Texas Windstorm (TWIA) ready to sign reinsurance renewal lines this week

This content is copyright to www.artemis.bm and should not appear anywhere else, or an infringement has occurred. Having already secured its largest ever catastrophe bond issue this year, the Texas Windstorm Insurance Association (TWIA) is now ready to sign lines for its reinsurance renewal, with […]

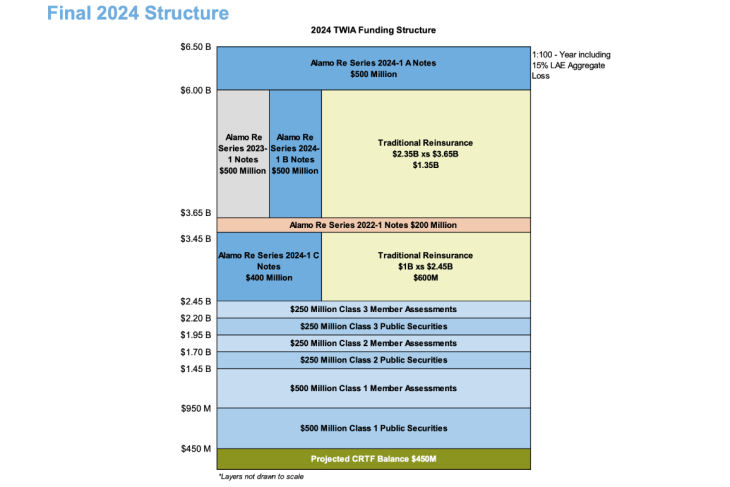

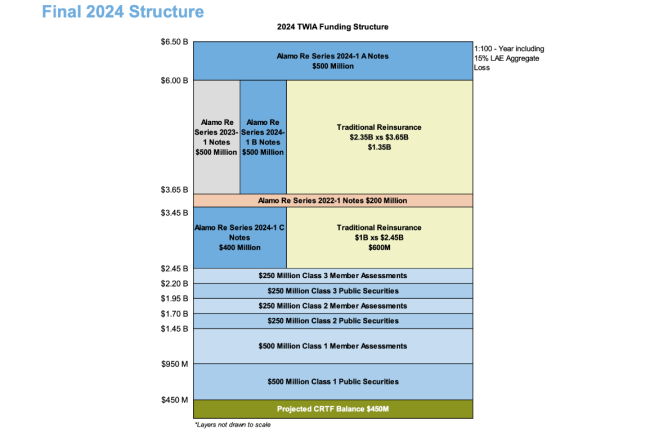

Industry Loss Warranty At $2.1bn, cat bonds will be TWIA’s biggest source of funding for 2024

This content is copyright to www.artemis.bm and should not appear anywhere else, or an infringement has occurred. For 2024, the funding tower of residual market insurer the Texas Windstorm Insurance Association (TWIA) will see catastrophe bonds as its largest component, providing 32% of the funding […]

Industry Loss Warranty

Allstate lifts Nationwide cat reinsurance tower by $1bn to $7.9bn, helped by cat bonds

This content is copyright to www.artemis.bm and should not appear anywhere else, or an infringement has occurred. Allstate has significantly lifted the top of its Nationwide excess catastrophe reinsurance tower to just over $7.9 billion, which is almost a $1 billion increase from the prior […]

Industry Loss Warranty

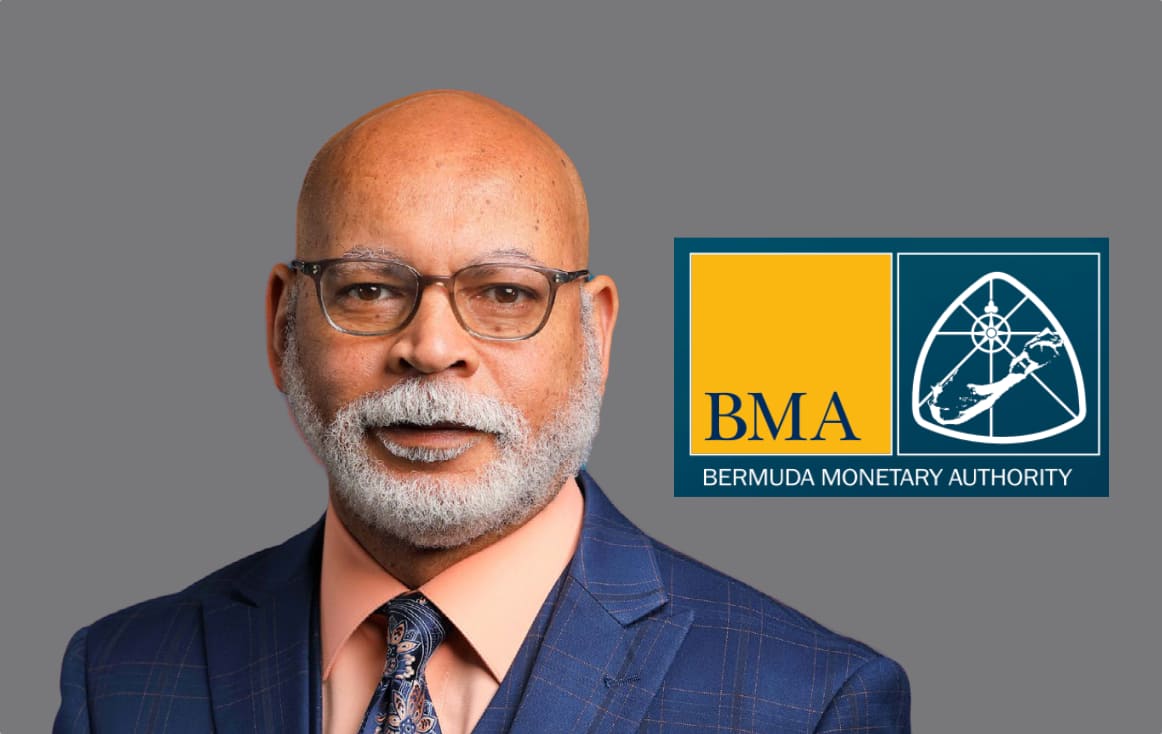

Bermuda’s BMA aims to better facilitate parametric climate-related re/insurance

This content is copyright to www.artemis.bm and should not appear anywhere else, or an infringement has occurred. The Bermuda Monetary Authority (BMA) has laid out its plans for 2024, with Chief Executive Officer (CEO) Craig Swan highlighting specific opportunities in parametric risk transfer for climate […]

Industry Loss WarrantyThis content is copyright to www.artemis.bm and should not appear anywhere else, or an infringement has occurred.

The Bermuda Monetary Authority (BMA) has laid out its plans for 2024, with Chief Executive Officer (CEO) Craig Swan highlighting specific opportunities in parametric risk transfer for climate insurance.

The 2024 business plan of Bermuda’s financial regulator contains a focus on “initiatives and projects to achieve positive outcomes and strengthen Bermuda’s regulatory framework for the upcoming year.”

The 2024 business plan of Bermuda’s financial regulator contains a focus on “initiatives and projects to achieve positive outcomes and strengthen Bermuda’s regulatory framework for the upcoming year.”

Of relevance to the insurance, reinsurance and insurance-linked securities (ILS) community, the Bermuda Monetary Authority (BMA) expects to continue to work on enhancing its regulatory and supervisory regimes to meet the evolving needs of financial service companies today.

There will be further work on the Insurance Code of Conduct, “to uphold the importance of financial transparency, consumer protection and education initiatives,” the BMA explains.

While an Environmental, Social and Governance (ESG) model and a Sustainability Strategy are also key initiatives and here there are relevant items to look out for, for this industry.

BMA CEO Craig Swan said, “The Authority’s strategy is underpinned by deep expertise and cross-functional viewpoints designed to champion innovation. This plan’s many thoughtfully curated objectives will optimise excellence while simultaneously preparing the organisation to meet and address emerging challenges that impact the regulatory environment. In a continually fluctuating business climate, this approach enables the BMA to open new pathways for enhancing our abilities and innovative practices today and for many years to come.”

Swan also commented, “The pace of innovation is challenging organisations to remain agile and adapt how they work to meet the ebb and flow of their markets. From artificial intelligence and automation to decentralised finance and insurance-linked securities, the financial services industry has evolved markedly over the last few decades with increasingly transformative leaps forward each successive year.

“As firms confront issues such as inflationary pressures, relentless consumer demands, volatility in the commodity markets and extreme climate patterns, they are building systems to redefine and reimagine their future aspirations.”

The BMA intends to explore working with investment funds to “set up a new framework that facilitates the ability to designate certain Bermuda funds as ESG compliant,” Swan said.

This could be an interesting initiative for ILS managers, given there are plenty of ILS fund structures domiciled in Bermuda that could find an ESG framework appealing to look into.

The BMA also intends to prepare a consultation paper on a new climate risk disclosure framework for Bermuda commercial (re)insurers, Swan also explained.

But, perhaps most compelling in the current environment and in terms of opportunity, the BMA also intends to work in 2024 on “reviewing and, where applicable, updating other (re)insurance frameworks to better facilitate parametric climate-related insurance products.”

Bermuda has always considered itself as the world’s climate risk capital market and given the proliferation of catastrophe, weather and climate focused underwriting expertise in the islands insurers, reinsurers and of course ILS fund managers, there is clearly a wealth of experience and relevant knowledge, as well as ongoing business there.

If Bermuda can make its regulatory and supervisory regime even more relevant to underwriters of parametric climate risk insurance and reinsurance opportunities, while also finding ways to tap into the ILS market expertise on the island, the opportunity to attract and deploy climate risk capital out of the market there seems a worthwhile achievable goal.

The BMA has always followed a forward-thinking agenda and this year’s business plan again highlights the regulators’ ability to focus on emerging trends that can be drivers of future profit for Bermuda’s financial market and its participants.

Bermuda’s BMA aims to better facilitate parametric climate-related re/insurance was published by: www.Artemis.bm

Our catastrophe bond deal directory

Sign up for our free weekly email newsletter here.

2024 still an attractive entry point for insurance-linked securities investors: K2 Advisors

This content is copyright to www.artemis.bm and should not appear anywhere else, or an infringement has occurred. Despite some tightening of spreads in catastrophe bonds, overall K2 Advisors, the hedge fund focused investment management unit of Franklin Templeton, remains overweight the insurance-linked securities (ILS) asset […]

Industry Loss WarrantyThis content is copyright to www.artemis.bm and should not appear anywhere else, or an infringement has occurred.

Despite some tightening of spreads in catastrophe bonds, overall K2 Advisors, the hedge fund focused investment management unit of Franklin Templeton, remains overweight the insurance-linked securities (ILS) asset class, although finds industry-loss warranties (ILW’s) relatively less attractive at this time.

![]() Positively, K2 Advisors notes that while private ILS investments, such as collateralized reinsurance and retrocession, have faced challenges, some capital is expected to flow to the managers with the best track-records.

Positively, K2 Advisors notes that while private ILS investments, such as collateralized reinsurance and retrocession, have faced challenges, some capital is expected to flow to the managers with the best track-records.

But, even with this, K2 Advisors says the private ILS segment may still be capital constrained, overall, suggesting rates have a greater chance to remain elevated.

Giving its outlook for the first-quarter of 2024, the K2 Advisors hedge fund team state, “Following a record year of new issuance, the catastrophe bond market spread is elevated relative to historical levels, despite tightening throughout the year. We believe it remains an attractive entry point.”

They expect January reinsurance renewal pricing to have shown continued increases, year-on-year, while in the cat bond space they say, “We expect an active and attractively priced new issuance pipeline throughout the first half of 2024.”

Adding that, “We continue to overweight insurance-linked securities due to the diversification they can provide, along with a yield pick- up and idiosyncratic risk/return profile.”

Going into more detail, K2 Advisors highlights the record issuance and market size indicated by Artemis’ data on the catastrophe bond market.

The investment manager comments, “The combination of increasing investor demand for more senior insurance-linked securities (ILS) risk and higher total insured values, likely due to economic inflation, have led the catastrophe bond market to reach its largest size on record. While catastrophe bond pricing tightened throughout 2023, we are seeing signs of price stabilization.

“When coupled with a meaningful collateral return, we believe this provides an attractive entry point for investors into the catastrophe bond market.”

On the private ILS side, the improvements in price achieved at the January reinsurance renewals will play into, “increasing the risk adjusted price improvements the markets experienced during the January 2023 renewals,” K2 Advisors suggest.

Going into more detail to explain, “Given the strong performance across ILS risk segments throughout 2023, we expect some level of new capital to enter the market. On the private ILS side, we expect capital to gravitate toward managers who have demonstrated suitable loss-reserving policies. There will likely continue to be a supply/demand imbalance across private ILS strategies, with cedants retaining more risk on their balance sheets. Subsequently, this implies more volatility and lower-down loss exposure as many frequency losses may not be able to be hedged.”

Overall, K2 Advisors remains overweight the insurance-linked securities (ILS) asset class as a whole.

While this has been revised down from strongly overweight at Q4 2023, it’s important to note that the only segment of ILS that has actually been revised down is industry-loss warranties (ILW’s), which was taken down from strongly overweight, to overweight.

K2 Advisors outlook remains strongly overweight for catastrophe bonds, private ILS transactions and retrocession, while its position on life ILS remains underweight.

2024 still an attractive entry point for insurance-linked securities investors: K2 Advisors was published by: www.Artemis.bm

Our catastrophe bond deal directory

Sign up for our free weekly email newsletter here.

Aggregate reinsurance back on the table, lower layers see more support: Aon

This content is copyright to www.artemis.bm and should not appear anywhere else, or an infringement has occurred. A few signs emerged at the recent January 1st 2024 reinsurance renewals that bode well for protection buyers as we move through this year and into the next, […]

Industry Loss WarrantyThis content is copyright to www.artemis.bm and should not appear anywhere else, or an infringement has occurred.

A few signs emerged at the recent January 1st 2024 reinsurance renewals that bode well for protection buyers as we move through this year and into the next, as broker Aon highlighted that appetite is returning for some of the more challenged products and areas of the tower.

Over the last couple of years appetite to underwrite aggregate reinsurance or retrocession and lower layers of towers, had dried up in many cases, as reinsurers shied away from the business that had driven so many losses to them in the years prior.

Over the last couple of years appetite to underwrite aggregate reinsurance or retrocession and lower layers of towers, had dried up in many cases, as reinsurers shied away from the business that had driven so many losses to them in the years prior.

But certain factors are beginning to drive more appetite to support insurer and protection buyer demand for cover, in aggregate form or lower down.

Aon’s Reinsurance Solutions team recently highlighted that one of the factors driving more appetite for these risks is the fact many reinsurers remain keen to grow, but the growth opportunity higher-up may now be less available, or facing more competition and a slight softening of prices.

Joe Monaghan, Global Growth Leader at Aon’s Reinsurance Solutions said that, at the January renewals, “Some reinsurers were also more flexible in more challenging areas, such as peril-specific lower layers and aggregate covers, particularly where insurers were able to offer potentially profitable participations elsewhere.”

By supporting cedents needs, reinsurers are able to secure better shares higher-up, is a common feature of a reinsurance market that is now stabilising and where capital has been less of a challenge to secure.

As well as leverage, using the aggregate and lower layers as a way to elicit more share of the most attractive layers, there are also reinsurers that believe the market has reset considerably, with much higher pricing and updated terms making some of these previously more challenges areas of the catastrophe reinsurance tower appealing again.

“Following the resetting of the property market and much improved results in 2023, many reinsurers are now keen to grow. As a result, some reinsurers were more accommodating at the renewal when it came to meeting the needs of individual insurers in more challenging areas, such peril specific lower layers and aggregate covers, as well as reinstating certain terms and conditions,” Aon’s Reinsurance Solutions team explained in more detail.

They added, “The increases in deductible levels a year ago have helped mitigate reinsurer losses, and reinforced necessary changes in the insurance value chain that should ultimately result in a much healthier and more sustainable market.

“In the meantime, reinsurers that want to grow in the segment should look to support insurers with flexibility in lower layers, aggregate covers and structured solutions.”

At the 1/1 2024 renewals most reinsurers went into negotiations with a desire to grow in property catastrophe reinsurance, Aon explained.

This gave insurers the ability to use their upper-layers and specialty portfolios as ways to attract reinsurer support for lower catastrophe layers and frequency coverage.

Aon said that the reinsurers that were most supportive at renewals in 2023, have benefited most from these market dynamics in 2024.

Aggregate covers are now “back on the table” Aon believes, with the reinsurance broker saying that more reinsurers are willing to consider them, at the right price and terms, in 2024.

Aon has called before for the market to innovate to narrow the reinsurance protection gaps that had emerged, when it comes to secondary perils and frequency exposures.

As we also reported, model confidence had been a driver of lower certainty in the ability to predict secondary perils and we asked whether the pendulum may have swung too far on catastrophe risk retention as well.

Aon’s Joe Monaghan again highlighted the broker’s concerns over whether the reinsurance market has retrenched too far, away from frequency and secondary perils.

He said, “As capacity continues to build, there will be opportunities for insurers to buy additional limit at the top of programs, and for reinsurers to work with brokers and clients to share the burden of secondary perils more equitably.”

Monaghan believes the industry must work to restore more of a risk-sharing balance, “The increases in retentions a year ago have mitigated reinsurer losses and contributed to their positive returns in 2023. But this has come at the expense of increased retained losses for insurers many of whom are struggling to achieve the improvements in primary pricing and underwriting which are often slowed by regulatory approval process quickly enough given their limited sources of capital to sustain increased catastrophes.

“We must work collectively to create the solutions necessary to sustain re/insurance symbiosis.”

Through greater participation in appropriately structured and designed aggregate covers, as well as lower-layers and finding ways to support secondary peril coverage, while also working to enhance risk models for these exposures, the reinsurance market can rebuild a way back into the critical areas of towers.

But, it does need to happen in an equitable way, where the rates paid by cedents are risk commensurate and the proportion of risk retained to ceded does not shift dramatically back to how it was around five to ten years ago, at the height (low) of the last soft market.

Read all of our reinsurance renewal news coverage.

Aggregate reinsurance back on the table, lower layers see more support: Aon was published by: www.Artemis.bm

Our catastrophe bond deal directory

Sign up for our free weekly email newsletter here.

Beazley Smart Tracker capital raise “heavily oversubscribed” for 2024: Roscoe

This content is copyright to www.artemis.bm and should not appear anywhere else, or an infringement has occurred. The capital raise for the 2024 underwriting year for London headquartered specialty insurance and reinsurance firm Beazley’s third-party capital backed Smart Tracker syndicate 5623 was “heavily oversubscribed” and […]

Industry Loss WarrantyThis content is copyright to www.artemis.bm and should not appear anywhere else, or an infringement has occurred.

The capital raise for the 2024 underwriting year for London headquartered specialty insurance and reinsurance firm Beazley’s third-party capital backed Smart Tracker syndicate 5623 was “heavily oversubscribed” and the structure remains on-track to deliver a fourth consecutive year of underwriting profits to backers.

![]() This is according to Will Roscoe, Head of Portfolio Underwriting at Beazley, and the Active Underwriter for the firm’s Smart Tracker Syndicate 5623 and its ESG Syndicate 4321.

This is according to Will Roscoe, Head of Portfolio Underwriting at Beazley, and the Active Underwriter for the firm’s Smart Tracker Syndicate 5623 and its ESG Syndicate 4321.

Roscoe was reflecting on a strong 2023 for the Beazley Portfolio Underwriting team he runs and looking ahead to 2024 in a post on Linkedin.

He explained that, “The Beazley Smart Tracker syndicate 5623 has delivered its 2023 business plan having underwritten $425m Gross Written Premium.”

Further stating that, “We are on track to return a fourth straight underwriting profit to our investors when we announce our 2021 year of account result next year.”

The third-party capital backed Smart Tracker is one of Beazley’s underwriting structures at Lloyd’s that attracts a diverse range of institutional investor capital.

It is considered akin to an insurance-linked strategy, attracting some well-known pension investors that allocate to insurance-linked securities (ILS).

The Smart Tracker both augments Beazley’s underwriting capacity in the market, while also enabling it to earn fee-like income and offer low-cost risk capital to clients.

The newer ESG Syndicate 4321 is also popular with third-party capital and delivers similar benefits to Beazley, while also providing a home for underwriting capital that targets ESG aligned opportunities.

Roscoe highlighted the demand from investors for the strategies, saying, “Our capital raise for the 2024 underwriting year of account was heavily oversubscribed, reflecting the strong demand we have seen from our third-party capital investors.”

He also highlighted that his team has launched additional underwriting facilities, saying, “We are proud to be leading the London market’s Smart Follow underwriting strategy.”

Beazley has ambitions to continue growing out the Smart Tracker and related facilities.

Roscoe said, “Looking ahead to 2024 we are poised to deliver further growth, with an ambitious plan to underwrite $525m in premium, taking advantage of continued excellent market conditions.”

The Smart Tracker has proved a popular structure for investors looking to participate in the returns of the Lloyd’s market, as it follows a curated approach to tracking and following the performance of some of the best underwriters.

Beazley Smart Tracker capital raise “heavily oversubscribed” for 2024: Roscoe was published by: www.Artemis.bm

Our catastrophe bond deal directory

Sign up for our free weekly email newsletter here.

Swiss Re: $50m cyber ILW is “novel and complementary” retro cover

This content is copyright to www.artemis.bm and should not appear anywhere else, or an infringement has occurred. Swiss Re secured $50 million of cyber industry-loss warranty (ILW) cover recently in a transaction that the broker involved, Gallagher Re, is hailing as the first cyber retrocession […]

Industry Loss WarrantyThis content is copyright to www.artemis.bm and should not appear anywhere else, or an infringement has occurred.

Swiss Re secured $50 million of cyber industry-loss warranty (ILW) cover recently in a transaction that the broker involved, Gallagher Re, is hailing as the first cyber retrocession ILW ever traded.

![]() The transaction was supported by a number of specialist reinsurers, according to Gallagher Re.

The transaction was supported by a number of specialist reinsurers, according to Gallagher Re.

We cannot be certain, but there is a chance that this $50 million cyber industry-loss warranty (ILW) trade is actually the same trade as the 144A securitized Matterhorn Re Ltd. (Series 2023-1) issuance that we covered last year.

It’s possible Swiss Re simply transformed the ILW arrangement into a 144A format, to make it more broadly acceptable to catastrophe bond investors and funds.

It is also possible that the $50 million cyber ILW is in addition to the $50 million of cyber industry loss protection from the Matterhorn Re cat bond, which is perhaps more notable as it shows Swiss Re securing even more industry-loss based cyber retro.

Either way, the coverage provided by the $50 million cyber industry-loss warranty (ILW) protects Swiss Re against catastrophic US cyber events, including coverage for widespread malicious ransomware or malware, prolonged catastrophic cloud outage and systemic data breach, the companies involved explained.

Commenting on the coverage provided, Nick Meuli, Head of P&C Capacity Management at Swiss Re, said, “Accessing alternative external sources of cyber capacity to support our inwards cyber business has been a key priority for us.

“We are very pleased to have secured significant ILW protection which provides yet another novel and complementary cover for our cyber portfolio.”

Ian Newman, Global Head of Cyber at Gallagher Re, further explained, “Alongside traditional retro and cat bond solutions, we believe ILWs and parametric solutions will form a critical part of the cyber value chain in the coming years.

“We are proud to have delivered another market first on behalf of Swiss Re, a true market leader in this space.”

Gallagher Re said that, “Swiss Re’s purchase of cyber market’s first Retro ILW comes after years of work in the field and reflects a market which is growing in confidence.”

The broker is expecting further growth of the cyber insurance-linked securities (ILS) market, with more cyber cat bonds expected to be issued.

Theo Norris, Head of Cyber ILS at Gallagher Re, added, “Successfully executing this innovative solution for Swiss Re is another step forward in broadening the potential access for capital to enter the Cyber insurance space and to provide effective, alternative solutions for insurers and reinsurers alike.”

As said, this could be the same arrangement as the Matterhorn Re 144A cyber industry-loss securitization that we had covered back in December, which was the first industry-loss triggered cyber cat bond to hit the market.

That deal took the number of completed cyber cat bonds to four, with four deals priced and a range of structural feature that can be incorporated into cyber cat bonds, including the industry-loss trigger, now tested and approved by the investor base.

As we reported at the time, the industry-loss trigger uses data from CyberAcuView, with PERILS acting as the reporting agency. The industry-loss trigger attaches at a $9 billion US cyber insurance industry loss, as reported by the agencies above.

You can read all about the industry-loss trigger cyber catastrophe bond from Swiss Re, the Matterhorn Re Ltd. (Series 2023-1) transaction, and every other cat bond ever issued in the Artemis Deal Directory.

Swiss Re: $50m cyber ILW is “novel and complementary” retro cover was published by: www.Artemis.bm

Our catastrophe bond deal directory

Sign up for our free weekly email newsletter here.

City National Rochdale mutual ILW fund grows further to $218m

This content is copyright to www.artemis.bm and should not appear anywhere else, or an infringement has occurred. The City National Rochdale Select Strategies Fund, a US mutual insurance-linked securities (ILS) fund focused on investments into industry-loss warranties (ILW’s) and industry-index trigger catastrophe bonds, has continued […]

Industry Loss WarrantyThis content is copyright to www.artemis.bm and should not appear anywhere else, or an infringement has occurred.

The City National Rochdale Select Strategies Fund, a US mutual insurance-linked securities (ILS) fund focused on investments into industry-loss warranties (ILW’s) and industry-index trigger catastrophe bonds, has continued to grow, to reach almost $218 million as of October 31st 2023.

![]() Investment adviser City National Rochdale (CNR) offers an industry-loss warranty (ILW) and industry-index trigger focused mutual insurance-linked securities (ILS) fund strategy in the United States.

Investment adviser City National Rochdale (CNR) offers an industry-loss warranty (ILW) and industry-index trigger focused mutual insurance-linked securities (ILS) fund strategy in the United States.

The capital from the City National Rochdale Select Strategies Fund is allocated to opportunities that are portfolio managed by the ILS investment team at Neuberger Berman and housed in its segregated account vehicle.

With ILW rates-on-line remaining elevated, despite some deceleration in recent quarters as Artemis’ index of ILW pricing shows, the opportunity remains very attractive and the CNR fund has attracted new inflows in the last year as a result.

The fund has experienced a 13% increase in invested assets over the year to October 31st 2023, reaching that date with over $213 million of ILW and cat bond assets invested in.

The total net assets of the ILW fund is a little higher, at the $218 million level.

But, the cost of the invested assets is just $155.6 million, suggesting a significant appreciation and return generated for investors in the fund.

Over a one-year period, the net asset value return of the fund reached just over 14.2%, according to some mutual fund reporting websites.

For this fund, the end of year renewals will likely be the key trading point of the last year, given ILW market activity was somewhat more subdued around the mid-year renewals of 2023.

So it will be interesting to see whether this ILW focused mutual fund can extend its assets growth further and faster when the next quarterly report is made.

View our chart of industry-loss warranty (ILW) price trends here.

City National Rochdale mutual ILW fund grows further to $218m was published by: www.Artemis.bm

Our catastrophe bond deal directory

Sign up for our free weekly email newsletter here.

TransRe’s Craig Hupper to retire from company at year-end

This content is copyright to www.artemis.bm and should not appear anywhere else, or an infringement has occurred. Craig Hupper, an executive from global reinsurance company TransRe who is well-known and liked in the insurance-linked securities (ILS) community, is set to retire from the firm at […]

Industry Loss WarrantyThis content is copyright to www.artemis.bm and should not appear anywhere else, or an infringement has occurred.

Craig Hupper, an executive from global reinsurance company TransRe who is well-known and liked in the insurance-linked securities (ILS) community, is set to retire from the firm at the end of this year, Artemis has learned.

Craig Hupper is a Senior Vice President at TransRe and currently holds the title of Managing Director, Head of Sustainability and Resilience.

Craig Hupper is a Senior Vice President at TransRe and currently holds the title of Managing Director, Head of Sustainability and Resilience.

But, through much of his career at the reinsurance company he has developed and led TransRe’s third-party capital and ILS offerings.

Hupper already had insurance and reinsurance market experience, gained on the broking side of the market, when he joined TransRe back in 1998.

At first Hupper was a VP of non-traditional underwriting and the Head of Retrocession for the reinsurer, after which he became an SVP and the Director of Risk Management, before moving over to dedicate his time to further developing third-party capital initiatives at TransRe in 2013.

Hupper has been instrumental in the build-out of the third-party capital and insurance-linked securities (ILS) offering at TransRe, as well as in the development of investor relationships.

His work at the company included, leading on the launch of TransRe’s long-established collateralized reinsurance sidecar vehicle, Pangaea, as well as other initiatives that connected institutional investor capital with reinsurance risk (private ILS arrangements) and also the launch of TransRe’s Bowline Re catastrophe bond program.

Hupper then shifted roles at TransRe in 2021, taking on a new position leading Environmental, Social & Governance (ESG) at the reinsurance firm.

Mike Torre, who had joined TransRe from broker Aon around five years ago, took over the lead at TransRe Capital Partners, managing the reinsurers third-party capital initiatives and relationships that year, as Hupper’s full-time focus moved to the new role.

Torre continues in that Capital Partners lead role today, supporting TransRe’s existing and future partnerships with alternative capital providers.

With Hupper now set to retire from TransRe at the end of this year, the company had already promoted existing employee Brett Denyer to become Head of Sustainability and Resilience earlier this year.

Denyer had already been a key member of TransRe’s Task Force on ESG for a number of years, and has also helped the reinsurer in further integrating ESG considerations into underwriting processes and decision-making.

While Hupper is now departing TransRe after his roughly 26 years of service, he intends to remain connected to the insurance-linked securities (ILS) market and be involved in selected reinsurance, ILS and sustainability focused ventures, following some time off early in 2024.

Hupper spoke at our New York conference back in 2022, participating in a panel session focused on ESG in ILS, which you can still watch here.

TransRe’s Craig Hupper to retire from company at year-end was published by: www.Artemis.bm

Our catastrophe bond deal directory

Sign up for our free weekly email newsletter here.

Higher-layer retro & ILW’s seeing price pressure, competition

This content is copyright to www.artemis.bm and should not appear anywhere else, or an infringement has occurred. Sources of retrocessional reinsurance capital appear in greater supply at this January renewal season than a year ago, which has applied some pressure to rates-on-line at higher, more […]

Industry Loss WarrantyThis content is copyright to www.artemis.bm and should not appear anywhere else, or an infringement has occurred.

Sources of retrocessional reinsurance capital appear in greater supply at this January renewal season than a year ago, which has applied some pressure to rates-on-line at higher, more remote layers, while also shifting more of the balance of power back towards buyers in some cases, we understand.

We’re told a number of retro programs have been placed with rates down approximately ~10% to ~15% for the January 2024 renewals.

We’re told a number of retro programs have been placed with rates down approximately ~10% to ~15% for the January 2024 renewals.

With ultimate net loss (UNL) traditional and collateralized retrocession seen as particularly competitive, given its broader coverage, this has also had a knock-on effect on the industry loss warranty (ILW) market, sources have told Artemis.

Increased appetites have been seen for the higher-layers of certain retrocession towers, resulting in a softening of pricing for these more risk-remote tranches of the retro market and the same can be said for the ILW marketplace.

This mirrors what has been seen in the catastrophe bond market, where risk-adjusted pricing has declined somewhat in the fourth-quarter of the year.

At the same time as appetites increasing, capital is more readily available this year and some traditional markets continue to display elevated desire to write catastrophe retro, which has lifted competition somewhat further.

Sources said that this has put more power back in the hands of retro buyers for 2024.

Capacity providers have held all the cards in retro over the last year or so. But, as appetites recover and some traditional markets look to secure greater shares, while the pricing still remains harder than before, this is applying pressure to retrocession rates and driving more power back to the protection buyer side.

It’s important to note, that conditions are not uniform and there remains a great deal of differentiation, we’re told.

But we understand some long-standing and trusted buyers of retro are seeing improved pricing and in some cases also certain terms, at the January 2024 renewals, while others are in the main experiencing a relatively flat and stable retro renewal, but with more capacity seemingly available in certain pockets.

We’re told that some retro programs have been placed with rates-on-line down ~10% to ~15%.

At the same time, where a year ago these programs may have seen numerous slips with individualised terms for different markets, the number of slips has been reduced dramatically and markets are less able to negotiate their own agreements this year.

Leading to a more balanced and even marketplace for retrocession, where it is the higher-layers that are seeing most price pressure, but the lower, higher-risk layers of retro continue to remain firm and largely with relatively flat pricing.

Some retro programs have been over-placed, given the higher appetites and greater availability of capacity, meaning some markets are getting signed down and taking less than they had hoped for.

So far, we’ve heard attachments are largely flat in retrocession, albeit with some adjustments seen, that have improved terms a little for buyers that felt particularly penalised in the last round of renewals.

Secondary perils remain out of favour though and tighter peril definitions and naming remains the norm.

In the market for industry loss warranties (ILW’s) conditions have been similar, with quotes for low rate-on-line ILW’s, so the more risk-remote, seen as down around the ~10% area, we’re told.

However, much of the ILW buying at year-end tends to begin as the retro renewals near or reach completion.

We’re told there remains retro capacity available which could affect the dynamics in the ILW market this new year, given UNL retro can often be seen as a better buy in coverage terms, if the pricing is conducive.

Higher rate-on-line (ROL) ILW’s in the market (so riskier) are producing quotes that are relatively flat, we understand, which is said to be turning heads back towards traditional and collateralized UNL retro protection as well and not driving the orders some might have anticipated.

While there remains a high level of appetite for deploying capital to ILW’s and some index markets are said to have funds available to deploy, there could be a bit of a delay in ILW’s starting to trade this year it seems, while the traditional retro renewals run their course.

As we have been reporting, the main reinsurance renewals appear largely stable, mostly flattish, with higher-layers experiencing the most price pressure and reinsurers largely holding the line on terms and conditions.

Retrocession appears quite similar, although perhaps with larger price declines being seen where competition and pressure from capital is greatest.

With some softening being seen, there is likely an element of certain markets aiming to make hay at this point in the cycle.

This had been forecast, with the areas that will see the greatest pressure on rates at the January 2024’s renewals always anticipated to have been in the higher-layers and the retrocession market.

Read all of our reinsurance renewals coverage here.

Higher-layer retro & ILW’s seeing price pressure, competition was published by: www.Artemis.bm

Our catastrophe bond deal directory

Sign up for our free weekly email newsletter here.

When it comes to ESG, ILS manager selection matters: Frontier Advisors

This content is copyright to www.artemis.bm and should not appear anywhere else, or an infringement has occurred. While the insurance-linked securities (ILS) sector has strengthened its governance practices considerably in recent years, when it comes to environmental, social and governance (ESG) considerations, ILS manager selection […]

Industry Loss WarrantyThis content is copyright to www.artemis.bm and should not appear anywhere else, or an infringement has occurred.

While the insurance-linked securities (ILS) sector has strengthened its governance practices considerably in recent years, when it comes to environmental, social and governance (ESG) considerations, ILS manager selection really matters, as there is variation in how ESG has been adopted and practices are followed, according to Frontier Advisors.

![]() Frontier Advisors is an Australian independent investment consultant with experience advising regional institutional investors that allocate to the insurance-linked securities (ILS) asset class.

Frontier Advisors is an Australian independent investment consultant with experience advising regional institutional investors that allocate to the insurance-linked securities (ILS) asset class.

In a recent paper, Isabella Milazzo, a Consultant in the Alternatives Research Team at Frontier Advisors, explained that for end-investors, ESG remains an important consideration when allocating to the insurance-linked securities (ILS) asset class.

She explained that ESG is increasingly being incorporated into the ILS market, saying that consideration of ESG issues is deemed to be “critical for the development of the ILS market and for insurance and reinsurance markets more broadly.”

As a result, “ILS managers are increasingly focused on improving ESG practices throughout the entire investment process,” Milazzo said.

But she also noted that, “Manager selection matters when considering ESG factors,” saying that, “Frontier has observed many instances in recent periods where ILS managers will deem contracts uninvestable on the basis that counterparties do not meet ESG criteria.

“However, there is variation with how stringent managers are with this process.”

Milazzo went on to explain that, for the ILS manager community, “environmental and climate change risk is of high importance.”

As a result, a significant amount of time and resource is put into understanding climate risk, the influence it has on specific perils and the effect it can have on ILS investments, Milazzo said.

She also highlighted that, as ILS investments are used to support resilience against natural disasters, this aligns with environmental sustainability goals.

On the social side, Milazzo noted that ILS investments also “inherently provide positive social impact in that they support the efficient functioning of the insurance market.”

ILS is one of the contributing sources of funding when natural disasters occur, helping in the rebuilding and recovery of affected communities.

Finally, Milazzo also highlighted that ILS managers own governance practices “have become increasingly robust over recent years.”

In fact, “It is typical for managers to conduct deep assessments of governance factors associated with all parties involved in ILS investments,” Milazzo explained.

Because of this, the ILS asset class is continuing improving and increasing the incorporation of ESG issues into its processes and ILS manager decision-making.

But, with ESG practices and their adoption not a level playing-field in the industry, it is important that investors do their own diligence on ILS managers, if ESG is one of their core investment tenets.

Recall that, the ILS ESG Transparency Initiative is a global insurance-linked securities (ILS) industry group of investment managers focused on enhancing environmental, social and governance (ESG) transparency in the ILS market.

When it comes to ESG, ILS manager selection matters: Frontier Advisors was published by: www.Artemis.bm

Our catastrophe bond deal directory

Sign up for our free weekly email newsletter here.

Verisk’s PCS expands Global Terror Index to include SRCC

This content is copyright to www.artemis.bm and should not appear anywhere else, or an infringement has occurred. PCS, a unit of Verisk, has announced an expansion of its insurance industry loss index for terrorism risks, with SRCC (Strikes, Riots, Civil Commotions, and Civil Unrest) now […]

Industry Loss WarrantyThis content is copyright to www.artemis.bm and should not appear anywhere else, or an infringement has occurred.

PCS, a unit of Verisk, has announced an expansion of its insurance industry loss index for terrorism risks, with SRCC (Strikes, Riots, Civil Commotions, and Civil Unrest) now being added to the PCS Global Terror Index.

![]() The company said that this enhancement will help the insurance and reinsurance industry in its understanding and management of political violence risks.

The company said that this enhancement will help the insurance and reinsurance industry in its understanding and management of political violence risks.

The addition of SRCC to PCS Global Terror will provide insurance and reinsurance firms with robust data for the assessment and quantification of risks associated with civil unrest, Verisk explained.

The number of SRCC events have been rising and as a result re/insurers need to accurately assess historical and current loss data for these types of perils, Verisk said.

This addition of SRCC loss data to this industry-loss index can provide companies with a systematic way to measure the frequency and severity of these types of events.

At the same time, the industry-loss index for terrorism can also be used for reinsurance and alternative risk-transfer transactions, such as industry-loss warranties (ILWs).

“PCS has identified over $10 billion in industry wide SRCC losses across 20 events dating back to 2010, compared to less than a billion on the terror side,” explained Ted Gregory, head of global PCS operations at Verisk. “This significant disparity highlights the need for a robust index that reflects the growing severity and frequency of SRCC events. By expanding the view of global political violence, PCS has developed an index that will help enable the market to trade SRCC on a standardized platform with an established methodology.”

Alex Mican, head of PCS global strategy and growth at Verisk, added, “The existing global terror (re)insurance market is small, but there’s a widespread view that it will grow significantly over the next decade. However, some structural changes are needed to facilitate its development. One important development will be the further entry of capital markets capacity to provide both reinsurance and retrocessional protection for companies assuming SRCC risk.”

Insured losses caused by unrest have risen to reach new highs in recent years, with SRCC risks rising in more than 50 percent of countries over the last 12 months, according to Verisk Maplecroft.

Verisk says that reinsurers have observed these losses and are now actively evaluating tools to support additional capacity and monitor this risk, with risk transfer becoming an increasing priority to manage exposures.

The SRCC enhancement to the PCS Global Terror Index product can help re/insurers access capacity from new markets, while it can also help exposed corporates such as multinational brands, retailers, and banks in understanding their exposure and whether their insurance coverage is sufficient.

Verisk’s PCS expands Global Terror Index to include SRCC was published by: www.Artemis.bm

Our catastrophe bond deal directory

Sign up for our free weekly email newsletter here.