City National Rochdale mutual ILW fund delivers 15.6% return

This content is copyright to www.artemis.bm and should not appear anywhere else, or an infringement has occurred. The City National Rochdale Select Strategies Fund, a US mutual insurance-linked securities (ILS) fund focused on investments into industry-loss warranties (ILW’s) and industry-index trigger catastrophe bonds, delivered its […]

Industry Loss Warranty

Mid-year renewals to see significant increase in US property cat capacity demand: Aon

This content is copyright to www.artemis.bm and should not appear anywhere else, or an infringement has occurred. Broking giant Aon is anticipating a “significant increase in demand” for property catastrophe reinsurance capacity at the upcoming mid-year renewals, with market conditions expected to continue developing favourably […]

Industry Loss Warranty

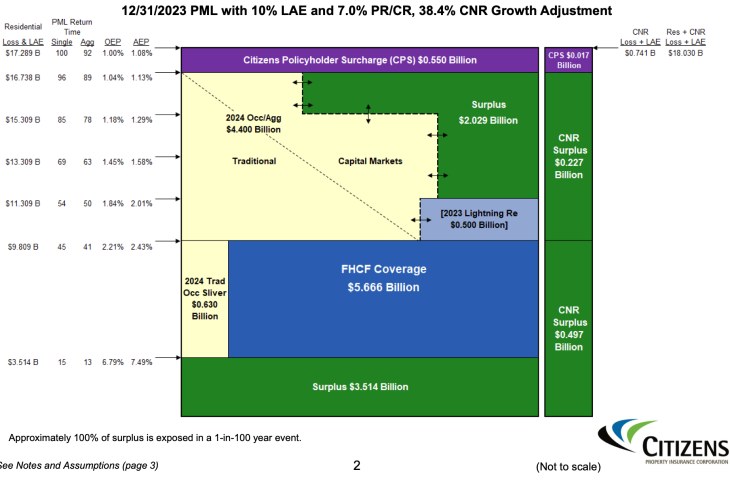

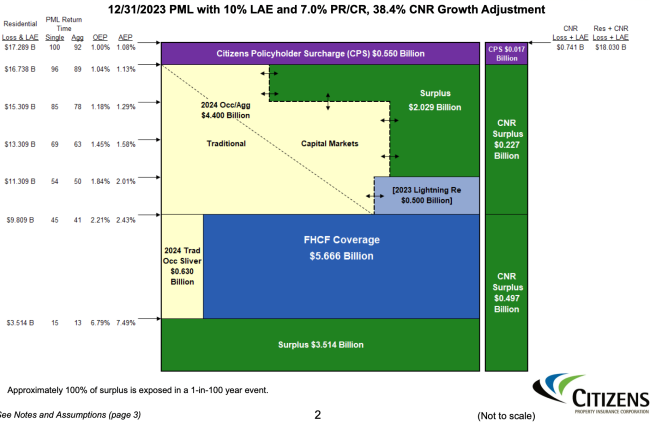

Florida Citizens: Capital markets “especially” positive for $5.5bn reinsurance renewal

This content is copyright to www.artemis.bm and should not appear anywhere else, or an infringement has occurred. Florida’s property insurer of last resort, Citizens Property Insurance Corporation, has said that its sees market conditions as especially positive in the capital markets, as it looks to […]

Industry Loss Warranty

Aon: Dramatic property cat shift at renewals. ILS capital at new $108bn high

This content is copyright to www.artemis.bm and should not appear anywhere else, or an infringement has occurred. Broking giant Aon has noted a buyers market for property catastrophe reinsurance at the April renewals, with flat to slightly down pricing and an environment where there has […]

Industry Loss WarrantyThis content is copyright to www.artemis.bm and should not appear anywhere else, or an infringement has occurred.

Broking giant Aon has noted a buyers market for property catastrophe reinsurance at the April renewals, with flat to slightly down pricing and an environment where there has been a “dramatic shift” towards ample capacity, within which ILS market growth is a key factor.

Aon said that reinsurance market conditions have continued to ease since January 1st, resulting in a much better opportunity for buyers at the April 1st renewals where some 60% of Asian treaty reinsurance business renews.

Aon said that reinsurance market conditions have continued to ease since January 1st, resulting in a much better opportunity for buyers at the April 1st renewals where some 60% of Asian treaty reinsurance business renews.

The broker noted that renewal pricing was “broadly flat” for property catastrophe reinsurance, but that certain Asia Pacific markets and product lines “remained challenged and subject to a tightening in terms and conditions”.

These included, property per-risk reinsurance; industrial fire accounts; certain natural catastrophe loss-affected regions; and U.S. exposed casualty treaties, Aon said.

In Japan, property catastrophe reinsurance renewal pricing was “flat to slightly reducing”, Aon said, while South Korea, China and India also saw greater competition for catastrophe business, but to varying degrees.

Aon also noted that, at April 1st, facultative reinsurance was a focus, as reinsurers displayed an increased appetite for this business at the renewal, while new players continued to enter the market, such as managing general agents.

New reinsurance capital deployment opportunities were also seen in India, Aon reports.

George Attard, CEO of Asia Pacific for Aon’s Reinsurance Solutions, commented, “The April 1st reinsurance renewals were more predictable and generally favorable to reinsurance buyers. As mid-year renewals get under way for the catastrophe-exposed markets of Florida, Australia and New Zealand, reinsurers are indicating a strong appetite for catastrophe risk. We would expect the positive trend of the January and April renewals to continue at mid-year renewals, with adequate capacity for property catastrophe risks and enhanced pricing competition. Insurers looking to purchase additional limit will also find adequate capacity to meet their needs.”

Interestingly, Aon also reports today that global reinsurance capital is back near its previous high, at $670 billion at the end of 2023.

Strong reinsurer results and a recovery in asset values in 2023 helped here, but so too did insurance-linked securities (ILS) market growth.

In fact, Aon Securities now estimates that ILS capital grew by 7% in 2023, to reach a new all-time high of $108 billion at the end of the year.

Catastrophe bond growth will have been one driver of that, but the expansion in the fourth quarter from the $103 billion Aon had reported for the end of September 2023 figure, must include growth on the collateralized side of the ILS market as well, given the cat bond market alone did not add $5 billion in the final quarter of the year.

That new high of $108 billion may be eclipsed once Aon reports the next quarterly rise, as capital has been building in the ILS sector and is expected to continue to do so through to the middle of the year.

Looking towards the mid-year renewals, where Florida and the US are more the focus, Aon said that Aon’s earlier renewal discussions are happening on a significant number of U.S. mid-year renewals, which is a positive trend, with reinsurers said “ready to provide indications and secure capacity.”

Aon notes that it expects the market will see around $7 billion of additional demand from U.S. insurers for property catastrophe reinsurance limit at the mid-year renewals.

This is because programs are keeping pace with inflation and evolving views of risk, as well as the contribution from “a resurgent Florida market.”

Given the rise in traditional and alternative reinsurance capital and the interest being shown by investors, that additional demand is likely to be soaked up very easily and it increasingly seems the mid-year renewals will be a far more stable, perhaps even flat, environment compared to the prior year.

Aon: Dramatic property cat shift at renewals. ILS capital at new $108bn high was published by: www.Artemis.bm

Our catastrophe bond deal directory

Sign up for our free weekly email newsletter here.

Tokio Marine is first Japanese cat bond sponsor to use sustainable development bond

This content is copyright to www.artemis.bm and should not appear anywhere else, or an infringement has occurred. Tokio Marine Holdings, Inc., through its subsidiary Tokio Marine & Nichido Fire Insurance Co. Ltd., has become the first Japanese insurer to make use of a SOFR-based World […]

Industry Loss WarrantyThis content is copyright to www.artemis.bm and should not appear anywhere else, or an infringement has occurred.

Tokio Marine Holdings, Inc., through its subsidiary Tokio Marine & Nichido Fire Insurance Co. Ltd., has become the first Japanese insurer to make use of a SOFR-based World Bank Sustainable Development Bond as a permitted investment within its latest catastrophe bond issuance, the company highlighted today.

As Artemis has been reporting, Tokio Marine has been in the market since February and has now secured its targeted $100 million Kizuna Re III Pte. Ltd. (Series 2024-1) catastrophe bond recently, with the reinsurance coverage from the transaction priced at the low-end of initial guidance.

Now, the Japanese insurer has highlighted its use of the proceeds of the catastrophe bond issuance to purchase a sustainable development bond, saying that using this “as collateral for the Kizuna Re III cat bond is supporting the achievement of sustainable development goals and contributing to the realization of a sustainable society.”

Use of proceeds of cat bond issues to invest into financing for sustainable development helps sponsors align their catastrophe bond issues with their own environmental, social and governance (ESG) agendas, while also making the investment more appealing to investors with an ESG focus or mandate.

Tokio Marine used the proceeds of the Kizuna Re III 2024-1 catastrophe bond, that provides it with earthquake reinsurance and was issued out of Singapore, to purchase a SOFR-based Sustainable Development Bond issued by the World Bank Group’s International Bank for Reconstruction and Development (IBRD).

The company said that, through its sustainability strategy, it aims to “solve social issues through business activities and contribute to the realizations of a sustainable society” as a medium- to long-term growth engine and is accelerating its efforts to take climate action, improve disaster resilience, and protect the natural environment.”

The company said that, as part of its goal to improve disaster resilience in what is one of the most disaster-prone countries in the world, Tokio Marine has been a regular user of catastrophe bonds, alongside purchasing traditional reinsurance capacity.

“As a part of these strategies, besides sponsoring the issuance of the Kizuna Re III cat bond, TMNF has elected to invest the proceeds from the sale of the Kizuna Re III cat bond in a SDB issued by IBRD (rather than money-market funds), which is the first example of a Japanese insurer doing so since IBRD notes transitioned from LIBOR to SOFR,” the company explained.

Adding that, “The principal amount of this catastrophe bond raised from qualified institutional investors will be invested in a SDB issued by IBRD under its Global Debt Issuance Facility. The net proceeds of the SDB will be used by IBRD to fund projects, programs, and activities in IBRD’s member countries designed to achieve positive social and environmental impacts and outcomes.”

It’s encouraging to see the use of sustainable development bonds as collateral investments in the catastrophe bond market expanding further beyond just the World Bank, to private insurance sector cat bond sponsors.

The World Bank itself was the first to do so this, since when insurance giant Assicurazioni Generali S.p.A. developed its framework for Green insurance-linked securities (ILS) which saw the proceeds of one of its catastrophe bonds used to refinance a green asset in an effort to help avoid greenhouse gas emissions.

But, Tokio Marine is the first private insurance or reinsurance market sponsor of a catastrophe bond to use a puttable SOFR linked Sustainable Development Bond from the IBRD, which marks an efficient way to structure a cat bond with collateral that can be put to work in supporting sustainable or ESG driven goals.

As a reminder, Gallagher Securities, the insurance-linked securities (ILS) specialist arm of reinsurance broker Gallagher Re was the sole structuring agent for this new cat bond for Tokio Marine, so will have been instrumental in incorporating the sustainable development bond as permitted investments for the collateral, within the overall cat bond structure for this issuance.

You can read all about this new Kizuna Re III Pte. Ltd. (Series 2024-1) catastrophe bond transaction and every other Tokio Marine sponsored cat bond in our Artemis Deal Directory.

Tokio Marine is first Japanese cat bond sponsor to use sustainable development bond was published by: www.Artemis.bm

Our catastrophe bond deal directory

Sign up for our free weekly email newsletter here.

Florida Citizens “will always be able to pay claims” – CEO Cerio

This content is copyright to www.artemis.bm and should not appear anywhere else, or an infringement has occurred. After Florida Governor Ron DeSantis claimed on television that the states Citizens Property Insurance Corporation “is not solvent”, the CEO of the insurer of last resort has responded […]

Industry Loss WarrantyThis content is copyright to www.artemis.bm and should not appear anywhere else, or an infringement has occurred.

After Florida Governor Ron DeSantis claimed on television that the states Citizens Property Insurance Corporation “is not solvent”, the CEO of the insurer of last resort has responded saying that Florida Citizens financial structure means it “will always be able to pay claims”.

The number of policies in-force at Florida Citizens has dipped to around 1.17 million at the end of February, down from a high of just over 1.4 million last year.

The number of policies in-force at Florida Citizens has dipped to around 1.17 million at the end of February, down from a high of just over 1.4 million last year.

That decline is thanks to depopulation activity, as private insurers take out some of its risk, but the state wind insurer of last resort has not seen its exposure decline especially, given the inflationary effects of the last year or so.

The financial adequacy of the Florida Citizens business model has come in for questioning of late, with US Senate Budget Committee Chairman Sheldon Whitehouse questioning the ability of Citizens to pay its claims without taxpayer support.

Which has led to a back and forth in letters between the Senator and Citizens CEO Tim Cerio, who has responded again to say that he believes Citizens has the ability to “always pay claims.”

“We believe we fully addressed the concerns raised in Chairman Whitehouse’s prior letter by pointing out in great detail the mechanisms under Florida law that ensure Citizens will always be able to pay the claims of its insureds. We also highlighted that neither Citizens, its predecessor entities, nor the State of Florida, have ever sought a federal bailout to cover hurricane losses. We also expressed concern that the Chairman’s letter could cause misplaced panic in a Florida insurance market well on its way to recovery,” Cerio explained.

Adding, “We will certainly meet with Budget Committee staff to provide information and documentation about Citizens’ structure, function, and claims paying ability. It is important to note that much of the information sought by the Budget Committee is already available online and is regularly discussed during our public board meetings.”

Cerio went on to explain, “It is also important to reiterate to Floridians in general, and Citizens policyholders in particular, that Citizens’ financial structure ensures that it will always be able to pay claims.”

He further said that, “we can think of no scenario in which Citizens would be required to seek federal financial assistance.”

Cerio said that should Citizens exhaust its surplus and extensive reinsurance coverage after a major hurricane or series of storms, it would be required under the Florida statutes to “levy surcharges on its policyholders and assessments on non-Citizens policyholders to eliminate any deficit.”

Cerio further said, “This is not mere speculation. Following the 2004-2005 hurricane seasons, Citizens successfully used this assessment mechanism to eliminate a deficit without federal assistance and with minimal impact on Florida insurance consumers.”

The Florida Citizens CEO then made a commitment to secure the necessary reinsurance and risk transfer for the coming hurricane season.

He stated that, “Going into the 2024 hurricane season, Citizens will have the reserves and reinsurance coverage to handle a 1-in-100-year storm without having to levy assessments on non-Citizens policyholders. To put that into context, Hurricane Andrew was a 1-in-43-year event while Hurricane Ivan was a 1-in-20 to 1-in-25-year hurricane.”

As we reported back in December 2023, Florida Citizens looks set to purchase even more reinsurance and catastrophe bond backed risk transfer in 2024, with its new layer structure, following the merging of its accounts, suggesting as much as $5.5 billion could be purchased this year.

Florida Citizens is expected to come back to market with catastrophe bonds in the coming month or so, with a large issuance of perhaps more than $1 billion anticipated, should the cat bond investor community be receptive.

At the same time, Citizens staff are already engaged with reinsurance and ILS markets to ensure it can secure the necessary reinsurance cover it needs from traditional and collateralized sources.

As we also reported back last December, Citizens will only have a $500 million Lightning Re Ltd. (Series 2023-1) industry loss trigger catastrophe bond left in-force, given it’s long-standing plans for an early redemption and other scheduled maturities of cat bonds, as it needs to buy afresh for the new combined tower reinsurance approach.

The cat bond and reinsurance market is expected to be receptive to Citizens needs, so it’s expected the insurer won’t be challenged to secure the necessary reinsurance it needs.

However, Citizens CEO Cerio did highlight once again the issue over whether the rates it is charging are sound in the first place.

Saying, “Although Citizens’ assessment authority means that it will always be able to pay claims, Citizens’ rates are currently actuarily unsound because of the “glide path.”

“It is critical that Citizens be able to charge actuarially sound rates to help minimize the risk of such assessments on the people of Florida.”

Meanwhile, Senator Whitehouse said Citizens has not addressed the concerns over its financial stability and claimed Citizens failed to cooperate with his investigation.

With reinsurance to cover a 1-in-100 year storm and the ability to levy assessments should that and whatever surplus is available be exhausted, it seems Citizens financial shape is no worse than it has been in the past and the reinsurance and cat bond market remains a critical source of risk financing.

As ever, risk commensurate pricing for inward policies remains key, as to does how that could also result in a much faster shift of policies back to the private marketplace, given private insurers would be more competitive then.

That could help to more rapidly reduce the exposure base of Citizens, so reducing the potential financial hit from major storms.

That, alongside measures to further increase the health of the Florida market seem the only reasonable way forwards, if the over-exposure of Citizens is seen as the problem.

Time would be well-spent on identifying how global insurance and reinsurance markets could better help, through the creation of capital structures to support more of Florida’s risk, if indeed reducing the chance of assessments and potential taxpayer levies is the real goal of lawmakers.

Florida Citizens “will always be able to pay claims” – CEO Cerio was published by: www.Artemis.bm

Our catastrophe bond deal directory

Sign up for our free weekly email newsletter here.

ILW market activity rising, as preparations for hurricane season begin

This content is copyright to www.artemis.bm and should not appear anywhere else, or an infringement has occurred. According to Artemis’ sources, activity in the industry-loss warranty (ILW) market has increased in the last few weeks, as reinsurance and insurance-linked securities (ILS) markets prepare for what […]

Industry Loss WarrantyThis content is copyright to www.artemis.bm and should not appear anywhere else, or an infringement has occurred.

According to Artemis’ sources, activity in the industry-loss warranty (ILW) market has increased in the last few weeks, as reinsurance and insurance-linked securities (ILS) markets prepare for what is anticipated to be an active 2024 Atlantic hurricane season.

![]() As we’ve reported, long-range seasonal forecasts for Atlantic hurricanes have suggested a challenging storm season could be ahead.

As we’ve reported, long-range seasonal forecasts for Atlantic hurricanes have suggested a challenging storm season could be ahead.

As we said, one forecaster called for a “hurricane season from hell” in 2024, while another is seen as particularly aggressive in calling for a large number of storms.

As we also reported from the SIFMA ILS event last week, forecaster Phil Klotzbach, Ph.D., from the Department of Atmospheric Science of the Colorado State University, said that the odds of La Niña are “pretty elevated” while conditions suggest we might not necessarily see as much re-curvature of storms as we did last year.

Forecasts are now concentrating minds on what could be ahead this hurricane season, with the Atlantic also at record warmth in the main development region, where storms form and fuel themselves.

With all that going on, it makes sense those holding portfolios of US coastal hurricane exposure would be preparing themselves and their portfolios for what could be a busy year of watching the tropics.

At the SIFMA ILS event in Miami last week, the subject of industry-loss warranties (ILW) and hedging preparations for hurricane season came up with a number of our contacts at ILS managers and investors in the sector.

All said that activity in ILW’s had picked up in just the last few weeks, while we also met some active buyers for the instruments.

It seems with a busy hurricane season forecast, the main route to hedging the portfolios of ILS investments continues to be the ILW, with some discussing the county-weighted industry-loss triggered instruments as well.

There was also discussion of industry-index products being constructed to more accurately reflect peak exposures in catastrophe bond portfolios, as tools for hedging against US wind exposure.

One source told us that ILW pricing has remained under-pressure through recent weeks, recall that Artemis’ data on industry loss warranty (ILW) price trends was already signalling this would occur during the last quarter of 2023.

Managers of portfolios of ILS instruments, reinsurance and retrocession with significant coastal wind exposure in the United States are keenly focused on ensuring their peaks are managed and concentration risk is controlled, we are told.

All of which makes perfect sense, in a year where such high hurricane numbers are being forecast currently.

We are also told that interest in ILW’s for hedging is being shown in some quarters of the London market as well, where retrocession needs have remained less sufficient than in previous years.

While the retro market was far more balanced at the January renewals, not everyone managed to secure the hedging capacity they needed and some were waiting to see how Atlantic conditions developed.

For those with capacity to deploy in support of industry-loss based reinsurance and retro, now might also be a good time to deploy it, as the forecasts may also assist in holding rates up a little more and some are suggesting that the softening in ILW triggered instruments that we’ve seen in catastrophe bonds of late may be slowing or even halting at this time.

We are told that capacity remains in ample supply for ILW’s and industry-loss index triggered instruments, albeit becoming more selective than it was around the January renewals.

Of course, there’s still a long way to go until the hurricane season peak and with more season hurricane forecasts due out over the next few weeks, it will be interesting to see if the activity levels in trading instruments such as ILW’s can further increase.

ILW market activity rising, as preparations for hurricane season begin was published by: www.Artemis.bm

Our catastrophe bond deal directory

Sign up for our free weekly email newsletter here.

Munich Re behind Hawaii coral reef parametric insurance renewal, coverage expands

This content is copyright to www.artemis.bm and should not appear anywhere else, or an infringement has occurred. An innovative parametric insurance product that provides protection to fund repairs following storm damage to coral reefs in Hawaii has been renewed and its coverage expanded, while global […]

Industry Loss WarrantyThis content is copyright to www.artemis.bm and should not appear anywhere else, or an infringement has occurred.

An innovative parametric insurance product that provides protection to fund repairs following storm damage to coral reefs in Hawaii has been renewed and its coverage expanded, while global reinsurance firm Munich Re is again backing the cover, which is arranged by WTW.

Back in November 2022, WTW alongside The Nature Conservancy launched the parametric coral reef insurance concept in the United States for the first time with a policy focused on Hawaii. Munich Re underwrote the risk for that first Hawaiian coral reef parametric insurance arrangement.

The same parametric risk transfer product concept had already been utilised in Mexico and was then expanded to also cover the Mesoamerican Reef system.

As we reported earlier this month, broker WTW has now taken the coral reef insurance concept across the globe to cover a South pacific coral reef in the Fiji archipelago as well.

Now, the Hawaii instance of the product has been renewed, with expanded coverage and higher payouts available, so that it can make more impact on the reef and the communities that rely on it.

The new parametric coral reef insurance policy expands coverage around the main Hawaiian islands and increases payouts after qualifying storms, WTW explained.

The new Hawaiian policy adds 314,976 square miles to the coverage area so that it can capture more storm events, with a maximum payout of $2 million total over the year-long policy period and $1 million possible per storm.

At the same time, the minimum payout after the parametric trigger is activated has doubled to $200,000, enabling a more meaningful post-storm response.

Payouts can be triggered when tropical storm winds of 50 knots or greater occur in the core of the coverage area.

Once again, a Munich Re insurance entity was selected as the coverage provider from seven competitive bids.

WTW said that more companies bid on this year’s policy, which it noted shows “increasing interest among insurers in nature-based solutions to protect against climate impacts.”

“Parametric insurance is increasingly demonstrating value in addressing disaster risk for natural assets, in this case providing Hawai’i with a tangible solution to quickly finance post- storm restoration activities that help reefs better recover and maintain resilience in the face of increasing climate impacts,” explained Simon Young, Senior Director in WTW’s Disaster Risk Finance and Parametrics team. “Increasing recognition of this value by conservation organisations, government bodies and other stakeholders on the demand side and by insurers on the supply side is mainstreaming parametric protections, driving accessibility and sustainability.”

“We are building something really transformative for communities and ecosystems as we respond to increasing storm activity associated with the climate crisis,” added Ulalia Woodside Lee, Executive Director, The Nature Conservancy, Hawai‘i and Palmyra. “The first policy provided momentum to develop response plans and partnerships. With these now in place and an increased minimum payout, we will be able to start damage assessments and reef repairs after a storm as soon as it’s safe to get in the water. This is important because corals must be reattached within several weeks after breaking or they will likely die.”

René Mück, Munich Re’s Global Head of Natural Catastrophe Parametrics, also said ”Using parametric risk transfer as a means to contribute to TNC’s conservation objectives in Hawaii aligns exactly with the objectives of Munich Re’s parametric business unit. We are proud to support TNC in Hawaii and appreciate the work with WTW on such initiatives.”

The parametric coral reef insurance product has already demonstrated its utility, when Hurricane Lisa’s landfall in Belize on November 2nd 2022 triggered the Mesoamerican Reef system parametric insurance product.

Munich Re behind Hawaii coral reef parametric insurance renewal, coverage expands was published by: www.Artemis.bm

Our catastrophe bond deal directory

Sign up for our free weekly email newsletter here.

Parametric insurance to cover South Pacific coral reef in Fiji archipelago

This content is copyright to www.artemis.bm and should not appear anywhere else, or an infringement has occurred. An innovative parametric insurance program has been taken across the globe to cover a South pacific coral reef in the Fiji archipelago, with broker WTW saying it will […]

Industry Loss WarrantyThis content is copyright to www.artemis.bm and should not appear anywhere else, or an infringement has occurred.

An innovative parametric insurance program has been taken across the globe to cover a South pacific coral reef in the Fiji archipelago, with broker WTW saying it will provide up to US $450,000 of cover for reef restoration and community assistance if cyclones hit.

The payout would go to Fiji’s island communities, if a cyclone hits the coral reef system of the South Pacific Ocean’s volcano-formed Lau Group of islands.

The payout would go to Fiji’s island communities, if a cyclone hits the coral reef system of the South Pacific Ocean’s volcano-formed Lau Group of islands.

The Indigenous people of Lau depend on the reef ecosystem as a source of food and income, so protecting it using a parametric risk transfer insurance product that will pay out after a cyclone strikes which could damage the reef, can enable the community to recover faster and put funds into reef conservation, restoration and resilience.

Development insurer and risk pool the Pacific Catastrophe Risk Insurance Company (PCRIC) is the insurer for this South Pacific parametric reef insurance, winning the bid after what WTW called “a competitive placement process.”

WTW worked with local correspondent broker Insurance Holdings (Pacific) Pte Ltd. and Fiji’s Vatuvara Foundation (VVF), which is the policyholder of the parametric insurance programme.

As well as helping to protect and repair the reef in the event of a cyclone, the parametric insurance payouts can be used to support the community with assistance activities to help address food and water security concerns caused by storm damage.

The initial coverage is for Vatuvara Island, a protected natural reserve; Yacata, where the local community resides; and Kaibu, the Vatuvara Private Islands Resort, while further sites in the Lau Seascape may be covered in future years.

Sarah Conway, Director and Ecosystem Resilience Lead, WTW, commented “We are grateful to BHP for supporting the design and implementation of the first coral reef insurance programme in Fiji. Building on lessons learned from our involvement with similar initiatives in other countries, this programme provides an exciting opportunity to innovate beyond rapid reef response to also include community assistance, enhancing the resilience of the ecosystem and those who depend on it.”

PCRIC CEO, Aholotu Palu, stated, “PCRIC is very pleased to demonstrate its commitment to serve non-sovereign entities with innovative parametric insurance products, in line with PCRIC’s mission to help the island communities of the Pacific to better prepare, structure and manage finances to foster disaster resilience and ensure rapid access to funds; the work of the Vatuvara Foundation, both in reef conservation and in local community empowerment, is recognised by the Government of Fiji as being in the national interest and consistent with development priorities, particularly the Blue Pacific Strategy, as well as commitments to climate change adaptation and disaster risk management.”

Katy Miller, Director, Vatuvara Foundation, added, “We are thankful that the innovative parametric policy will allow for the prompt access to funds following a destructive cyclone event to identify reef damage and assist reef recovery with a community-led team in Northern Lau. Increased frequency and severity of extreme weather events is expected in the area, and protecting natural ecosystems in the Lau Group is crucial to build long-term community resilience to anthropogenic threats including climate change.”

Ashley Preston, Head of Climate Resilience, BHP, also said, “BHP is funding an innovative parametric insurance product, which aims to support the conservation of coral reefs and surrounding local communities in Fiji’s northern Lau Group, and build the knowledge base for how similar financial products could be used to improve climate resilience. We are pleased to work with WTW and Vatuvara Foundation on this project, which supports BHP’s commitments to action on climate, conservation and empowering communities.”

Parametric insurance to cover South Pacific coral reef in Fiji archipelago was published by: www.Artemis.bm

Our catastrophe bond deal directory

Sign up for our free weekly email newsletter here.

Jireh Connect facilitates first industry loss warranty (ILW) placement

This content is copyright to www.artemis.bm and should not appear anywhere else, or an infringement has occurred. Jireh Connect, a technology platform that targets helping brokers place risk more efficiently with reinsurance and risk capital providers and manage the process more effectively, has announced the […]

Industry Loss WarrantyThis content is copyright to www.artemis.bm and should not appear anywhere else, or an infringement has occurred.

Jireh Connect, a technology platform that targets helping brokers place risk more efficiently with reinsurance and risk capital providers and manage the process more effectively, has announced the completion of its first placement, an industry loss warranty (ILW).

Jireh Connect has been launched by well-known Bermuda-based insurance-linked securities (ILS) market executive Sal Tucci.

Last year, Tucci launched Jireh Holdings Ltd., a company offering ILS risk transformation, fronting and advisory services to clients, with a broader insurance management offering in the works.

Jireh Connect was also launched, as Tucci sought to bring a technology platform to market that is built by brokers, for brokers, but makes their workflow easier and more efficient.

The Jireh Connect platform was soft-launched with one broker in Bermuda at the start of this year, successfully managing nearly $100 million in capacity across various ILW structures in its first month of operation, the company claimed today.

“We couldn’t be more pleased with the early success of Jireh Connect both in terms of facilitating its first bound transaction but also in having six markets actively engage on the platform,” explained Tucci. “We have had very positive feedback without our having made any prior public announcement of its availability to them. We credit this positive engagement to our very different approach to technology within our unique market.”

As we reported, ReFlex Solutions Ltd, an independent reinsurance brokerage headquartered in Bermuda launched by Neville Ching was said to be partnering with Jireh.

Jireh Connect enables brokers to coordinate reinsurance placements across their teams, acting as a front-office broker workbench, which can distribute deals, share documents with markets and capture external market feedback for users.

The platform can deliver analytics on market appetite and pricing in real-time, to help inform strategies when structuring transactions.

Jireh Connect was initially launched as a Minimum Viable Product (MVP) in 2024, with a focus on becoming a reinsurance broker workbench for ILW arrangements. New product offerings and system features are expected to be rolled out based on market demand, the company said.

Tucci said, “In the past, we’ve seen the roll out of numerous platforms in the reinsurance market developed by people from outside the industry who, looking in from the outside, endeavor to compress the value chain by disintermediating what they deem to be an inefficient market. We believe this is absolutely the wrong approach. Jireh Connect has been specifically designed ‘by brokers for brokers’ to complement the current reinsurance broker market process rather compete or replace it.”

Tucci further explained, “By way of example, despite the unquestionable convenience of ordering and paying for goods via your smartphone, there will always be customers who opt to wait in longer lines to order and pay cash. Many previous technology attempts within the reinsurance market make sense in theory and look great in a venture capital pitchbook, but the well-entrenched realities of how reinsurance is bought and sold cannot simply be ignored. Given our deep market experience, we designed Jireh Connect to provide the same efficacy to brokers through the platform even when customers or markets opt to communicate via email or in person. That is a significant differentiator between Jireh Connect and others that have come before us.”

Jireh Connect facilitates first industry loss warranty (ILW) placement was published by: www.Artemis.bm

Our catastrophe bond deal directory

Sign up for our free weekly email newsletter here.

Bermuda’s BMA aims to better facilitate parametric climate-related re/insurance

This content is copyright to www.artemis.bm and should not appear anywhere else, or an infringement has occurred. The Bermuda Monetary Authority (BMA) has laid out its plans for 2024, with Chief Executive Officer (CEO) Craig Swan highlighting specific opportunities in parametric risk transfer for climate […]

Industry Loss WarrantyThis content is copyright to www.artemis.bm and should not appear anywhere else, or an infringement has occurred.

The Bermuda Monetary Authority (BMA) has laid out its plans for 2024, with Chief Executive Officer (CEO) Craig Swan highlighting specific opportunities in parametric risk transfer for climate insurance.

The 2024 business plan of Bermuda’s financial regulator contains a focus on “initiatives and projects to achieve positive outcomes and strengthen Bermuda’s regulatory framework for the upcoming year.”

The 2024 business plan of Bermuda’s financial regulator contains a focus on “initiatives and projects to achieve positive outcomes and strengthen Bermuda’s regulatory framework for the upcoming year.”

Of relevance to the insurance, reinsurance and insurance-linked securities (ILS) community, the Bermuda Monetary Authority (BMA) expects to continue to work on enhancing its regulatory and supervisory regimes to meet the evolving needs of financial service companies today.

There will be further work on the Insurance Code of Conduct, “to uphold the importance of financial transparency, consumer protection and education initiatives,” the BMA explains.

While an Environmental, Social and Governance (ESG) model and a Sustainability Strategy are also key initiatives and here there are relevant items to look out for, for this industry.

BMA CEO Craig Swan said, “The Authority’s strategy is underpinned by deep expertise and cross-functional viewpoints designed to champion innovation. This plan’s many thoughtfully curated objectives will optimise excellence while simultaneously preparing the organisation to meet and address emerging challenges that impact the regulatory environment. In a continually fluctuating business climate, this approach enables the BMA to open new pathways for enhancing our abilities and innovative practices today and for many years to come.”

Swan also commented, “The pace of innovation is challenging organisations to remain agile and adapt how they work to meet the ebb and flow of their markets. From artificial intelligence and automation to decentralised finance and insurance-linked securities, the financial services industry has evolved markedly over the last few decades with increasingly transformative leaps forward each successive year.

“As firms confront issues such as inflationary pressures, relentless consumer demands, volatility in the commodity markets and extreme climate patterns, they are building systems to redefine and reimagine their future aspirations.”

The BMA intends to explore working with investment funds to “set up a new framework that facilitates the ability to designate certain Bermuda funds as ESG compliant,” Swan said.

This could be an interesting initiative for ILS managers, given there are plenty of ILS fund structures domiciled in Bermuda that could find an ESG framework appealing to look into.

The BMA also intends to prepare a consultation paper on a new climate risk disclosure framework for Bermuda commercial (re)insurers, Swan also explained.

But, perhaps most compelling in the current environment and in terms of opportunity, the BMA also intends to work in 2024 on “reviewing and, where applicable, updating other (re)insurance frameworks to better facilitate parametric climate-related insurance products.”

Bermuda has always considered itself as the world’s climate risk capital market and given the proliferation of catastrophe, weather and climate focused underwriting expertise in the islands insurers, reinsurers and of course ILS fund managers, there is clearly a wealth of experience and relevant knowledge, as well as ongoing business there.

If Bermuda can make its regulatory and supervisory regime even more relevant to underwriters of parametric climate risk insurance and reinsurance opportunities, while also finding ways to tap into the ILS market expertise on the island, the opportunity to attract and deploy climate risk capital out of the market there seems a worthwhile achievable goal.

The BMA has always followed a forward-thinking agenda and this year’s business plan again highlights the regulators’ ability to focus on emerging trends that can be drivers of future profit for Bermuda’s financial market and its participants.

Bermuda’s BMA aims to better facilitate parametric climate-related re/insurance was published by: www.Artemis.bm

Our catastrophe bond deal directory

Sign up for our free weekly email newsletter here.

2024 still an attractive entry point for insurance-linked securities investors: K2 Advisors

This content is copyright to www.artemis.bm and should not appear anywhere else, or an infringement has occurred. Despite some tightening of spreads in catastrophe bonds, overall K2 Advisors, the hedge fund focused investment management unit of Franklin Templeton, remains overweight the insurance-linked securities (ILS) asset […]

Industry Loss WarrantyThis content is copyright to www.artemis.bm and should not appear anywhere else, or an infringement has occurred.

Despite some tightening of spreads in catastrophe bonds, overall K2 Advisors, the hedge fund focused investment management unit of Franklin Templeton, remains overweight the insurance-linked securities (ILS) asset class, although finds industry-loss warranties (ILW’s) relatively less attractive at this time.

![]() Positively, K2 Advisors notes that while private ILS investments, such as collateralized reinsurance and retrocession, have faced challenges, some capital is expected to flow to the managers with the best track-records.

Positively, K2 Advisors notes that while private ILS investments, such as collateralized reinsurance and retrocession, have faced challenges, some capital is expected to flow to the managers with the best track-records.

But, even with this, K2 Advisors says the private ILS segment may still be capital constrained, overall, suggesting rates have a greater chance to remain elevated.

Giving its outlook for the first-quarter of 2024, the K2 Advisors hedge fund team state, “Following a record year of new issuance, the catastrophe bond market spread is elevated relative to historical levels, despite tightening throughout the year. We believe it remains an attractive entry point.”

They expect January reinsurance renewal pricing to have shown continued increases, year-on-year, while in the cat bond space they say, “We expect an active and attractively priced new issuance pipeline throughout the first half of 2024.”

Adding that, “We continue to overweight insurance-linked securities due to the diversification they can provide, along with a yield pick- up and idiosyncratic risk/return profile.”

Going into more detail, K2 Advisors highlights the record issuance and market size indicated by Artemis’ data on the catastrophe bond market.

The investment manager comments, “The combination of increasing investor demand for more senior insurance-linked securities (ILS) risk and higher total insured values, likely due to economic inflation, have led the catastrophe bond market to reach its largest size on record. While catastrophe bond pricing tightened throughout 2023, we are seeing signs of price stabilization.

“When coupled with a meaningful collateral return, we believe this provides an attractive entry point for investors into the catastrophe bond market.”

On the private ILS side, the improvements in price achieved at the January reinsurance renewals will play into, “increasing the risk adjusted price improvements the markets experienced during the January 2023 renewals,” K2 Advisors suggest.

Going into more detail to explain, “Given the strong performance across ILS risk segments throughout 2023, we expect some level of new capital to enter the market. On the private ILS side, we expect capital to gravitate toward managers who have demonstrated suitable loss-reserving policies. There will likely continue to be a supply/demand imbalance across private ILS strategies, with cedants retaining more risk on their balance sheets. Subsequently, this implies more volatility and lower-down loss exposure as many frequency losses may not be able to be hedged.”

Overall, K2 Advisors remains overweight the insurance-linked securities (ILS) asset class as a whole.

While this has been revised down from strongly overweight at Q4 2023, it’s important to note that the only segment of ILS that has actually been revised down is industry-loss warranties (ILW’s), which was taken down from strongly overweight, to overweight.

K2 Advisors outlook remains strongly overweight for catastrophe bonds, private ILS transactions and retrocession, while its position on life ILS remains underweight.

2024 still an attractive entry point for insurance-linked securities investors: K2 Advisors was published by: www.Artemis.bm

Our catastrophe bond deal directory

Sign up for our free weekly email newsletter here.

Aggregate reinsurance back on the table, lower layers see more support: Aon

This content is copyright to www.artemis.bm and should not appear anywhere else, or an infringement has occurred. A few signs emerged at the recent January 1st 2024 reinsurance renewals that bode well for protection buyers as we move through this year and into the next, […]

Industry Loss WarrantyThis content is copyright to www.artemis.bm and should not appear anywhere else, or an infringement has occurred.

A few signs emerged at the recent January 1st 2024 reinsurance renewals that bode well for protection buyers as we move through this year and into the next, as broker Aon highlighted that appetite is returning for some of the more challenged products and areas of the tower.

Over the last couple of years appetite to underwrite aggregate reinsurance or retrocession and lower layers of towers, had dried up in many cases, as reinsurers shied away from the business that had driven so many losses to them in the years prior.

Over the last couple of years appetite to underwrite aggregate reinsurance or retrocession and lower layers of towers, had dried up in many cases, as reinsurers shied away from the business that had driven so many losses to them in the years prior.

But certain factors are beginning to drive more appetite to support insurer and protection buyer demand for cover, in aggregate form or lower down.

Aon’s Reinsurance Solutions team recently highlighted that one of the factors driving more appetite for these risks is the fact many reinsurers remain keen to grow, but the growth opportunity higher-up may now be less available, or facing more competition and a slight softening of prices.

Joe Monaghan, Global Growth Leader at Aon’s Reinsurance Solutions said that, at the January renewals, “Some reinsurers were also more flexible in more challenging areas, such as peril-specific lower layers and aggregate covers, particularly where insurers were able to offer potentially profitable participations elsewhere.”

By supporting cedents needs, reinsurers are able to secure better shares higher-up, is a common feature of a reinsurance market that is now stabilising and where capital has been less of a challenge to secure.

As well as leverage, using the aggregate and lower layers as a way to elicit more share of the most attractive layers, there are also reinsurers that believe the market has reset considerably, with much higher pricing and updated terms making some of these previously more challenges areas of the catastrophe reinsurance tower appealing again.

“Following the resetting of the property market and much improved results in 2023, many reinsurers are now keen to grow. As a result, some reinsurers were more accommodating at the renewal when it came to meeting the needs of individual insurers in more challenging areas, such peril specific lower layers and aggregate covers, as well as reinstating certain terms and conditions,” Aon’s Reinsurance Solutions team explained in more detail.

They added, “The increases in deductible levels a year ago have helped mitigate reinsurer losses, and reinforced necessary changes in the insurance value chain that should ultimately result in a much healthier and more sustainable market.

“In the meantime, reinsurers that want to grow in the segment should look to support insurers with flexibility in lower layers, aggregate covers and structured solutions.”

At the 1/1 2024 renewals most reinsurers went into negotiations with a desire to grow in property catastrophe reinsurance, Aon explained.

This gave insurers the ability to use their upper-layers and specialty portfolios as ways to attract reinsurer support for lower catastrophe layers and frequency coverage.

Aon said that the reinsurers that were most supportive at renewals in 2023, have benefited most from these market dynamics in 2024.

Aggregate covers are now “back on the table” Aon believes, with the reinsurance broker saying that more reinsurers are willing to consider them, at the right price and terms, in 2024.

Aon has called before for the market to innovate to narrow the reinsurance protection gaps that had emerged, when it comes to secondary perils and frequency exposures.

As we also reported, model confidence had been a driver of lower certainty in the ability to predict secondary perils and we asked whether the pendulum may have swung too far on catastrophe risk retention as well.

Aon’s Joe Monaghan again highlighted the broker’s concerns over whether the reinsurance market has retrenched too far, away from frequency and secondary perils.

He said, “As capacity continues to build, there will be opportunities for insurers to buy additional limit at the top of programs, and for reinsurers to work with brokers and clients to share the burden of secondary perils more equitably.”

Monaghan believes the industry must work to restore more of a risk-sharing balance, “The increases in retentions a year ago have mitigated reinsurer losses and contributed to their positive returns in 2023. But this has come at the expense of increased retained losses for insurers many of whom are struggling to achieve the improvements in primary pricing and underwriting which are often slowed by regulatory approval process quickly enough given their limited sources of capital to sustain increased catastrophes.

“We must work collectively to create the solutions necessary to sustain re/insurance symbiosis.”

Through greater participation in appropriately structured and designed aggregate covers, as well as lower-layers and finding ways to support secondary peril coverage, while also working to enhance risk models for these exposures, the reinsurance market can rebuild a way back into the critical areas of towers.

But, it does need to happen in an equitable way, where the rates paid by cedents are risk commensurate and the proportion of risk retained to ceded does not shift dramatically back to how it was around five to ten years ago, at the height (low) of the last soft market.

Read all of our reinsurance renewal news coverage.

Aggregate reinsurance back on the table, lower layers see more support: Aon was published by: www.Artemis.bm

Our catastrophe bond deal directory

Sign up for our free weekly email newsletter here.