US cat sees “material softening” in minimum rates-on-line: Gallagher Re

This content is copyright to www.artemis.bm and should not appear anywhere else, or an infringement has occurred. Catastrophe reinsurance pricing for programs in the United States is seeing “material softening” in minimum rates-on-line, broker Gallagher Re has said, as reinsurers “abandon” the need for top-layer […]

Industry Loss Warranty

Improved Florida cat reinsurance renewal conditions expected for June 1: MMC CEO

This content is copyright to www.artemis.bm and should not appear anywhere else, or an infringement has occurred. Early signs suggest that the Florida catastrophe reinsurance renewals at June 1st 2024 will see improved conditions for cedents, as capital has flowed in and reinsurer appetites have […]

Industry Loss WarrantyBanque Bonhôte launches ESG fund strategy incorporating catastrophe bonds

This content is copyright to www.artemis.bm and should not appear anywhere else, or an infringement has occurred. Banque Bonhôte & Cie, a Swiss private bank, investment firm and wealth manager, has announced the launch of a new environmental, social and governance (ESG) focused fund strategy […]

Industry Loss Warranty

US cat sees “material softening” in minimum rates-on-line: Gallagher Re

This content is copyright to www.artemis.bm and should not appear anywhere else, or an infringement has occurred. Catastrophe reinsurance pricing for programs in the United States is seeing “material softening” in minimum rates-on-line, broker Gallagher Re has said, as reinsurers “abandon” the need for top-layer […]

Industry Loss WarrantyThis content is copyright to www.artemis.bm and should not appear anywhere else, or an infringement has occurred.

Catastrophe reinsurance pricing for programs in the United States is seeing “material softening” in minimum rates-on-line, broker Gallagher Re has said, as reinsurers “abandon” the need for top-layer pricing to exceed the risk-free rate.

![]() While there are only limited US property catastrophe reinsurance renewals at April 1st, the broker notes that placements seen suggest a continuation of the moderation trend witnessed at January renewals.

While there are only limited US property catastrophe reinsurance renewals at April 1st, the broker notes that placements seen suggest a continuation of the moderation trend witnessed at January renewals.

All of which is playing out in the catastrophe bond market, where pricing for protection has softened over recent months.

“Capacity has continued to flow into the property catastrophe market, where capacity is sufficient to meet expiring and new capacity needs,” Gallagher Re explained.

Gallagher Securities, the insurance-linked securities (ILS) and investment banking broker-dealer arm of the broker noted the trend in the cat bond market through the first-quarter of 2024.

Saying that, “Cat bond risk spreads for most perils have declined 30% plus year-on-year but remain stable vs. Q4 2023 with growing capacity in dynamic balance with growing demand.”

You can analyse trends in cat bond risk spreads by year and by quarter in our chart.

While cat bonds generally place in the upper-layers of reinsurance towers, Gallagher Re noted that lower-layers are still more challenging for cedents.

“Cat pricing discipline continued at the bottom end of programs, where risk adjusted decreases were difficult to achieve,” the broker said.

While at higher layers, where the cat bond market is most prevalent, “We saw risk adjusted rate reductions at the top end of programs, particularly on capacity that was purchased new in the height of the hard market.

“We are seeing the end of “inverted pricing” where new top layers placed in the past couple years required pricing in excess of underlying layers.”

Gallagher Re sees the risk market as still firmer than property catastrophe placement for the United States, as capital has not flowed to that segment of the market as much as to pure cat risks.

“That said, across both risk and cat markets we are seeing material softening in minimum rates on line, as reinsurers abandon the requirement for top layer pricing to exceed the risk-free rate of return in US Treasuries,” stated Gallagher Re.

US cat sees “material softening” in minimum rates-on-line: Gallagher Re was published by: www.Artemis.bm

Our catastrophe bond deal directory

Sign up for our free weekly email newsletter here.

Improved Florida cat reinsurance renewal conditions expected for June 1: MMC CEO

This content is copyright to www.artemis.bm and should not appear anywhere else, or an infringement has occurred. Early signs suggest that the Florida catastrophe reinsurance renewals at June 1st 2024 will see improved conditions for cedents, as capital has flowed in and reinsurer appetites have […]

Industry Loss WarrantyThis content is copyright to www.artemis.bm and should not appear anywhere else, or an infringement has occurred.

Early signs suggest that the Florida catastrophe reinsurance renewals at June 1st 2024 will see improved conditions for cedents, as capital has flowed in and reinsurer appetites have recovered, according to Marsh McLennan CEO John Doyle.

Speaking yesterday during the Marsh McLennan earnings call, Doyle highlighted an improving marketplace for the clients of his firm’s reinsurance broker Guy Carpenter.

Speaking yesterday during the Marsh McLennan earnings call, Doyle highlighted an improving marketplace for the clients of his firm’s reinsurance broker Guy Carpenter.

The recent April 1st reinsurance renewals saw increased capacity and reinsurer appetite, which the broker expects will positively influence the June reinsurance renewals as well in 2024.

“Reinsurance market conditions remain stable with increased client demand and adequate capacity,” Doyle explained.

He noted that, “In the April renewal period, US property cat reinsurance rates were flat, with some decreases for accounts without losses,” while “Loss impacted accounts averaged increases in the 10 to 20% range.”

Adding that, “I think both markets continued to stabilise, on average, in the quarter. And again, I would remind everyone, it’s a collection of markets, not a single market. That stabilisation is good for our clients and in some cases a better market has led to increased demand in both insurance and reinsurance.”

Dean Klisura, CEO of Guy Carpenter went into some more detail, saying, “Market conditions are stable, but we’re definitely seeing increased client demand to buy additional property cat limit, particularly at the top end of programmes. That was very pronounced throughout the first quarter, at 1/1, through the quarter, and certainly that trend continued on April 1st.”

Adding that his teams are seeing, “Strong capital inflows into the reinsurance market, driven by strong reinsurer returns, double digit returns in 2023.

“Reinsurer appetite is increased for property cat, there’s an inflow of capital and capacity, competition at the top end of programmes, it’s been good for both buyers and sellers in the marketplace.”

Looking ahead to the mid-year, Doyle explained, “Early signs for June 1 Florida cat risk renewals point to improve market conditions for cedents, increased reinsurance appetite for growth should be adequate to meet higher demand.”

Which is already being seen in early placements for the mid-year and the catastrophe bond market.

Reinsurance capacity levels are expected to be more than adequate, while differentiation will continue and loss impacted accounts are still likely to see the greatest chance of increases, it appears.

However, Marsh McLennan CEO Doyle also commented that, “I would also say that insurers and reinsurers are cautious about that rising cost of risk environment that I mentioned as well. And so, while again a stabilising market is better for our clients overall, I don’t expect that relative stability to change anytime soon, given some of the rising cost of risk issues that the insurance community is confronting today.”

This “relative stability” suggests that the appetites for risk may not increase so significantly at the lower-levels of reinsurance towers, which are again likely to prove the most stable of all the layers placed at 6/1 and 7/1 renewals.

Improved Florida cat reinsurance renewal conditions expected for June 1: MMC CEO was published by: www.Artemis.bm

Our catastrophe bond deal directory

Sign up for our free weekly email newsletter here.

Banque Bonhôte launches ESG fund strategy incorporating catastrophe bonds

This content is copyright to www.artemis.bm and should not appear anywhere else, or an infringement has occurred. Banque Bonhôte & Cie, a Swiss private bank, investment firm and wealth manager, has announced the launch of a new environmental, social and governance (ESG) focused fund strategy […]

Industry Loss WarrantyThis content is copyright to www.artemis.bm and should not appear anywhere else, or an infringement has occurred.

Banque Bonhôte & Cie, a Swiss private bank, investment firm and wealth manager, has announced the launch of a new environmental, social and governance (ESG) focused fund strategy that will incorporate catastrophe bonds as one of its allocations.

![]() Pierre-François Donzé, Head of Asset Management at Banque Bonhôte, said that, “Our approach and the integration of ESG criteria, is based on a quantitative allocation methodology to identify appropriate investment opportunities in the entire spectrum of the fixed income bond universe.”

Pierre-François Donzé, Head of Asset Management at Banque Bonhôte, said that, “Our approach and the integration of ESG criteria, is based on a quantitative allocation methodology to identify appropriate investment opportunities in the entire spectrum of the fixed income bond universe.”

The newly launched Bonhôte Selection Global Bonds ESG fund strategy does not follow a benchmark, instead leveraging quantitative methods to identify assets to invest in from the fixed income universe, based on indicators that define the attractiveness of one type of bond, over another.

These can range from the majority of the global fixed income universe, including sovereign bonds, investment-grade and high-yield corporate bonds.

But in addition catastrophe bonds are a specific asset class that will be targeted for this ESG focused investment fund strategy, the private bank explained.

The private bank notes that, catastrophe bonds, “Offer an advantageous risk/reward and provide useful diversification through a performance that is largely uncorrelated with conventional financial markets.”

Explaining that, “CAT bonds, which are part of the insurance-linked securities (ILS) category, are used by insurers and reinsurers to transfer the risks of predefined events to investors.”

The strategy has been optimised for investors whose reference currency is the Swiss franc and takes into account the cost of currency hedging as well.

The use of ESG criteria to identify opportunities is “a fundamental part of our investment strategy,” Banque Bonhôte & Cie said.

“The fund promotes environmental or social features, or a mix of the two, by investing in the vehicles and securities of issuers with an ESG profile above the median of their peers. Many controversial business activities and sectors are automatically excluded,” the company further explained.

Catastrophe bonds can be up to a maximum of 20% of the ESG investment fund strategy

Julien Stähli, Director of Investments, stated “This new fund gives pride of place to ESG criteria and marks a further step in our long-standing commitment to responsible investment and quantitative approaches.”

Donzé also said the approach taken, “Makes it possible to add value compared to strategies limited to a single market segment. The indicators used estimate the relative attractiveness of the various segments of the bond market on a historical basis.”

He also said that the Global Bonds ESG fund portfolio will be “dynamically rebalanced” when the indicators used suggest this is necessary.

It’s clear that Banque Bonhôte & Cie recognises the investment qualities of catastrophe bonds and the diversifying benefits they can deliver to portfolios, as well as the inherent ESG qualities given their role in the provision of critical disaster risk financing to support the global insurance and reinsurance industry.

As we previously reported, Banque Bonhôte & Cie had said before that catastrophe bonds, as an asset class, exhibits the rare property of price moves that are independent of broader financial markets and so can be considered “the only true source of diversification.”

Banque Bonhôte launches ESG fund strategy incorporating catastrophe bonds was published by: www.Artemis.bm

Our catastrophe bond deal directory

Sign up for our free weekly email newsletter here.

City National Rochdale mutual ILW fund delivers 15.6% return

This content is copyright to www.artemis.bm and should not appear anywhere else, or an infringement has occurred. The City National Rochdale Select Strategies Fund, a US mutual insurance-linked securities (ILS) fund focused on investments into industry-loss warranties (ILW’s) and industry-index trigger catastrophe bonds, delivered its […]

Industry Loss WarrantyThis content is copyright to www.artemis.bm and should not appear anywhere else, or an infringement has occurred.

The City National Rochdale Select Strategies Fund, a US mutual insurance-linked securities (ILS) fund focused on investments into industry-loss warranties (ILW’s) and industry-index trigger catastrophe bonds, delivered its strongest annual performance in the last year, with an almost 15.6% return to its investors.

![]() With a now six year track record for this fund, Kurt Hawkesworth, President and Chief Executive Officer of the City National Rochdale Select Strategies Fund, commented, “The Fund’s 2023 portfolio performed well, with a net return of +15.58% for the year ended January 31, 2024.

With a now six year track record for this fund, Kurt Hawkesworth, President and Chief Executive Officer of the City National Rochdale Select Strategies Fund, commented, “The Fund’s 2023 portfolio performed well, with a net return of +15.58% for the year ended January 31, 2024.

“The Fund’s 2023 calendar year net return was the highest since the Fund’s inception and 2023 is the sixth consecutive year that the Fund generated positive, fundamentally non-correlated returns.”

Recall that, investment adviser City National Rochdale (CNR) offers this industry-loss warranty (ILW) and industry-index trigger focused mutual insurance-linked securities (ILS) fund strategy in the United States.

The capital from the City National Rochdale Select Strategies Fund is allocated to opportunities that are portfolio managed by the ILS investment team at Neuberger Berman and housed in its segregated account vehicle.

As Artemis’ index of ILW pricing shows, the industry-loss warranty (ILW) opportunity remains attractive, despite some notable softening of index-linked ILS products, such as ILW’s and catastrophe bonds.

That has helped the CNR ILW fund to a record return, over the last year to January 31st 2024.

Hawkesworth continued to explain, “The Fund’s 2023 return reflects the higher premiums realized following the occurrence of Hurricane Ian and increasing cash yields. In the catastrophe bond (“Cat Bond”) space, positive momentum for the Fund’s performance was assisted by a record total issuance in the primary market, and a secondary market that created tactical trading opportunities as sellers gradually sold off bonds maturing at the end of the year at a discount to raise cash for new issuances.”

Hawkesworth also noted that the CNR ILW fund portfolio was constructed to be more defensive, with higher attachment points, wider exclusions of non-peak secondary perils, and increased regional diversification through county- and state-weighted positions.

He noted that, weighted ILW protection continues “to become a larger share of the portfolio as demand from insurers and reinsurers for these products has steadily increased.”

He also commented that, “We believe that the incorporation of real-time environmental and financial risk considerations can have a meaningful positive influence on longer-term results and that our active management was an important driver of performance in 2023.”

Looking ahead, Hawkesworth explained that, “Currently, pricing in both the industry loss warranty (“ILW”) and Cat Bond segments continue to be attractive, albeit down slightly from the historic highs seen in Q4 2022. We remain confident that this environment will continue to present a compelling investment opportunity given the demand we are seeing as well as the structural and pricing improvements achieved post-Hurricane Ian.

“The Fund’s portfolio construction process for 2024 is now well underway, and we are focused on diversification and capital-efficient opportunities in the ILW and Cat Bond markets, where we believe risk-adjusted returns are most attractive.”

At January 31st, the total net assets of the City National Rochdale Select Strategies Fund had risen to almost $223.9 million, up from $218 million as of October 31st 2023.

Investments into ILW’s and industry-loss trigger cat bonds totalled $211.9 million of that, slightly down from the $213 million at October 31st last year.

The 15.6% return is healthy and outpaces many pure catastrophe bonds for that period, as ILW’s can often have higher return potential.

View our chart of industry-loss warranty (ILW) price trends here.

City National Rochdale mutual ILW fund delivers 15.6% return was published by: www.Artemis.bm

Our catastrophe bond deal directory

Sign up for our free weekly email newsletter here.

Mid-year renewals to see significant increase in US property cat capacity demand: Aon

This content is copyright to www.artemis.bm and should not appear anywhere else, or an infringement has occurred. Broking giant Aon is anticipating a “significant increase in demand” for property catastrophe reinsurance capacity at the upcoming mid-year renewals, with market conditions expected to continue developing favourably […]

Industry Loss WarrantyThis content is copyright to www.artemis.bm and should not appear anywhere else, or an infringement has occurred.

Broking giant Aon is anticipating a “significant increase in demand” for property catastrophe reinsurance capacity at the upcoming mid-year renewals, with market conditions expected to continue developing favourably for buyers.

“The positive direction taken by the U.S. property catastrophe reinsurance market in January and again at April 1 looks set to continue at mid-year, with ample property catastrophe capacity to meet demand, and signs of greater price competition,” Aon’s Reinsurance Solutions has explained.

“The positive direction taken by the U.S. property catastrophe reinsurance market in January and again at April 1 looks set to continue at mid-year, with ample property catastrophe capacity to meet demand, and signs of greater price competition,” Aon’s Reinsurance Solutions has explained.

Saying, “We anticipate a significant increase in demand for property catastrophe capacity at mid-year renewals, with attractive opportunities for reinsurers to put excess capital to work on well-priced lower layer covers as well as meeting demand for increased limit.”

The broking group notes that earlier renewal discussions are now happening on a significant number of US programs, while reinsurers are “ready to provide indications and lock in capacity.”

Among those reinsurers targeting property catastrophe risk, there is a “broad desire” to write larger lines in 2024, which positively for cedents means that “supply will be available for insurers looking to purchase additional limit.”

“As such, pricing improvement and enhanced consistency on terms is expected to continue heading into mid-year renewals,” the Aon Reinsurance Solutions team explained.

In addition to which, the broker believes there is now more openness among reinsurers to consider providing the kind of supplemental covers that had been absent from the market in 2023.

While there is also an acceptance that insurers will be looking to push more standardised terms across allocated lines.

For regional US insurance carriers, the efforts taken to improve portfolios are having a positive effect, Aon believes, with reinsurers increasingly showing a positive response to them.

“We are seeing a growing number of reinsurers writing specific regional programs for the first time,” Aon said.

Further noting that, “As reinsurers continue to acknowledge and respond to the portfolio, underwriting and structure enhancements made by U.S. regionals, the overall market for the segment will continue to stabilize.”

The Florida market is at a “dynamic” point in its history, Aon notes, as “legislative reforms and underwriting actions helped the market turn the corner.”

This bodes well for the June 1st renewals, when most Florida specific reinsurance towers renew.

The broker highlights that, “A group of 51 Florida focused personal lines property insurance companies tracked by Aon generated a positive underwriting income for the first time in the last four years with an almost $900 million improvement in net underwriting margin for 2023.”

Market dynamics in Florida are also set to result in a major shift of risk back to the private sector, Aon states.

Explaining that, “The shift of Florida Citizens customers to private carriers, combined with the expiration of the Florida government-funded Reinsurance to Assist Policyholders layer and planned increases in reinsurance globally for many insurers, will create significant additional demand for new property reinsurance capacity.”

The increased demand is expected to be met though, with reinsurance capacity for property catastrophe risk in Florida “set to return and expected to meet increased demand at mid-year renewals.”

In addition, the catastrophe bond market is playing a key role and “Catastrophe bond activity for Florida property carriers is also at record levels,” Aon says.

The broker counts almost $1 billion of Florida risk ceded through cat bonds through the start of 2024, while a number of cat bond deals remain in the market as well.

Read all of our reinsurance renewals news.

Mid-year renewals to see significant increase in US property cat capacity demand: Aon was published by: www.Artemis.bm

Our catastrophe bond deal directory

Sign up for our free weekly email newsletter here.

Florida Citizens: Capital markets “especially” positive for $5.5bn reinsurance renewal

This content is copyright to www.artemis.bm and should not appear anywhere else, or an infringement has occurred. Florida’s property insurer of last resort, Citizens Property Insurance Corporation, has said that its sees market conditions as especially positive in the capital markets, as it looks to […]

Industry Loss WarrantyThis content is copyright to www.artemis.bm and should not appear anywhere else, or an infringement has occurred.

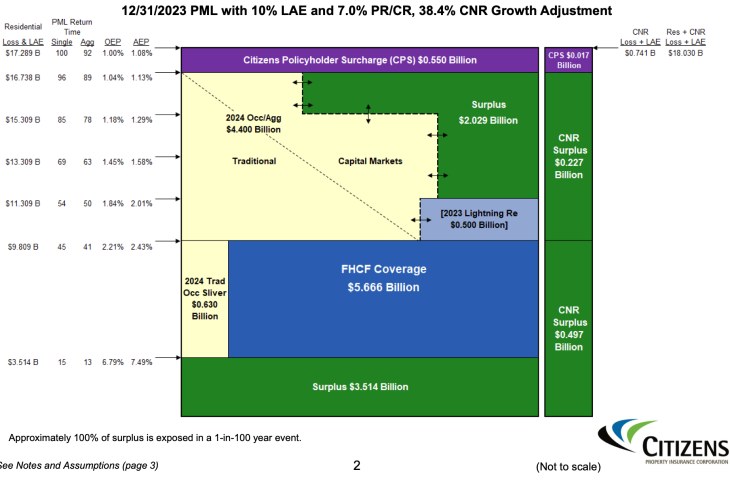

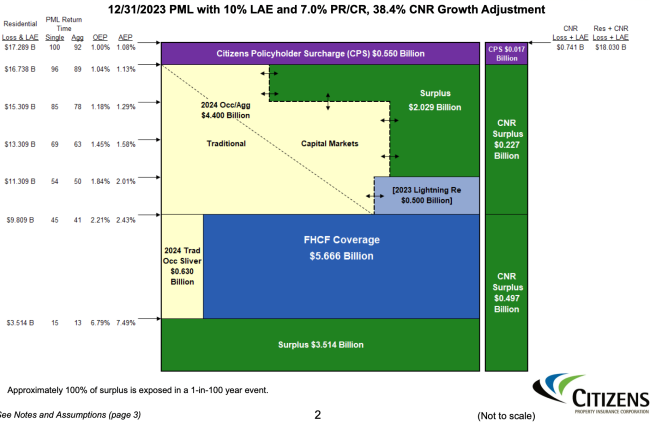

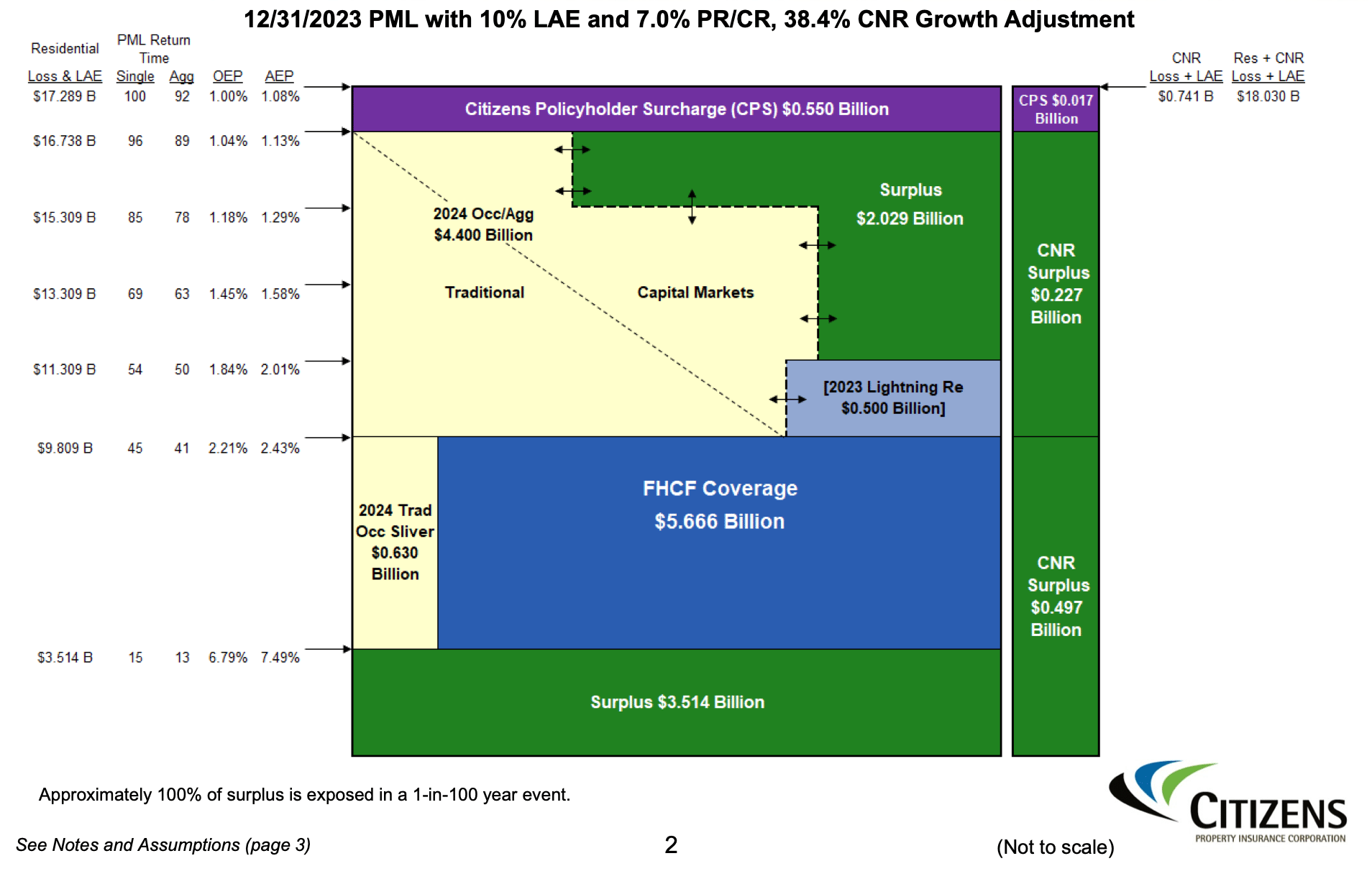

Florida’s property insurer of last resort, Citizens Property Insurance Corporation, has said that its sees market conditions as especially positive in the capital markets, as it looks to progress its $5.5 billion reinsurance renewal for 2024.

Citizens is expected to buy its largest tower ever, with a total of $5.5 billion of reinsurance limit needed this year.

The insurer has merged its three previous accounts, the Personal Lines Account (PLA), the Commercial Lines Account (CLA), and the Coastal Account, into a single Citizens Account and this is the first time Citizens is coming to the reinsurance market with this consolidated approach to its risk tower and risk transfer needs.

The total $5.5 billion reinsurance purchase will come in two main layers.

First, a sliver layer that sits alongside the FHCF coverage, which will provide approximately $630 million of per-occurrence one-year cover, in excess of at attachment point of $3.5 billion, to cover personal residential and commercial residential losses.

This sliver layer will be placed in the traditional reinsurance market and is designed to work alongside the mandatory coverage provided by the FHCF.

Above that will sit the bulk of Florida Citizens private market risk transfer and reinsurance (roughly $4.9 billion worth), with layer 1 attaching at $9.8 billion and extending to $16.7 billion, with reinsurance, catastrophe bonds and surplus all set to work together in this layer.

The residual market insurer is planning to keep its industry-loss triggered Lightning Re Ltd. (Series 2023-1) catastrophe bond for the coming year, clearly finding it a cost-effective form of reinsurance to continue paying the risk premiums for.

It’s important to note that this is not a new Lightning Re issuance, it’s just the multi-year cat bond rolling forwards and being maintained for another year for Citizens.

In addition to that, Citizens will need roughly $4.4 billion of new reinsurance and risk transfer for this layer.

Florida Citizens intends to procure this from both the traditional and capital markets, so more catastrophe bonds are anticipated.

Both aggregate and occurrence coverage will fill this layer as well, although it’s not clear whether any occurrence cat bonds would be issued, as Citizens has not sponsored a purely occurrence cat bond since 2013, with aggregate named storm cover the most likely structure, we believe.

This layer 1 of around $4.9 billion will provide reinsurance for Florida Citizens personal residential and commercial residential losses.

Now that the structure of the tower is better understood, it’s anticipated Citizens will get indications from markets to help it decide how best to structure the reinsurance within this layer and how much of it could be sourced in catastrophe bond and also collateralized reinsurance form.

Historically, Florida Citizens has always sponsored cat bonds and had a significant component of its traditional reinsurance provided by ILS funds, often in collateralized formats.

We see no reason to expect different in 2024. In fact, it’s anticipated that Florida Citizens could bring a particularly large catastrophe bond to market this year, while we’re also hearing that large lines are anticipated by some of the major ILS market players again.

Citizens staff noted that, “Thus far in 2024, global reinsurance markets, especially capital markets, have a positive outlook with an increase in capacity and demand with rates that projected to remain flat to – 5% depending on the cedent.”

No doubt Florida Citizens will have been watching the cat bond market closely and will be pleased with recent price developments for catastrophe bonds with Florida hurricane exposure.

A year ago, Florida Citizens secured just over $5.38 billion of reinsurance protection, from traditional and ILS markets, for 2023.

This consisted of $2.4 billion of outstanding catastrophe bonds, at the time of the renewal, and a fresh placement of $2.98 billion of traditional and collateralized reinsurance at the June 1st renewal in 2023.

Buying $5 billion of completely new reinsurance for 2024 is a significant increase, remember the Lightning Re bond is still in-force and will roll forwards to provide the other $500 million.

Florida Citizens: Capital markets “especially” positive for $5.5bn reinsurance renewal was published by: www.Artemis.bm

Our catastrophe bond deal directory

Sign up for our free weekly email newsletter here.

PGGM / PFZW lift ILS allocation ranges for Swiss Re sidecar, Nightingale Re

This content is copyright to www.artemis.bm and should not appear anywhere else, or an infringement has occurred. Target allocation ranges have been adjusted for some of the investments that make up the giant insurance-linked securities (ILS) portfolio managed by PGGM, the Dutch pension fund investment […]

Industry Loss WarrantyThis content is copyright to www.artemis.bm and should not appear anywhere else, or an infringement has occurred.

Target allocation ranges have been adjusted for some of the investments that make up the giant insurance-linked securities (ILS) portfolio managed by PGGM, the Dutch pension fund investment manager, on behalf of its end-client the Dutch pension PFZW.

In particular, the target allocation ranges for the Swiss Re private sidecar structure Viaduct Re and private mandate vehicle Nightingale Re have both seen increases in recent months.

In particular, the target allocation ranges for the Swiss Re private sidecar structure Viaduct Re and private mandate vehicle Nightingale Re have both seen increases in recent months.

As we reported back in March, the PGGM managed insurance-linked securities (ILS) portfolio had grown to more than US $9 billion in ILS assets under management by the end of 2023.

At that time, we also knew was that the investor had been making increased use of the Nightingale Re Ltd. private mandate vehicle, through which PGGM aims to partner directly with cedents needing reinsurance capital, entering into private transactions that can be significant in size.

By the end of 2023 PGGM’s insurance-linked investments team had made 11 investments using the Nightingale Re structure.

But, now Artemis has learned from the latest disclosure made by PGGM’s client the Dutch pension fund for the care and healthcare sector PFZW, that the target allocation range has been increased for the Nightingale Re strategy from the EUR 50-250 million, that was set as recently as the middle of 2023, to now between EUR 250-500 million as of January 31st 2024.

Which implies the Nightingale Re strategy could double, or more, for PGGM and PFZW if they chose to, with scope to increase the amount of private collateralised reinsurance activity entered into using the Bermuda vehicle.

Another notable change, in the targeted allocation ranges, is for the Viaduct Re Ltd. private reinsurance sidecar arrangement between PGGM and Swiss Re.

We reported back in 2020 that PGGM had made a second investment into Viaduct Re, which meant private reinsurance sidecar arrangements between the investor and Swiss Re had reached over US $500 million in terms of size.

But now, the latest disclosure from pension PFZW, shows that the target allocation range for PGGM’s Viaduct Re arrangement has risen from the EUR 250-500m it had been set at back at the mid-point of 2023, to now between EUR 500 million to 1 billion as of January 31st.

Which again suggests scope to double the allocation, should it prove appealing and the market opportunity conducive to do so.

With these allocation target ranges, which PGGM / PFZW have set for each of the ILS managers and reinsurance partners they invest with, of course we don’t have specific visibility of just how large each allocation is.

But, when the target allocation range doubles, it suggests there has at least been growth in how much capital is being invested through that arrangement or ILS partnership, at least tipping it into the new bracket, as it becomes too large for the old.

For most of the rest of the PFZW ILS investments managed by PGGM, the target ranges remain static since 2023, to such industry names as Aeolus Capital Management, Fermat Capital Management, Nephila Capital, LGT ILS Partners, Elementum Advisors, Munich Re, AXA XL, rated reinsurer Vermeer Re, Partner Re and SCOR.

But, for the first time we have visibility of the allocation to a fund managed by Integral ILS, which is named the Riemann Fund and has an allocation target range of EUR 50-250 million set.

There is also one that has declined, which is a strategy that had been managed by AlphaCat, the Soteria Fund, which at June 2023 had been cited as having a target range of EUR 250-500 million, but now presumably being in run-off since the acquisition of Validus by RenRe, that target has dropped to EUR 50-250 million.

However, the overall ILS allocation scope remains within a range of EUR 5 billion to EUR 10 billion for PFZW, capping the potential across all of the different ILS strategies and reinsurer partnerships.

PGGM remains the largest single investor listed in our directory of pension funds and sovereign wealth funds investing in ILS and reinsurance and is the biggest allocator in the ILS sector.

PGGM / PFZW lift ILS allocation ranges for Swiss Re sidecar, Nightingale Re was published by: www.Artemis.bm

Our catastrophe bond deal directory

Sign up for our free weekly email newsletter here.

Signs of growth in collateralised reinsurance market: Vickers, Gallagher Re

This content is copyright to www.artemis.bm and should not appear anywhere else, or an infringement has occurred. The level of insurance-linked securities (ILS) capital reached new heights in 2023 on the back of record issuance in the catastrophe bond market, and while collateralised reinsurance has […]

Industry Loss WarrantyThis content is copyright to www.artemis.bm and should not appear anywhere else, or an infringement has occurred.

The level of insurance-linked securities (ILS) capital reached new heights in 2023 on the back of record issuance in the catastrophe bond market, and while collateralised reinsurance has so far failed to rebound, there are signs of growth, according to James Vickers, Chairman of International, Gallagher Re.

Artemis spoke with Vickers around the launch of the reinsurance broker’s April 1 renewals report, which reveals that further price softening is anticipated as demand continues to rise alongside greater availability of capital.

Artemis spoke with Vickers around the launch of the reinsurance broker’s April 1 renewals report, which reveals that further price softening is anticipated as demand continues to rise alongside greater availability of capital.

After reaching record heights in 2023 and with cat bond market momentum persisting so far in 2024, Vickers feels that ILS capital’s influence could be quite significant at the mid-year reinsurance renewals.

“ILS capital is always playing a supporting role to the traditional market. But it is buoyant, and the spreads are coming down,” said Vickers.

“The best ILS fund managers are growing their funds under management; they produced some wonderful returns for 2023. And some of them we know have got offers of more capital that they feel comfortable to deploy. So, yes, ILS capital can be very helpful,” he added.

On the traditional cat bond side of the ILS marketplace, Vickers reiterated that ILS managers who’ve performed well almost have an embarrassment of riches at the moment.

“It’s more a question of can they continue to deploy their capacity at attractive terms,” he said.

But while cat bond market growth has been impressive in recent times, the collateralised reinsurance market, which is the largest part of the ILS universe, has stagnated.

“Collateralisation is an interesting topic,” said Vickers. “There are signs that there is a bit of growth there. Capacity is coming into that market, and for a lot of investors that’s a better way to enter the market. Partner up, do a collateralised sidecar with an existing, well-known reinsurer rather than investing in a bricks and mortar reinsurer from scratch.”

Vickers went on to note that it’s quite noticeable that a number of the new reinsurance startups that have been discussed have failed to materialise, stating that at this time, they don’t seem to be able to attract investors.

“And one of the reasons, I think, is that those who wish to invest in reinsurance, is you’ve got so many other options, such as collateralised sidecars, so if you can find the right partner, is quite an attractive option.

“So, collateralised, it may grow a bit, particularly as investors grow in confidence,” said Vickers.

Commenting on capital more broadly and whether it can rebuild this year and how influential that could be at the mid-year renewals and into 2025, Vickers said that if 2024 is another good underwriting year and the investment performance is decent, capital will continue to build.

“If you think what one good underwriting year can do, allied with reducing interest rates that are boosting up the asset side of the balance sheets as well, it can be quite significant.

“Having said that, as a reinsurer sitting sit there at the mid-year, you’ve still got the US hurricane season ahead of you, you’re probably not counting your chickens until you get to the end of the year and know what state your capital is going to be in. Touch wood, so far, it’s been a pretty good Q1. But just because nothing untoward happens between now and 1/6 doesn’t necessarily mean that reinsurers will be overly aggressive in terms of using their capital because they know that they’ve still got to get through the more traditionally difficult second-half year,” said Vickers.

Interestingly, Vickers told Artemis that while there appears to be a feeling around the investor community that the reinsurance market was hardening from around 2019 onwards, the reality is that 2020, 2021, and 2022 were all pretty poor years.

“And there are more hard bitten investors who think okay, fine, 2023 is a good year but one swallow doesn’t make a summer. Reinsurers need to produce another year and show that they can do it consistently,” said Vickers.

“Let’s wait and see whether reinsurers can manage a second decent year. Then I think the dynamics might change a bit. But again, smart investors will also be looking at demand as they will be worried if the capital grows too fast that’ll only push pricing down and the returns will fall away.

“Now, if they can be convinced that demand is going to grow and that capital can be put to good use at a reasonable margin, that’s another subject,” he concluded.

Read all of our interviews with ILS market and reinsurance sector professionals here.

Signs of growth in collateralised reinsurance market: Vickers, Gallagher Re was published by: www.Artemis.bm

Our catastrophe bond deal directory

Sign up for our free weekly email newsletter here.

Redistribution of risk opened up more reinsurance capacity at April 1: Gallagher Re

This content is copyright to www.artemis.bm and should not appear anywhere else, or an infringement has occurred. The “redistribution of risk” between primary insurers and reinsurance capital providers that occurred in 2023 has now helped to encourage and rebuild appetites, resulting in more reinsurance capacity […]

Industry Loss WarrantyThis content is copyright to www.artemis.bm and should not appear anywhere else, or an infringement has occurred.

The “redistribution of risk” between primary insurers and reinsurance capital providers that occurred in 2023 has now helped to encourage and rebuild appetites, resulting in more reinsurance capacity being available at the April 1st renewals, Gallagher Re has said.

In particular this has been evident in the property catastrophe and specialty reinsurance sectors, the broker noted, and this has led to more stable conditions at the renewal.

In particular this has been evident in the property catastrophe and specialty reinsurance sectors, the broker noted, and this has led to more stable conditions at the renewal.

At the same time, it has also helped to encourage more demand, resulting in better pricing and more capacity being available, so a far more calm renewal environment than was seen a year earlier.

In the property catastrophe reinsurance market, Gallagher Re notes a “continuation of reinsurance markets taking on more risk in search of the growth seen at the January 1st renewal.”

As a result, there was more available capacity for property catastrophe reinsurance programs and “incremental improvement” in risk-adjusted pricing at firm-order-terms, which the broker noted was “primarily at the top end of property programs.”

Interestingly, Gallagher Re noted that multi-class placement strategies were more prevalent, as buyers looked to capitalise on reinsurers appetites to write more property catastrophe business.

These multiclass placement strategies helped to support more challenging property per risk and casualty treaties, Gallagher Re said.

In addition, thanks to the increased level of reinsurance capacity being made available, Gallagher Re noted that property and specialty buyers were able to “secure improved terms and support in non-catastrophe areas.”

Gallaher Re CEO, Tom Wakefield, commented on the state of the reinsurance market at the April 1st 2024 renewals, “Broadly, the market has more capacity available, which is really encouraging. Industry capital has gone up by about 12% thanks to better combined ratios, fewer losses from natural disasters, and improved investment income.

“This means there’s more room to accommodate clients’ needs and should lead to better terms and conditions as a result. However, recent events in Baltimore remind us of the ever-changing dynamic market we are operating in.”

Read all of our reinsurance renewals news.

Redistribution of risk opened up more reinsurance capacity at April 1: Gallagher Re was published by: www.Artemis.bm

Our catastrophe bond deal directory

Sign up for our free weekly email newsletter here.

Further reinsurance market softening seen likely: Gallagher Re CEO

This content is copyright to www.artemis.bm and should not appear anywhere else, or an infringement has occurred. It is hard to see anything other than further small price improvements for reinsurance cedents given the strong state of both traditional and alternative reinsurance markets at this […]

Industry Loss WarrantyThis content is copyright to www.artemis.bm and should not appear anywhere else, or an infringement has occurred.

It is hard to see anything other than further small price improvements for reinsurance cedents given the strong state of both traditional and alternative reinsurance markets at this time, Tom Wakefield, CEO of broker Gallagher Re has said.

![]() The reinsurance broker’s CEO is anticipating further softening it seems, thanks to the increased levels of reinsurance capital in the sector.

The reinsurance broker’s CEO is anticipating further softening it seems, thanks to the increased levels of reinsurance capital in the sector.

Gallagher Re, in reporting this morning on the April 1st renewals, estimated that reinsurance industry capital has grown by roughly 12%, while alternative or insurance-linked securities (ILS) capital was also up by double-digits in 2023.

Driving home just how much more stable the reinsurance marketplace is today than it was a year ago, Gallagher Re noted that protection buyers were able to access increased capacity, firm order and clear programs at improved terms, as well as secure support in critical non-cat areas.

The broker notes that in 2023 the main driver of the challenging market dynamic was a reluctance to deploy limit, rather than any shortage of deployable capital.

But, in 2024, the appetite to deploy limit has improved significantly and also deployable capital has increased as well, resulting in much more attractive market conditions for buyers.

“Industry capital has increased by roughly 12%, driven by a mix of much improved underlying combined ratios, a light natural catastrophe load (despite insured catastrophes across the industry being heavy), and better investment income,” Gallagher Re’s CEO Tom Wakefield explained.

“Increased capacity, coupled with increased appetite, should lead to an easing of terms and conditions for clients despite the increased challenges facing the insurance market on natural catastrophe exposure,” Wakefield continued.

Gallagher Re also estimates that alternative capital in the reinsurance market, so that contributed by catastrophe bonds, other ILS investments and collateralized structures, has similarly increased by double-digits over the last year.

Alternative capital has been driven higher by the same market fundamentals of favourable catastrophe loss experience and elevated investment income, the broker explained.

CEO Wakefield noted that, “Despite there being no signs of a significant influx of new capital yet, other than into some of the best performing ILS funds, it is hard to see anything other than a slight further improvement in pricing from the cedant’s perspective.”

Suggesting that Gallagher Re is anticipating further softening and of both price and terms, as its commentary suggests a market that has more room to give back to the primary insurers, before it hits a limit in terms of its risk-appetite.

Wakefield’s commentary even suggests that softening could perhaps be more of a market feature, should discipline slide in certain pockets of the marketplace.

“It remains to be seen if the reinsurers who are falling behind their growth targets will maintain the same pricing discipline at the mid-year renewals which represent the last chance to achieve their 2024 revenue goals,” the reinsurance broker’s CEO said.

Read all of our reinsurance renewals news.

Further reinsurance market softening seen likely: Gallagher Re CEO was published by: www.Artemis.bm

Our catastrophe bond deal directory

Sign up for our free weekly email newsletter here.