilitate parametric climate-related re/insurance was published by: www.Artemis.bm

Our catastrophe bond deal directory

Sign up for our free weekly email newsletter here.

2024 still an attractive entry point for insurance-linked securities investors: K2 Advisors

This content is copyright to www.artemis.bm and should not appear anywhere else, or an infringement has occurred. Despite some tightening of spreads in catastrophe bonds, overall K2 Advisors, the hedge fund focused investment management unit of Franklin Templeton, remains overweight the insurance-linked securities (ILS) asset […]

Industry Loss WarrantyThis content is copyright to www.artemis.bm and should not appear anywhere else, or an infringement has occurred.

Despite some tightening of spreads in catastrophe bonds, overall K2 Advisors, the hedge fund focused investment management unit of Franklin Templeton, remains overweight the insurance-linked securities (ILS) asset class, although finds industry-loss warranties (ILW’s) relatively less attractive at this time.

![]() Positively, K2 Advisors notes that while private ILS investments, such as collateralized reinsurance and retrocession, have faced challenges, some capital is expected to flow to the managers with the best track-records.

Positively, K2 Advisors notes that while private ILS investments, such as collateralized reinsurance and retrocession, have faced challenges, some capital is expected to flow to the managers with the best track-records.

But, even with this, K2 Advisors says the private ILS segment may still be capital constrained, overall, suggesting rates have a greater chance to remain elevated.

Giving its outlook for the first-quarter of 2024, the K2 Advisors hedge fund team state, “Following a record year of new issuance, the catastrophe bond market spread is elevated relative to historical levels, despite tightening throughout the year. We believe it remains an attractive entry point.”

They expect January reinsurance renewal pricing to have shown continued increases, year-on-year, while in the cat bond space they say, “We expect an active and attractively priced new issuance pipeline throughout the first half of 2024.”

Adding that, “We continue to overweight insurance-linked securities due to the diversification they can provide, along with a yield pick- up and idiosyncratic risk/return profile.”

Going into more detail, K2 Advisors highlights the record issuance and market size indicated by Artemis’ data on the catastrophe bond market.

The investment manager comments, “The combination of increasing investor demand for more senior insurance-linked securities (ILS) risk and higher total insured values, likely due to economic inflation, have led the catastrophe bond market to reach its largest size on record. While catastrophe bond pricing tightened throughout 2023, we are seeing signs of price stabilization.

“When coupled with a meaningful collateral return, we believe this provides an attractive entry point for investors into the catastrophe bond market.”

On the private ILS side, the improvements in price achieved at the January reinsurance renewals will play into, “increasing the risk adjusted price improvements the markets experienced during the January 2023 renewals,” K2 Advisors suggest.

Going into more detail to explain, “Given the strong performance across ILS risk segments throughout 2023, we expect some level of new capital to enter the market. On the private ILS side, we expect capital to gravitate toward managers who have demonstrated suitable loss-reserving policies. There will likely continue to be a supply/demand imbalance across private ILS strategies, with cedants retaining more risk on their balance sheets. Subsequently, this implies more volatility and lower-down loss exposure as many frequency losses may not be able to be hedged.”

Overall, K2 Advisors remains overweight the insurance-linked securities (ILS) asset class as a whole.

While this has been revised down from strongly overweight at Q4 2023, it’s important to note that the only segment of ILS that has actually been revised down is industry-loss warranties (ILW’s), which was taken down from strongly overweight, to overweight.

K2 Advisors outlook remains strongly overweight for catastrophe bonds, private ILS transactions and retrocession, while its position on life ILS remains underweight.

2024 still an attractive entry point for insurance-linked securities investors: K2 Advisors was published by: www.Artemis.bm

Our catastrophe bond deal directory

Sign up for our free weekly email newsletter here.